May Investment Plan

The Alpha is in the System

We are closing one of my best months ever.

Not just in terms of returns, but in terms of significance. It proved that my system works and helps avoid mistakes, it proved that focusing on strength is how money is made, it proved that leaving your personal bias at the door improves your returns.

It proved that this Substack has value.

If you were to look at the last months of content, since I refocused myself in January, I was bearish on 95% of the market and extremely bullish on the few names which had a strong price action and demand.

I highlighted liquidity and stock selectivity issues from the market in February, focusing myself on defensives; proven right in March as most of the stocks I did not want to be in fell off the cliff and are still underperforming today, which didn’t make me more bullish - with reasons. I got a bit more balanced in April as even though I called a potential bear market, I also highlighted that at least one sector was worth buying: photonics.

Everything wasn’t perfect, I won’t claim the contrary. But over the months, my content was crystal clear: focus on the names and sectors which would yield the most returns at the best risk/reward. Following those regardless of my personal opinion led me to share defensive assets until March - while social media were buying falling knifes, and buy the strongest sector then, yielding wonderful returns in April.

Everything is written, black and white.

Everything is timestamped.

I started to quantify returns based on my articles and alerts shared in the Substack chat - which you should join as I share both my long-term and swing plans, creating two equal-weighted portfolios. You’ll find the logic behind both strategies here. I believe this to be the best representation of my stock picking and therefore this Substack’s value.

The long term portfolio, which buys and holds my positions at healthy valuation and price action, is up 57.59% YTD generating 53.64% alpha.

