A Second Breath For Solar Names

When social media darlings with triple digit returns potential are forgotten

This is another story of cyclicality and inventory. Another cycle which finished in blood a year ago while social media kept screaming to buy a dip which kept on dipping until being forgotten, and as usual no one is here to pick up the leftovers.

Not many, at least; and I’ll be part of the few.

Enphase and SolarEdge were two darlings of the 2022 bull run and are down 85%+ since for many reasons, mostly valid ones. We’ll go over each of them and why the situation is changing and why these two could yield great returns over the next year(s), and how to capitalize on it.

Solar Systems & Hardware

I’ll start with a rapid overview on how solar systems work to share some basics and understand what Enphase and SolarEdge sell, and how they compete.

Nothing very complicated - at least on the surface.

Solar panels are set on the roof to catch luminosity and transform it into DC current - a certain type of current.

They are connected to one or many inverters depending on the system, which are meant to transform the electricity generated by the solar panel from one state to another - only AC current can be used by households’ hardware. They also are the brain of the system, managing production and distribution while transforming the current if necessary.

Inverters are connected to the grid, the household electrical system, and batteries - potentially, to manage electricity depending on the need and its most efficient usage. Sometimes reselling production is more interesting than consuming it.

Enphase and SolarEdge compete on two hardware: inverters and batteries, and on the system they propose to households which have fundamentally different architectures, both with their advantages and flaws.

Enphase’s architecture transforms current at the panel level, with inverters attached to each panel transiting AC current to an electrical panel. A system with 20 panels comes with 20 inverters; a more efficient current conversion, less impactful dysfunction and a globally more efficient system altogether, which also comes at higher expenses. The Rolls-Royce of solar systems; more efficient, more expensive.

SolarEdge’s architecture has a centralized system to transform the current to which all solar panels are connected. The representation above is SolarEdge’s system. It comes with fewer inverters and hardware, hence less expensive but with a single point of failure and a globally lower efficiency than Enphase. The Toyota of solar systems.

Both also sell batteries which are comparable in quality as of today and can simply be added to the architecture. They are the next narrative for solar systems as technology improved drastically over the last years and makes them very efficient - and worth the spending.

Both companies share the entire inverter market in the west and only have Tesla as serious competition when it comes to batteries with its powerwall system.

When it comes to quality and efficiency, Enphase is strictly better. But quality comes at a price, which gives SolarEdge a clear advantage while the latter has been improving in terms of quality and could become a more premium service than it used to be. Add to that that SolarEdge is also starting to sell to small companies who understand the value of solar systems, opening a new market entirely.

Both have qualities and flaws which will appeal to different clients. Both can thrive, as long as the sector thrives.

The Solar Industry & Pre-2023 Bull Run

The solar industry is born from a simple need: autonomy and self-reliance.

Solar is the cheapest source of energy and the only, or one of the only sources which can be used by households for self-reliance. I have a detailed write-up about energy and about how an electrical grid works for cities, which can be a great introduction, although not a necessary one.

