Space & Lithium: Today's Opportunities

Three names with large narrative tailwinds & potential from my weekly screener

I ran my weekly screeners this weekend to find new opportunities - with quite a bit of success as shared in this note, and I am trying to figure out the best format to share this data regularly with you. For today, it will be a quick write-up on three names worth sharing, but I’d love to get some feedback on what you guys would prefer going forward.

Would you rather have weekly or bi-monthly articles like this one, focusing on the names I select? Or would you prefer weekly access to the raw data (~10 names per week) so you can dig into the names I don’t highlight (which included big winners like Marvell or Iridium these last weeks on which I simply didn’t have time to write), but that still meet my uptrend criteria? I could share this in a section of my website or simply drop it every weekend in the group chat - or something else entirely.

Everything is on the table, I just want to make sure it actually brings you value, you might also be satisfied with the way things are right now. Any feedback is welcome!

Intuitive Machines

Ticker: LUNR 0.00%↑

IM is about space logistics and lunar infrastructure. Their core business is to design, manufacture and operate lunar landers (Nova-C and Nova-D) to transport scientific and commercial payloads to the surface of the Moon. They basically manufacture the luggage that contains what “travelers” want to bring to the moon and goes inside the rocket - except in this case the luggage can move by itself and deliver your panties right at your hotel door autonomously.

- NASA")

This is the core but not the only competence they have, they also manufacture rovers, Earth re-entry vehicles and other pieces of hardware (propulsion systems, avoidance systems, autonomy landing software, lunar rovers…), communication solutions on or close to the moon - basically setting up internet up there, software necessary for any companies travelling in the region, and a few other smaller things.

If I were to summarize, IM is one of the key player on hardware/software requirements to explore the moon but also later on, exploit it.

Their business model today is to fund R&D and capital intensive missions with governmental contracts; they are the primary NASA partner for lots of hardware and software, with a five years $4.82B contract to set up communication and navigation services for missions in the region - the famous moon’s internet, and late March a new $180M contract for IM’s fifth landing mission for NASA’s Commercial Lunar Payload Services (“CLPS”) initiative. NASA financed the four missions for a total ~$390M.

IM-1 was the first commercial payload to successfully land on the moon ever in February 2024, and transmitted 350 megabytes of information during ~140h, a pretty large success even if the NOVA tipped on landing, preventing perfect conditions and only transmitted for a few days. Can’t succeed on the first try right?

IM-2 confirmed the technology’s capacity to land but did not land where it was supposed - ~250m away, and could not set its solar panel right ending in a power outage. Initial tests were successful, with more complex tests being cancelled.

IM-3 is supposed to launch H2-26 with no defined dates yet, with autonomous robots, radiation sensors, a lunar plant experiment, Intuitive Machines’ first lunar data relay satellite - to start building a commercial data relay network in lunar orbit, and more… And IM-4 is scheduled in 2027, launched with SpaceX Falcon for always more hardware on the moon.

I think the case is pretty clear already. The technology still requires fine tuning which can only happen with tests and IM is NASA’s preferred partner for those, with Firefly Aerospace as its main competitor as it is a wish for NASA to diversify - meaning contracts will continue to go towards both, and others. IM is the undisputable leader today and proved its technology already so as NASA intends to accelerate the frequency of launches and tests, IM will naturally benefit from more contracts.

This is our generation’s space conquest and it is a very serious one which the U.S. intend to win. If you wonder why, the answers are simply: the moon is filled of key resources we’d love to extract, its gravity and conditions make it an interesting geography for any kind of manufacturing (pharmaceuticals and semiconductors are already being manufactured in space with many advantages), plus the need to make humanity an interplanetary species.

These kind of missions and the global interest around the moon will only increase in the years to come. Becoming the go-to hardware manufacturer for moon exploration and later on exploitation is something, just like becoming the preferred launcher for commercial or touristic space travels for SpaceX or Rocket Lab is.

There is an entire economy and supply chain on the space exploration sector which is set to explode in the years to come - I could write on that if interested.