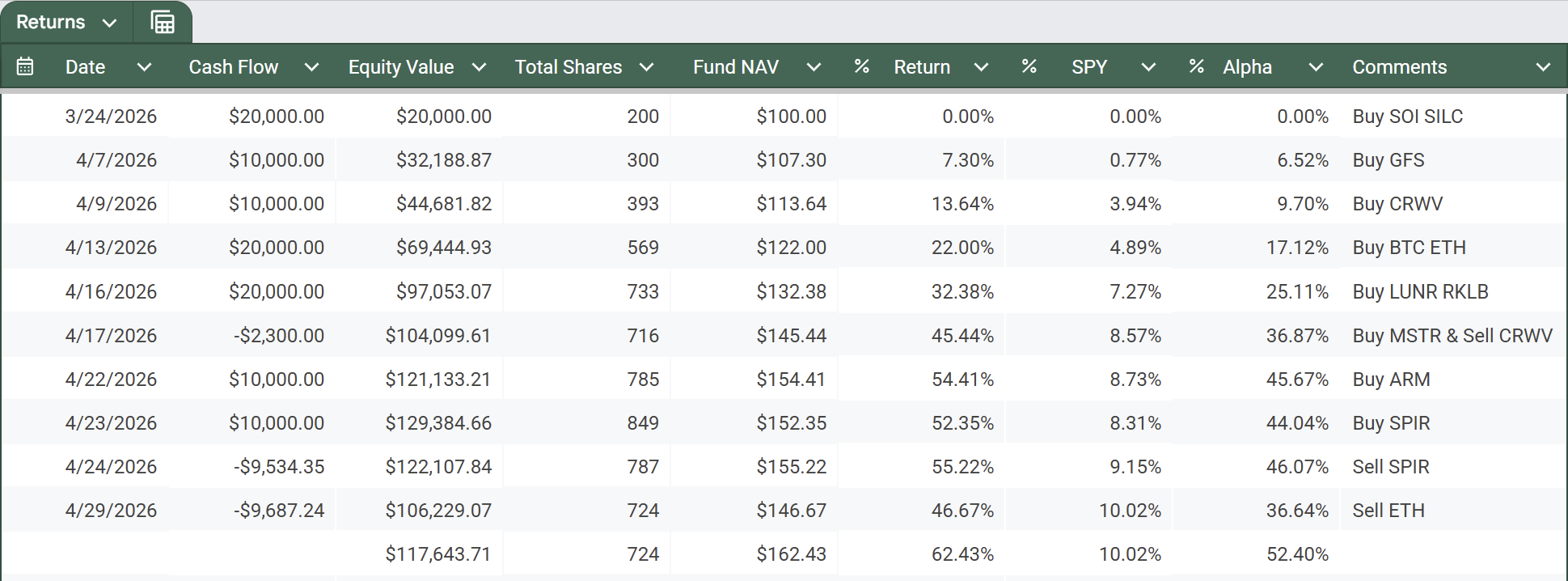

My swing portfolio, which buys interesting assets based on price action and market strength with a pre-defined plan, is up 62.43% YTD, generating 52.40% alpha since opening.

My personal portfolio is up 107.58% YTD at the time of writing, a performance to be proud of for a public bear. Mistakes were made and it could have been better, but the markets are a place of constant improvement, so I’ll continue to improve my writing, my investing and my trading.

Leaps have already happened since I started writing less than two years ago. Many more are coming. There are no limits to what can be done in the markets if one accepts to learn. There are good and bad times, but no real limits. So, let’s keep grinding, improve the system, and always generate more alpha.

Before we start, if you haven’t read those articles yet, I really advise that you do so. I will try to have a consolidated write-up in the coming weeks with my entire investing process revisited, but until then, this is what you should read.

Once again, I started to share some of my swings and price action alerts on Substack chat, and I don’t think all of you are aware/present. So if you are interested in those real-time alerts, this is the place to be and the next step on this service.

Now, let’s review the month, and plan for the next.

Today’s Market

I have no concrete answer on what happened this month - no one does, but I can try to share my thoughts. The market is forward-looking and cares about future cash flow generation. Today’s situation isn’t better than the end of March, it is actually worse. The Strait is closed, oil is not flowing, its price is rising and the consequences are concrete, real and will be long. We’ll talk about this later.

On the contrary, we have seen the first steps of peace talks, and this is what the market focuses on. Stocks sold off as the war started, even before it. Stocks ripped off before its end. Markets’ anticipate. What they see is a conversation between the two main actors. The U.S. was able to reduce Israel’s aggressiveness towards Lebanon while Iran accepted to pause its nuclear program.

The takeaway is that parley is possible, concessions can be made.

They aren’t made yet, but they can, and the market anticipates it.

This is one part of the market’s excitement; the anticipation of a soonish return to normal as mom and dad could discuss their issues like adults and make the best decision for the kids. Seems like the discussion is a bit more complex than the market originally thought, but it is happening.

The second part of the trigger is the market’s realization that demand for AI services and hardware is really strong and will continue, strengthen, and is simply necessary, not because companies like to spend but because they must spend; something I was already sharing months ago, but the market doubted it.

But once again: AI demand is through the roof.

The necessary next step is optimized, more efficient compute, to help providers deliver more with less. This grows revenues and margins by reducing costs & will reassure the markets about the financial soundness of their expansion.

This next step requires scaling up AI infrastructure. The companies providing this hardware - like ALAB, are not impacted by the CapEx risks that Oracle and others suffer from. Their business is simply manufacturing hardware, selling it at high margins and generating cash right away.

Maximizing compute per unit of space & energy is core for any provider’s profitability. Demand for the hardware capable of doing so will grow because providers have no choice but to buy it. They are in a race against their own leverage & need efficiency to generate cash as fast as possible.

Every data set of the last months suggests this take was accurate. Last week’s and this week’s earnings confirm it - and you should read both reviews to understand why AI hardware is the place to be. Hyperscalers need to spend on more efficient hardware to help GPUs compute. We simply don’t have enough, and today’s infrastructure cannot meet demand.

A number of AI companies, including Anthropic, have faced a capacity crunch for computing in recent weeks, leading to price increases for access to AI processors, outages, and rationing.