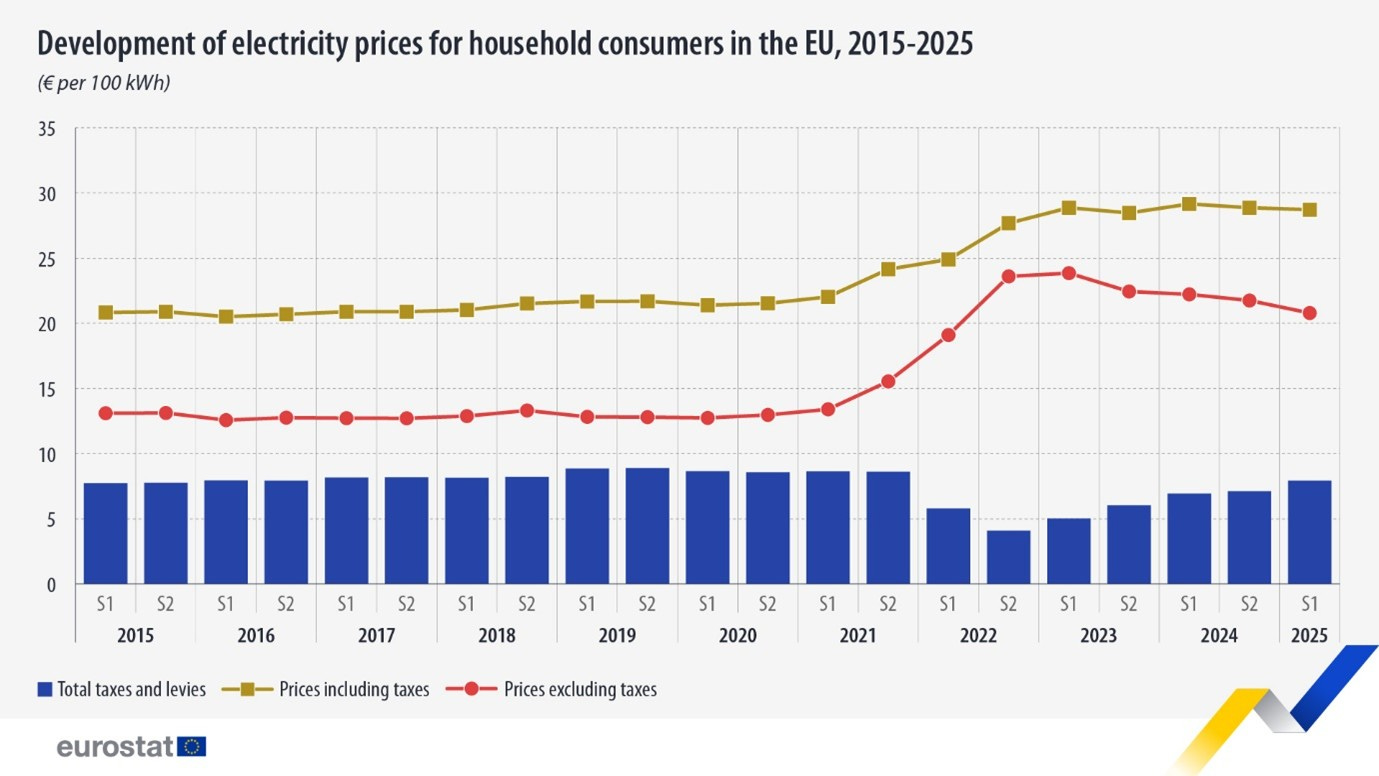

When it comes to households, it is becoming cheaper to have an efficient solar system to power your house than to rely on the grid and electricity price fluctuation which can be due to different reasons depending where you live - electricity price rocketed when the war between Russia and Ukraine started in Europe for example, and never went back down since, while taxes... Well, in general taxes never go down.

This is a constant and mandatory expense for households who have no control on its source, price or quality. The only control households have on their electricity costs is using electricity or not. They can accept to lower their heat or air conditioning but if they want to live at peak comfort, they’ll need to pay the price. Whatever it is.

Solar changes this as it allows them to have control and potentially be self-sufficient for their electrical production. The reason for that need is different for each household around the world but the advantages are the same for everyone; they do not rely on anyone but their system, and have a clear view on prices beforehand.

The early 2020s came with many circumstances which yielded a massive demand for solar systems across the west - U.S. and Europe will be our focus in this write-up, due to the advantages of solar systems but mostly external factors.

The economics were interesting during the COVID period with very low interest rates, allowing very low borrowing costs; an entire solar system can range from $10k to $30k and is usually financed by loans, hence the importance of low rates as a single percentage increase can yield thousands more to pay.

Regulations were pro-renewable in the west with favorable financing conditions, tax reductions, state subsidies, and more... They still are favorable in Europe, but the landscape changed a bit in the U.S.

Electrification was in full speed with Tesla being the most sold car in the west and requiring electrical installations, which was often paired with solar installation and drove demand.

Another important factor of the last cycle was California which was a specific case for the solar industry due to a specific regulatory framework.

In a few words, households were allowed to sell their energy production to the grid without pricing restrictions while the state had the most expensive electricity prices - $0.30-0.40/kWh vs $0.14/kWh elsewhere. That allowed homeowners installing a solar system to refund it in ~5 years compared to ~15 under normal conditions elsewhere. Everything post-refund of the system was pure profit. Very favorable conditions to finally make the step and finance your installation.

The situation changed in 2023 as households wouldn’t be able to sell electricity at grid rate anymore, slowing demand as the economics changed.

The combination of those conditions triggered the perfect conditions in the west for a gold rush on solar systems, and this is what happened. And as the conditions changed and demand stabilized, the classic inventory building cycle occurred. Installers were anticipating continuous demand and bought more hardware from manufacturers. As demand did not materialize, installers ended up with quarters of inventory.

Demand flattened, inventories were full, orders stopped flowing, revenues flattened, margins shrank, cash generation slowed and stocks crashed.