And as said so many time, with the markets being about liquidity first, sentiment second and fundamentals third, the space sector is a large focus for #1 and #2 while #3 are still speculative but also very real, with potential. With SpaceX IPO coming this year, the excitement around the entire sector is palpable and should only increase - at least until D-day, boosting #1 and #2 further. It is already happening to be honest with SpaceX expected to IPO ~$2T which is massive, Rocket Lab up 135%, PlanetLabs up 724% or ASTMobile up 323% since 2025. Space is hot.

Without any surprises, IM is pushing higher and meeting my criteria - growing volume on rising stock with breakouts, and Firefly Aerospace which is also a publicly traded company (IPOd in 2025 so chart is in daily timeframe) has the exact same profile. Same sector, same tailwinds, same momentum.

Both are on a pretty tough resistance right now ~$23 and ~$35, breaking those levels on volume would trigger a clear uptrend for months - hence giving a great entry, while retesting lower breakout ~$20 and ~$28 respectively would give a great risk reward accumulation point… Two really strong setups either way.

This is the bottom line of the trades, speculative but based on real fundamentals and potential, carried by a heavy momentum with SpaceX and the Artemis II mission, the push governments are giving to space exploration, etc…

Two positions I could personally take with a few months timeframe as I’d also expect SpaceX IPO to print a top in optimism and anticipation - too early to say for now but probable.

Sigma Lithium Corp

Ticker: SGML 0.00%↑

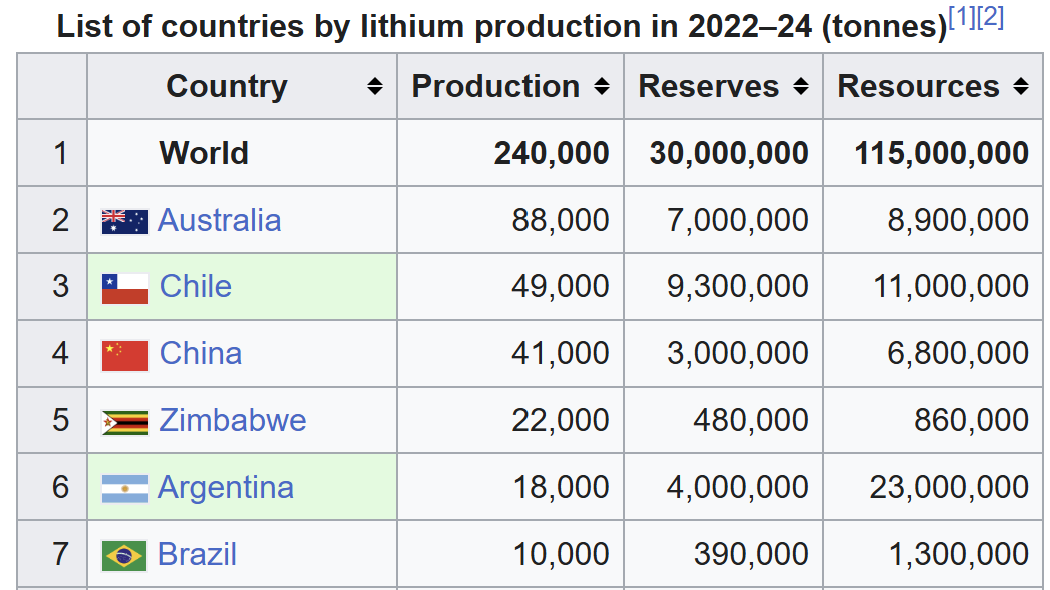

Much more classic within a well-known sector, a small capitalization still at ~$1.6B but with “less” execution risks and clearer demand for its products as we are talking about lithium - as advertised in the name. Sigma is a pure play on high quality lithium extraction, operating in Brazil with a few twists, transforming it from just another lithium player to a potential great opportunity.