The market finally realized this and pushed AI hardware names higher, setting a new ATH on Nvidia, a significant move which quarters of jaw-dropping results did not achieve. Very hard for me to be bearish on the sector considering this as I ask myself.

Why would investors buy Nvidia higher today, without any news, while those jaw-dropping quarters didn’t make them blink?

I have two answers. Either they didn’t believe it then and believe it now - my opinion as the market is also pushing new hardware verticals and not just trading winners. Or this is only traders centralizing liquidity on a name before making their final profit.

Tomorrow’s Market

If you look at the market closely, you’ll notice that one risk sector alone is responsible for most of the gains this year: AI hardware. The only other sectors outperforming are defensives - energy or materials. The rest is either flat or down. Selectivity isn’t the sign of a bull market.

From a macro perspective, the Strait is still closed, damages is growing each passing day and the pressure to reopen it must be stronger than ever. It is hard to imagine countries like China not pressing Iran’s government - or whatever is the chain of command in the country, to accept a deal and move on.

Still, the entire world is taken hostage by both Iran and the U.S. and a moment will come - sooner rather than later, where pressure will make one - or both, break. This situation cannot continue or it will push major world actors to take drastic measures which would have fewer consequences than continuing with the blockade.

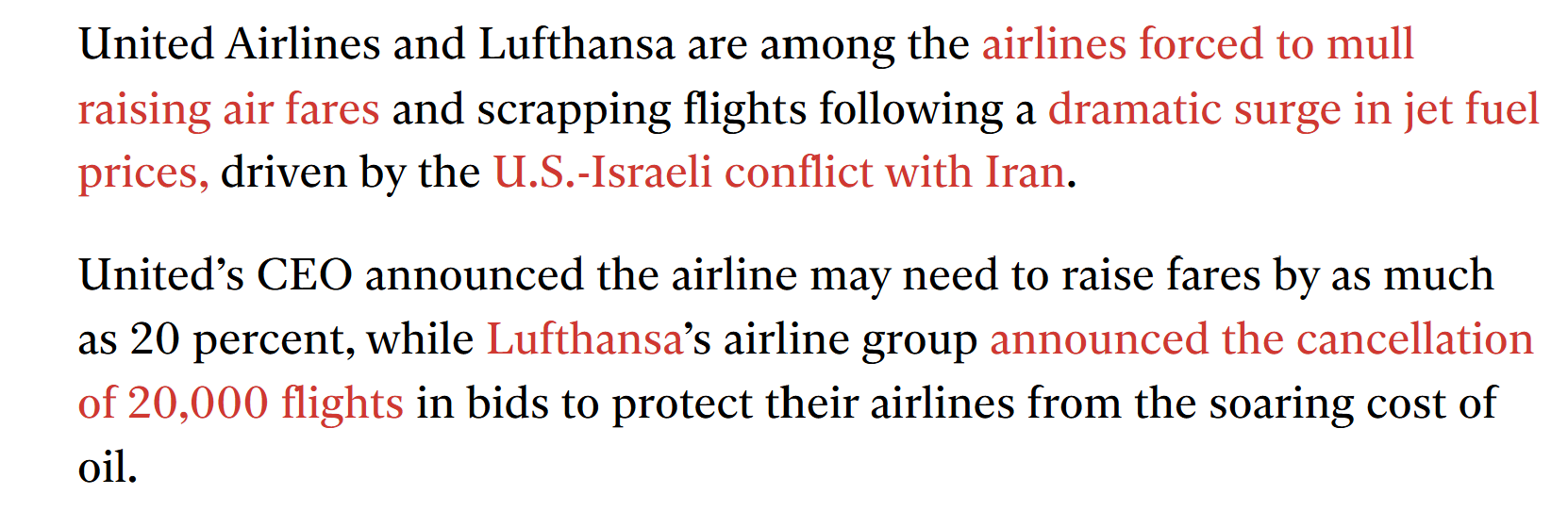

What is obvious today is that damages will be consequential. I’ve already talked about them, and we must be ready for when they show up. Don’t be surprised when/if inflation picks up and risk assets nosedive as the market anticipates economic slowdowns. The chances of this happening are high after two months of disruption - and counting. Another example – besides the last one about fuel prices in Portugal, is Airlines in Europe canceling some of their flights due to fuel costs. Reserves and future purchases are now depleted or not sufficient to maintain normal business.