We’ve seen the dynamic with Nordic Semiconductors last week, and with hardware providers globally through the years.

As you can see in the revenues, the situation stabilized since with revenues flat since end of 2024 while comments have been positive on the installers’ inventory situation, which are emptied by now.

We are back to a healthy situation for those companies.

We might even be starting to see a rebound.

The Post 2025 Situation

The situation is much different today. Not only did the regulatory framework change in California, but it also changed everywhere in the U.S. since Trump took office - not much changed in Europe in terms of regulatory incentives as with the current energy “crisis,” independence is even more important for both countries and households.

On the U.S. situation.

The Inflation Reduction Act forced manufacturers to relocalize production within the U.S. which added costs - to build and equip the factories plus opex. This was rewarded by tax credits but the costs remain higher globally than delocalized factories, while the upfront costs had to be spent.

The Investment Tax Credit - a 30% tax credit to install solar systems, was cancelled so installation now costs a flat 30% more for households. It still exists for business in a different form.

Tariffs have and continue to create uncertainties and inflate prices.

On the positives, the most important factor were the last months’ rate cuts and the probable continuation of rate cuts at least in the U.S., assuming Trump were to have a puppet at the helm of the Fed, as otherwise we should expect stable rates at best, while Europe is back with pretty low rates already, healthy enough to fuel financing for solar systems.

Sector Recovery & Growth

Today, the need for solar energy and energy independence hasn’t changed. I am living in Portugal and went through the April 2025 blackout and the 2026 storms, which haven’t impacted me personally but highlighted the importance of independent sources of electricity for households.

Those blackouts and situations aren’t frequent, but we’ve had lots of them these last years in the west, the latest one in America in New York with record colds which put some tension on the grid with record electrical consumption.

Europe’s electricity prices haven’t gone down and shouldn’t go down any time soon as even with a renegotiation with Russia to access cheap energy, the pipes have been broken and will take years to rebuild - after years of negotiation, so this seems utopic. Solar is the only source of self-reliance for households and the cheapest source of electricity. That was true then, is still true now and will get truer in the future.

If given the opportunity, everyone would love to have solar systems on their house or apartments. The only variables for demand are external to the fundamentals. They are about prices, financing, purchasing power, installation times, etc...

California also adapted itself to its new conditions by adding batteries, which allow a more efficient management of their generation, storing when necessary and reselling on peak demand.

Under NEM 3.0, homeowners with battery storage can earn approximately $200 per week by storing solar electricity generated during the day and exporting it to the grid during high-value windows.

Solar.com analysis

Battery attachment rates have increased following those changes, passing from ~10% in 2022 to 70%+ last year. This trend will continue as batteries are now very efficient for an affordable price.

We see that demand’s starting to pick up, certainly due to the inventory from installers finally being cleaned up while the need for hardware continues, illustrated here with SolarEdge hardware sales which are clearly picking up.

This is the bull case from here.

Inventories are cleared, fundamentals are strong, need for solar is growing, financing conditions are easing. The questions from here are:

Will the financing conditions easing refuel demand and yield growth?

If so, which player will be the best performer in this scenario?

Enphase vs Solaredge

The market focuses on cash generation - you’ve probably heard me say that already, it’s probably the most repeated sentence on this Substack. This means Enphase will logically have a premium over SolarEdge due to its premium product, higher margins hence higher cash generation.

A company which generates more cash deserves more recognition.

Even ignoring that data issue Q3-24, you can see the difference in margins. Enphase will be a better stock and deserve a bigger premium, at least based on today’s data.

But things are changing.

SolarEdge has been transforming its business. They drastically improved the quality of their inverters after CEO transition, reducing their failure rate from ~7% to <2% compared to ~1% for Enphase, and have improved their batteries to be comparable to competition in terms of quality.

SolarEdge is a turnaround story that comes with execution risks but also potential. If they were to catch up in terms of quality and efficiency while still being cheaper than Enphase, demand would shift towards its product accelerating growth, stabilizing margins and growing cash generation. This is the vision of new management and their objective - assumed many times over the last quarters.

That said, it wouldn’t change the architecture advantages of Enphase - notably having independent panels which are globally more efficient and impactful in case of failure while also more complex. But it would make a serious competitor not only in pricing, but also in quality.

The battle for market share has been ferocious between both with Enphase at the top during the peak as regulations & financing conditions allowed most to buy premium, but SolarEdge is back at #1 as many focus on affordability again, while quality has increased making its value per dollar hard to compete with.

