The Perfect Edges

Finding returns within a bearish market

I know you guys want to talk about photonics and risk assets. But my articles aren’t focused on tech but on returns and market’s strength - which means photonics and space today but strength is also rising elsewhere.

I have been bearish publicly lately, since the end of last year where most of my focus went towards defensive names like Halliburton or Schlumberger, with valid reasons as they overperformed most tech still today. I also highlighted clear changes on the market in February, a clear rotation to defensive assets in March and another bearish but more nuanced take early April, highlighting that even if defensives were the go-to for liquidity, there was strength in some pocket sectors – AI hardware/photonics and space as you guys know.

I did not have a 100% success rate, but it isn’t the goal of an investor. Outperforming is, and my defensive names did great until March 2025 while higher-risk/reward names I focused on later have rocketed during April. The equal-weighted performance of my stock picks has delivered 50% alpha YTD - pretty significant for a bear.

But this write-up isn’t meant to be a performance review, this introduction is just here to highlight that my view of the market today is biased and bearish, and even if there is strength in some risk sectors, I’d still expect some pain during the year.

Why So Bearish…

I don’t like being bearish. I rarely am. My work here is the entire opposite of a bear; what I look for all day long is strength, sectors where liquidity is flowing so I can ride uptrends. But sometimes strength is found in sectors which are structurally bearish for the economy and the risk assets in the market.

Oil, first. I went through it in length on my last monthly report, so I’d advise you to read it. The Strait of Hormuz has been closed for two months; impact on economies is real, increasing exponentially each passing day. What was a slower production or a reserve depletion which could be managed is either becoming a shutdown or a forced purchase of oil at quasi double usual prices.

And as the world is globalized, inflation in China hurts the U.S. If local production prices are higher, sale prices are also higher. Oil triggers worldwide inflation when it comes to goods, but not necessarily equally everywhere.

As energy prices differ around the globe, an explosive oil price inflation in Asia will affect local manufacturing more than in a region with lower energy prices inflation, the U.S. in our case - who do not depend from Middle East’s oil compared to Asia, meaning U.S-manufactured products should get more competitive.

Inflation takes time to spread through an economy. The effect won’t be seen before manufacturing cycles on new purchase oil end, which can take up to months in some cases - meaning today’s disruption will be felt in real inflation in months. To illustrate - even if this was a different situation, the post-covid inflation, triggered by massive stimulus, took a year from the stimulus start to real economy price increase.