I continue to be bearish on most of the market. Nothing changed, or maybe, a lot has changed for the worse, macro-wise; despite the S&P 500 being at an all time high, I see no reason to be less bearish than I was a month ago.

But I know two things for sure.

I cannot be 100% confident in my bias. Macro is too hard to anticipate and there is a possibility for nothing to happen, for economies to absorb this disruption or only have limited impacts. Even if my confidence in inflation is sky-high, I cannot know when/if that will happen.

If I were right and it were to happen before the end of the year, I still couldn’t predict how the market will react and what the situation will be like. AI hardware names might continue to rocket with massive spending while the rest tanks. Who knows?

So I continue to follow my system, and buy strength.

As long as the assets I look at hold their W50 and bounce on it, with strong narratives and fundamentals, I will buy/hold. I have no reason to behave differently.

The only thing I do differently is liquidity attribution. There is strength in defensive assets and I started pushing more liquidity towards them. Those hedge my portfolio short-term and would yield results long-term if I were to be right. It’s all about finding a balance between concentration, performance and safety.

But always focused on strength.

Portfolio & My Focus

Today, I see strength in three verticals and own 9 positions (Soitec, Global Foundries, ARM, Silicom Ltd, Rocket Labs, Intuitive Machines, VG, Intrepid Potash and SolarEdge). I usually hold 5 positions max but Rocket Lab/Intuitive Machines and SolarEdge/VG have combined the size of one which really makes 7 positions, while my account is running ~50% margin, which justifies more diversification, while 100% of my margin is set up on trades with stop loss, to mitigate risk.

Overall happy with my portfolio, but I will continue to rotate liquidity as the market moves and creates new opportunities, if necessary.

AI hardware, my favorite.

Strength is undeniable and broad. Winners keep winning, with TSM and Nvidia at all time highs after years of constant demand growth and cash generation while new technologies have a clear tailwind as the market is realizing that compute is and will be limited for years by physical constraints – you can’t generate more energy with a snap, the only way forward is optimized compute.

This creates many new narratives, or “bottlenecks”, the new favorite word on social media, and many new opportunities as some technologies must be built from scratch, from optimized energy sources to optimized semiconductors, etc… Everything is new.

I do not think retail investors realize the opportunity in front of us. This is one of the best times ever to make life-changing returns, if you focus on the revolution in front of you… Ignoring this sector today is a stock picker mistake.

Let’s break down the winners and my view of each.

Photonics. We’ve been over the technology and its key players, this is a must-read, not to buy today but to be aware of the players and their fundamentals for when opportunities are given. To be ready.

There are tons of ways to invest in photonics but most of those stocks have run too much to be safe risk/rewards so I’d personally wait for pullbacks, and I would make sure to buy only the good ones - the ones cited in my write-up. Poet taught us that many of them, the least necessary ones, will die slowly and be forgotten. Only invest in those who cannot be replaced. If photonics were to become the new normal, Soitec and GlobalFoundries cannot be avoided. They aren’t the only ones, but those are the right focus.

As for buying, the rule is always the same: be patient and keep a close eye on the W50. That’s where I’ll buy mine, and that’s where most of my liquidity will be going if given the opportunity - especially in Soitec, but not only. And if there are great swing plays, I’ll share them on the Substack chat.

Optimizers. Photonics is a wonderful technology, but it isn’t ready, lots of R&D is ongoing and volume production hasn’t started. This is the future, but AI inference needs to be optimized today. Which opens other verticals.