First, the company certifies a “quintuple green extraction” (zero coal power, zero tailings dams, zero utilization of potable water, zero use of hazardous chemicals and zero accidents), which you might not care about but many companies do as they have environmental restrictions – the famous ESG regulations. This became important as most of the resource comes from China or Chinese operated mines and doesn’t answer these regulations.

As the west is working on independence from extraction to refining and focuses on ESG-approved commodities, Sigma will receive more demand - as my second point will confirm.

Second, the company signed a $100M collateralized bank guarantee fully collateralized by its own clients through a blend of corporate guarantees, letters of credit and export receivables to be mutually agreed. This is the equivalent of Meta and Microsoft pre-paying for Nebius’ compute before it is installed, highlighting the demand for its products and allowing them to invest healthily in their second Greentech plant to double production from 270,000t to 520,000t annually.

Healthy balance sheet and the financing to double their capacity – hence revenues, in the medium term. This comes with execution risks obviously but this is excellent news for the financial health of the company and its growth profile.

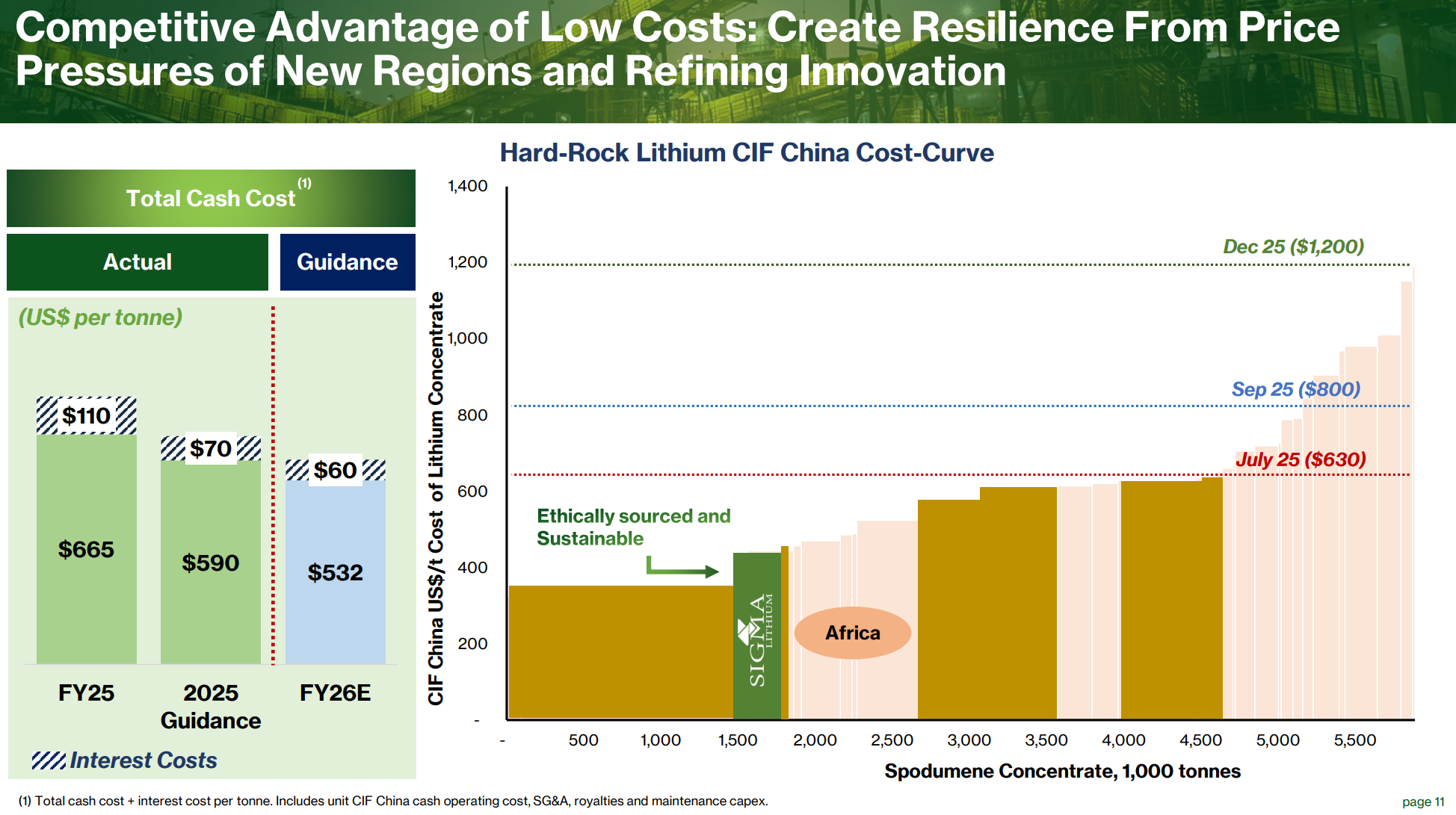

Third, as a pure play lithium extractor, Sigma is optimized with ~40% operating cash margins – pretty high for a commodity miner, and extracts the commodity for cheaper than competition - hence very competitive on the market.

Sigma is guiding to a $592/t extraction and shipping of their lithium, which puts them on the lowest extraction price on the sector - green position on the chart, while the red, blue and green lines are their profitability margins depending on lithium’s price, which as we’ll see has been rising and sits ~$2,000/t today.

Fourth, the geopolitical situation helps western companies with Trump’s tariffs forcing local production - Brazil isn’t local but it is close from U.S. factories which are being built to refine the raw material locally, while battery productions are already within the U.S. for some companies. As the continent works on building a supply chain locally - meaning without China, Sigma will become a logical go-to partner.

Natural resources are also on the rise for many reason - geopolitics and fears of supply chain shocks, raising oil being, refocus of liquidity… Raising resources are never great for an economy but we can benefit from it.