You can see this in the revenue profile of both companies as SolarEdge is clearly back to growth while Enphase is still a bit lagging.

One has growth & a potential transformation ongoing which would make it a serious competitor in terms of quality, market share and cash generation. The other is the established Rolls-Royce which could keep its throne and will be rewarded by the market with stable and higher cash generation.

Both require solar demand to pick up.

And both can win together.

Investment Strategy

SolarEdge’s bottom was ~0.7x sales with revenues declining ~60% at that time. This is what we can call a bottom and as this write-up showed, a situation we should not revisit now that inventories are clean and demand picks up. We’d need a comparable situation to get back to those multiples, and it shouldn’t happen short/medium term.

This ~2x sales was also the bottom before the run-up during the solar bubble with revenues were growing 100%+ and we reached the top around ~35x sales. I wouldn’t expect anything comparable but I could make the point that 1.5x-2x sales is a healthy multiple for SolarEdge - a great risk/reward, assuming healthy sector and operations.

To my opinion, normal operation is the least we could expect moving forward. We still could wish for more data about demand but we’ve seen it stable through quarters and guidance is positive - even with Q1 being the weakest due to seasonality. SolarEdge is an optimistic investment on management executing its transformation. If that were to happen, ~2x sales wouldn’t be normal, it would be cheap. Enphase did not reach 2x sales at the bottom of the inventory crash, it bottomed at ~2.3x sales.

Outside of black swans or recessions, I could see SolarEdge having a bottom around 1.5x sales while its potential could easily surpass 4x sales, probably higher, in the bull case of a successful transformation, growing margins and market share.

Price action-wise, we have what I look for.

A -97% through 3 years followed by a clear bottom late 2024, growing volume while holding that bottom which means accumulation, followed by different breakouts and a reclaim of the weekly 50 in August 2025, which have been held since except for some divergences slightly below.

The last quarter wasn’t as great as many would expect and yet was rewarded by a nice retest of the weekly 50 - which I personally bought, and a +15% right after, signaling that the potential of the turnaround was more important than the actual results, and that the market was optimistic about it.

Anything around $35 seems like a fair buy as long as the stock holds above its weekly 50 and local bottom ~$28. This is a great risk-reward I can take today with a very large potential if SolarEdge were to succeed in its transformation, even more if demand were to pick up and revenues/cash generation also accelerate.

On Enphase, we are a bit early to my taste. Growth is lower and demand for premium hardware might be slower to catch up but if SolarEdge does grow, Enphase logically should follow. The question is will they be able to retake market share while batteries are the most demanded products and their quality is on par with Tesla and SolarEdge while being more expensive.

Management said Q1-26 should be the bottom - although they have said that before as well. Personally, I believe Enphase is simply lagging SolarEdge & will follow, maybe a few more weeks to confirm the return of demand for premium hardware but that demand should return.

Price action is a mimic of SolarEdge a few quarters ago after a comparable drawdown followed by growing volume and a reclaim of its weekly 50. The stock is trading at ~4x sales which is correct as its local bottom was ~2.3x sales.

I wouldn’t buy there though. We don’t have confirmation of growth, margins, return of demand nor market share, we do not have a clear double bottom in terms of price action and 4x sales isn’t the best risk-reward for this name.

Enphase has great potential but I’d wait for a bit more development before chipping in, especially as if SolarEdge were to keep its market share or even increase it, the company - and stock, would suffer from it.

Both names have potential as long as solar demand continues, and I believe it will as long as financing is healthy - which should be the case moving forward. Enphase just needs a bit more confirmation while optimism is already here for SolarEdge. We’ll need a bit of time for those names to prove themselves, probably quarters, but there is potential for both for an optimistic and patient investor who can hold those for ~2 years or so, as long as the stocks behave properly and the news confirms the return of demand for solar systems.

Social media darlings are always ignored after they gave back all their gains.

But that’s usually when they pick up again.

I apologize for taking so long to share this report. SolarEdge ran since I started my position and finished my research; I was taken by other subjects & didn’t have the time to write…

Price action always gives second chances to the patient ones.

——————————————————

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

Hi I spent sometime reading your thesis on Solaredge. Sounds a solid picks. However, it feels like it’s a company that lacks strong moats. Particularly, strong competition with cheaper Chinese-made inverters in the European market (wonder if you have some insights on this particular risk)… Also, in the American market a main challenge has always been that Trump has personal disgust against solar and wind power…

Going to have to wait for the retest of the $35 sadly. Hopefully bring patient pay. Well done for catching this! 👏🏼