Engineering and design. Whether for photonics or not, everything starts by engineering. I have two names worth looking at on different verticals. Marvell for its focus on networking architectures, in high demand as bandwidth and latency are the current bottleneck; and ARM which is focused on optimized CPU architectures, also in high demand to orchestrate GPUs.

Hardware optimizers. AI inference needs to be optimized today, that comes with solutions which already exist. My favorite remains Silicom Ltd and their Ditto hardware, but I also need to talk about AsteraLabs which I had to close due to price action, but proved my thesis right a few weeks later. I’d gladly buy back into that one on a healthy pullback. Credo is also on my list, while I also look at current leaders with MU, Sandisk and the likes.

Compute providers. Besides hardware, as compute is constrained, neoclouds have a major role to play. I was wrong on thinking Nebius would be punished for slower growth due to physical constraints - although the market is still punishing others for the same reasons, but I was also right to buy back in on price action signals - even if that trade was closed to concentrate liquidity into others a bit later. Both Nebius and CoreWeave are excellent buys in my opinion, on healthy pullbacks.

There are many more excellent names, great buys and great holds, some I haven’t had time to look at and others I know but cannot focus on. I’d love to buy them all but never will, concentration makes returns. Never forget that 80% of your returns come from your sizing, not your picking. You do not need to buy everything, you need to be laser-focused on a few and execute perfectly with large positions.

Putting 50% of your net worth into a safer risk reward which returns 30% will yield more than a 2% allocation into a moonshot pushing 200%. You can pick a 10x and make no money. It’ll give you a great dopamine rush but it won’t make you rich, and dopamine isn’t really going to change your life. If you want dopamine, play sports. Don’t chase it in investing, it isn’t the right place.

All stocks aren’t meant to be bought, and you shouldn’t always run behind the shiny new ones. I made multiple times more money in a month with a large allocation on Soitec than in a year and a half holding Palantir from $17 to $180.

If that doesn’t inspire you to focus on what really matters: sizing, nothing will…

Space, the rising one

I shared my thesis a few days ago so I won’t go over it again, nothing changed since except that most of those names gave strong pullbacks. I did accumulate LUNR and RKLB as shared in my chat, but they now need to confirm and push higher, otherwise those will just be fake breakouts and force me to close my positions.

I have a smaller attribution on this sector, I believe in it and in its potential, but I prefer AI hardware. I only own two names and both combined are worth a full position ~20% of net liquidity; I do not intend to grow it much further as long as the AI trade continues. But I do not want to have all my eggs in the same basket so this vertical gives me an interesting risk diversification.

Defensives, the real hedge

The real diversification is here, with a much bigger portion of my portfolio at ~40% net liquidity, concentrated in VG and Intrepid Potash, with a smaller allocation on SolarEdge.

This isn’t only about my personal bias on macro, this is also because both names have a very strong price action, and did bounce on interesting regions to accumulate. My bias helps but I am still following my system here, with IPI bought on a strong volume breakout retest close to its W50.

I believe those three are the best candidates as many others names like Halliburton or Schlumberger, and defensive ones like Darlings or Smith & Wesson have already returned what I expected them to. I also keep a close eyes on material names, with my favorite being Sigmal Lithium and would gladly buy a pullback, as the stock ran 53% since presented, two weeks ago...

My focus remains on AI, the next step to look up to is the resolution of the Middle East conflict which shouldn’t be long, and will be resolved before the consequences show up on macro, which would give a window for the market to focus on tech earnings and AI buildouts. Until things change. Hopefully, they won’t, but I will not ignore strength in defensive names.

This is the market as I view it today. Price action confirms that the leaders are in AI so that is where most of my liquidity is, while keeping my portfolio balanced with other narratives, including a defensive one.