Lastly, the dollar falling is a big tailwind for Latin America comapnies as most of their loans – as confirmed with Sigma’s own loan, are denominated in dollars while their expenses to pay local workers and resources are in local currencies. I’ve wrote about this currency mix and how it impacts LATAM on MercadoLibre’s thesis.

In summary, Sigma is an optimized pure play with a very healthy balance sheet, an accelerating growth profile, healthy cash generation with an advantage with its ESG product compliance and cost competitiveness, while the global macro is a tailwind – less competition from China combined with cheaper operations in Brazil.

To put some perspectives, Albemarle Corp – its main competitor, has already ran ~170% over the last year without explosive news and while having a less attractive financial profile – but being a much bigger diversified company.

The second tailwind for the industry is the global electrification happening around the world now while lithium is the most important component for batteries – which are globally getting cheaper and more efficient for households and businesses alike. If we look at Tesla’s success with Megapacks and the rebound for solar installations for households, on which I am overly bullish and is pushed by the Iran war, then demand for lithium should continue to increase, and if the commodity is also more expensive, profits for producers simply accelerates.

And both Albemarle and Sigma charts show this kind of anticipation by the market. As usual for the latter, the same chart patterns as always.

Now sitting below a strong resistance which creates the same condition than both IM and Firefly Aerospace: a breakout on volume triggers a buy on the retest as the trend is starting, while a rebound on the W50 triggers accumulation anticipating for a potential breakout.

If we start looking at valuation, the stock looks more expensive than its peers but it also has higher cash generation, healthier balance sheet, a premium for the potential revenue growth, its ESG compliance, accelerating demand for local supply chain and cost competitivity, with the risk being execution risk for its expansions.

Another name I would gladly buy on the right price action conditions.

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

SGML's CEO Ana Cabral repeatedly highlights the fact that Sigma utilizes 100% clean hydroelectric power for its Grota do Cirilo operations in Brazil.

While Argentina mines far more lithium than Brazil, Argentina depends much more on diesel fuel to power its operations.

SGML stock price has doubled in the last 30 days.

Really interesting businesses, none of which I’d heard of before but all of which I’ll check out!