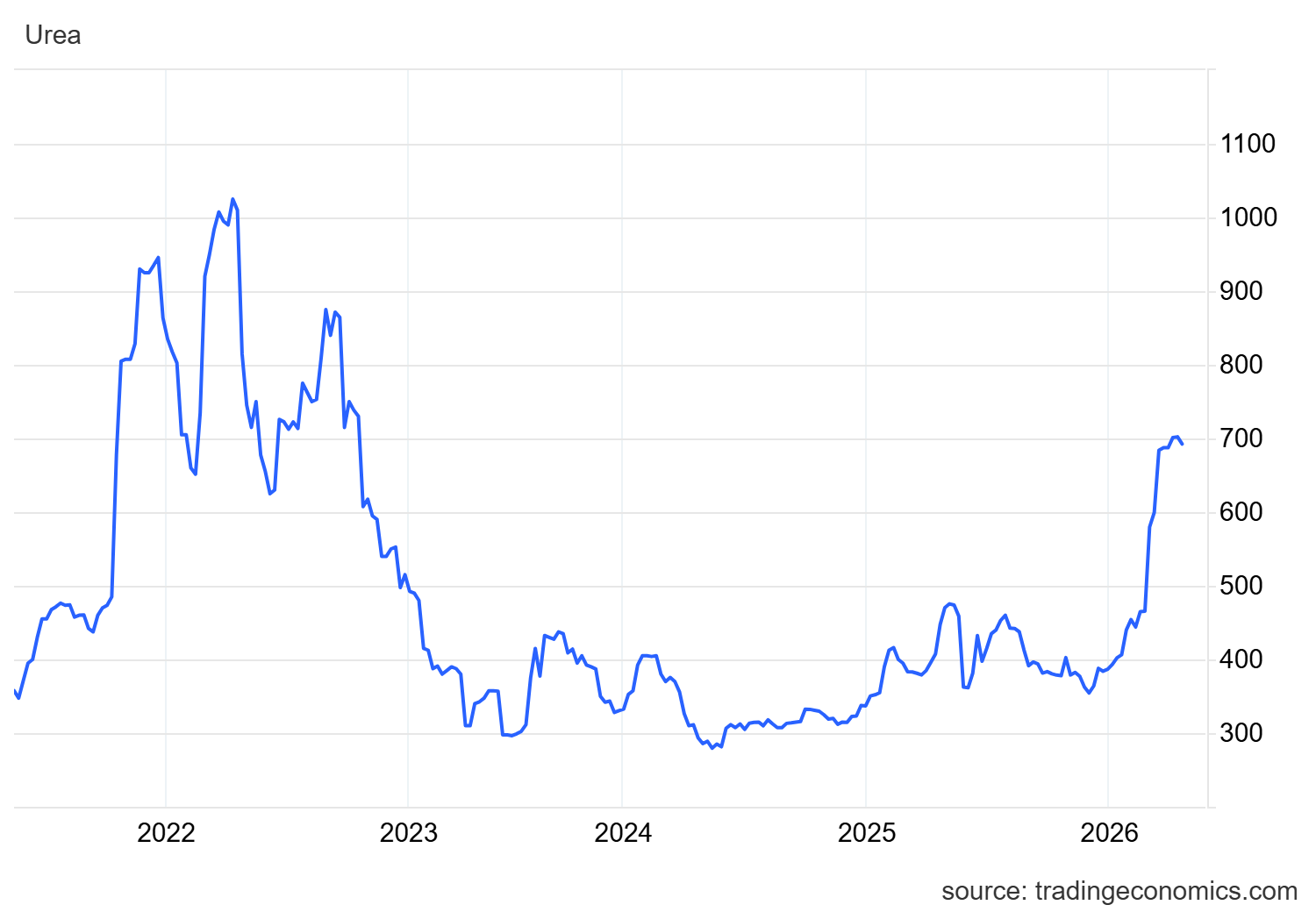

But there is more to it. As oil prices affect virtually everything, directly or indirectly, there is another key sector which relies on it: agriculture. Not just running tractors on the fields but also manufacturing chemicals; one of them used for almost any kind of agricultural production: fertilizers. Guess what is happening to the commodity price?

Energy is only one side of the coin, there are many others and when it comes to fertilizers, price increases mean more expensive food. It also means a more expensive commodity to be sold by those who produce it.

The Chemical Bull Run

If my bearish bias were to be confirmed, risk assets wouldn’t be the best place to be. Although that being said, trying to forecast macro and market’s reactions are a fool’s errand, but statistically, the chances for defensive assets to outperform is high - and a nice edge would be appreciated in such times.

In this kind of event, only a few sectors thrive; those who profit from the mess – usually first-necessity products producers, and those who protect you from it – usually currencies or precious metals. Useless to say energy and food are in the first category.

And there is strength in this sector: growing volume, breakouts and retests happening right now, meaning liquidity is flowing into them, probably trying to edge portfolios with at least one defensive narrative.

I found three companies worth looking at in this sector: Intrepid Potash, CF Industries and Nutrien - which we already talked about here.

Intrepid Potash

Here’s a brief review of the company.

Intrepid Potash, Inc. (IPI) is the sole domestic producer of muriate of potash in the United States, operating securely outside the volatile geopolitical supply chains that currently disrupt global fertilizer markets. While its core business provides a structural advantage in U.S. food security, IPI is actively pivoting to capture a stake in the domestic energy transition. Flush with cash from a recent $70M divestiture of non-core assets, the company is accelerating its "White Silver" lithium project in Utah. By proving the viability of extracting battery-grade lithium directly from its existing industrial brine, IPI is pitching a highly lucrative, "dual-sovereignty" narrative to the market: a completely localized U.S. supply chain for both agriculture and batteries.

The core of the thesis is its muriate of potash business - a potassium fertilizer to enhance plant growth and improve crop yield and quality, with a production in the U.S. allowing the company to benefit from price increases while being competitive compared to foreign exporters - also reducing shipping costs.

That’s defensive bull case, but it gets better; a $70M cash injection from selling non-core assets which helps their balance sheet and allows investments in another key vertical: lithium. I have already talked about this with Sigma - whose stock is up 50% since shared, and IPI would share comparable qualities - in terms of geography not ESG compliance. This is an ongoing project which comes with execution risks, but the potential is real.