My Guilty Pleasure

I opened a trade this week, one I shouldn’t have as it doesn’t fit my system. But sometimes, breaking the system can work and I accept to take this risk because of the interesting risk/reward profile, and the position my portfolio is in today.

Transmedics, again. I’ll make the thesis short. The company is excellent, with almost perfect results for a good year now, an excellent Q4-25, and yet the stock is down -18% year-to-date and no one cares about it anymore. I did close my position as I never hold weakness - and was right not to.

So why look at it? Because it is a name I follow since two years now, and one I know very well. The narrative today is that as fuel prices spike, Transmedics’ margins will tumble while management shared multiple times that they were passing most of the added costs to customers. The market is expecting $174.4M in revenues while Q1-26 was record-breaking in terms of flights and Europe is starting to scale; I personally estimate the floor to be ~$172M only in U.S. so revenues should be a beat - or so I believe. Margins won’t hurt in Q1 and management’s comments should help the market understand the fuel pricing dynamic.

The stock is trading close to its lowest multiples ever while getting ready to share what could be its best quarter ever, show Europe expansion, reassure the market on fuel costs and give information about their ongoing trials.

For once, I trust my gut more than the market, but I trust it with a reasonable position in July’s $150 option calls. My bet is that the market realizes its mistake and reprices the stock properly post Q1-26 this Tuesday.

To be crystal clear, if I am wrong, those calls are going to $0.

This isn’t a trade for the faint of heart. This is a highly speculative position based on my knowledge of the company and its dynamics - which I could misunderstand. I am well aware of the situation and accept to take the risks, but this is an everything or nothing earnings play.

Let’s see how that works out.

Looking Ahead

We are still in the heart of earning season and there will be much more to say, with an extremely busy week coming, important for the portfolio: Firefly Aerospace, Palantir, On, Fabrinet, Lattice, Global Foundries, SuperMicro, AMD, Transmedics, AsteraLabs, Arista, Lumentum, SolarEdge, Nutrien, ARM, COHR, CoreWeave, RocketLab, Iren… And those are only the portfolio-impacting ones, not including the ones I have an interest in.

Going to be busy and you can expect one or two reviews this week. I know those are less read but keep in mind that following sectors and competition/partners is key in tracking our positions. I wouldn’t write about earnings if they didn't matter, it certainly would save me tons of time!

To conclude,

This is it for me, there wasn’t much news this month nor subjects to dig. The market is the same, the conditions are the same, the risks and opportunities are the same. It doesn’t always have to be complicated, sometimes the best thing to do is just to continue doing what worked.

So that’s what I’ll be doing. Look at the names I mentioned in this write-up, open the positions on those retesting key supports, rotate liquidity by cutting losers fast if I have some, trim weakening winners... The usual.

With Nvidia pushing higher, I wouldn’t be surprised if this market had more juice in it for new records as liquidity concentrates into the most obvious trade: infrastructure. Once again, with today’s news and dynamics, I do not see reasons not to have most of our portfolios invested in this vertical. If you missed the train or don’t feel comfortable buying, just let it be, wait for your turn. There’ll be more occasions. Just remember for the next times. Why play the game in hard mode? Focus on strength at healthy price levels and let the market do the rest.

This is one of the most hated rallies I have seen. Don’t fight it, don’t try to assume it can’t run higher or longer. It can. The game is different when liquidity concentrates into a few names or narratives, and a hated rally can last longer than any bears would have assumed. It will end, no doubt here, but what we need to do is to be ready for when it does, not try to guess when or why.

I’ll continue to follow my system, share it with you regularly with articles, reviews and chats. Join us not to miss anything!

Another month starts. Let’s kill it.

Thanks, great summary. As for your Substack chat posts, do you actually buy all the items you post about once they reach a certain price?

Thank you for the summary! The most exciting earnings week for photonics holders is coming up. This could provide clarity for speculative plays like SIVE. SIVE makes up 30% of my portfolio, still not sure if I should take some profit..