At 1.61x sales, we are in the company’s average which isn’t cheap, but not expensive either assuming a potential bearish economy, growing demand, prices and potential lithium production in the next years.

The market is already optimistic with a clear breakout after the news of both the $70M cash-in and lithium plans, now close to giving the perfect ~$33 retest on its W50.

This isn’t an overly exciting position to take, but it would be an excellent edge against a potential pullback or slowdown in the global economy as not only its product would be more expensive and more demanded, but IPI would be given a premium for its local production.

CF Industries

A much bigger name with different tailwinds, still involved in fertilizers with an energy vertical, not lithium.

CF Industries Holdings, Inc. (CF) is a leading global manufacturer of nitrogen-based products, specifically ammonia, granular urea, and urea ammonium nitrate (UAN), essential agricultural fertilizers applied to soil to maximize crop yields. They also produce diesel exhaust fluid (DEF) to reduce industrial emissions. CF is a highly critical asset on two fronts. First, its North American manufacturing footprint provides a secure, highly profitable supply of fertilizer to the global agricultural market. Second, CF is repurposing its core product for the clean energy transition. Because ammonia is an incredibly efficient way to store and transport hydrogen, CF is scaling “blue” ammonia to be used as a zero-carbon alternative fuel for heavy-polluting industries like global marine shipping and power generation.

The company’s last earnings proved its cash generation stability, but the real stock price catalyst came from geopolitics and the advantage CF has over competition in a complex situation with higher energy and fertilizer prices - local production hence lower costs.

Just like IPI, the stock isn’t necessarily cheap today after pushing to a new ATH in March, but value is here, especially in the scenario where today’s geopolitics make a mess in the next months.

Just like IPI, price action is interesting with a new ATH and currently a healthy retest, far from perfect as we’d love to see low triple digits again to buy - and we might, depending on the Iran/U.S. negotiations this week, but interesting enough to keep an eye on it.

Once again, not an overly exciting investment but one which could protect capital, even yield interesting returns in case the economy went south.

Final Words

There are more fertilizer-related companies like Mosaic, for example, but the market hasn’t shown love to those and you know I only look at strength; those two are the best defensive/fertilizer-related names I could find on the market, and two great defensive opportunities.

Now, we have no idea what will happen and it is possible that energy prices end up being absorbed in the months to come and inflation never really shows up, or maybe just with a small spike, not hurting growth stocks. If it were to happen, it would take a few more months to do so, probably post-summer vacations or so; this would be the minimum holding period for those positions. And it would need to be sold if the risk were not materializing.

But just like I presented Halliburton, Schlumberger and talked about Dollar General or Dollar Tree - which all returned 50%+ in the next six months, there can be value in having a safer asset, an edge, within a risk portfolio. In the best-case scenario, this edge is not yielding much return and only consumes a bit of your cash while the market pushes risks higher. In the worst, this edge can be the difference between seeing your portfolio crushed, and having one healthy position generating returns to buy back strength on risk when it comes back.

Everything always looks easy when risk rockets, and we have a tendency to forget that a 50% return, whether on risk or defensive, yields the same amount of money. The only difference is the risk profile of your pick; and safer returns are always a better investment than riskier ones.

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

I would add that there are three main types of fertilizers: N-Nitrogen/Urea, P-Potash, and K-Potassium. And they are all needed for different purposes. The current blockade of the Strait of Hormuz has the most severe impact on the supply of N, which is a by-product of natural gas (with Qatar and Iran being among the largest suppliers around the world). The three fertilizer companies, as you mentioned, focus on different fertilizer products. IPI->K; NTR->P (+50%) + N (around 25%); CF->N. So invest accordingly. If you want a pure hedge against the current geopolitical tension around the Gulf, CF would be an obvious choice (which is also the most volatile one among the three). However, there are decent reasons to be bullish on all three as long-term trades. Have you also looked into agricultural products like $weat or $corn? I am smelling some opportunities there as a result of the severe fertilizer shortage/ price hike around the world, as well as the severe drought in the US.

Does publishing articles online help you become a better investor? I can imagine that putting your thoughts into words and sharing them with others might improve your thinking. Have there been times when this process led you to change your thesis or perspective?