The AI Wearables Hardware Opportunity

When hardware cycles meet AI's wearable demand

Every year, I go back home in France for Christmas. We all went for a run this year on the 25th; it helps with digestion they say. As everyone were getting ready, the ones waiting formed a group to talk and compare their Garmin and look at my cousin’s, who just received hers on the morning.

I’m a nerd. I read and write financial articles; I have no clue what a “Garmin” is; so they all looked at me like I was an alien when I asked, before taking time to explain that it’s their watch. The best watch in the world apparently, for runners & athletes in general - or so they say.

There’s a reason for that introduction, don’t worry.

I’m still a nerd who runs but I usually do so with my feet, a short & ear buds, nothing else, or a t-shirt maybe. But here they were, waving their Garmin under my nose and explaining what it can do for you - and it doesn’t run for you. They kept comparing them until my uncle complained about his for one reason: his battery isn’t that great.

Something I could relate to with my Bluetooth earbuds. I don’t run for three or four hours, but a long flight or work session and battery’s dead. Charges really fast but it leaves an uncomfortable gap for me sometimes. His Garmin needed a bit longer to die but he still found it too rapid, a few hours usually, less than a day while using it with GPS trackers etc…

This is a clear pain point. Not just for my uncle & me, not just for watches & earbuds, but for millions, maybe billions, and for all wearables. Batteries don’t last long enough and the more functionalities they have, the shorter they hold. We want wearables that hold at least a full day so we can go about our day and charge them only at night, like we do with our smartphones.

Guess what we’ll be talking about today?

You probably guessed batteries. Wrong; half wrong. We’re going to talk about the nRF54L, which won’t give you much of a clue either, but by the time we finish this write-up you’ll understand everything.

It does have to do with batteries, though. And I believe there is a strong bull case here for many reasons, the first being the situation I just described. Would you pay a bit more for better battery life? For your Garmin to last twice as long, or even just 50% longer? For your earbuds to last 7-8 hours instead of 4h?

I would. I think most of you would too, and frankly, the last few decades have shown that battery life is one of the most important concerns for end users.

As AI evolves and new generation of wearables are being commercialized, we will be facing battery problems as AI drains it multiple times faster than traditionally. The new Meta Smart Glasses, for example, last ~5h with constant but basic use.

So you’d put your glasses on your nose for a zoo session with your kids and you’re done by lunch, with no place to plug it, unless you carry an external battery to use during lunch break. These products are already impressive but there is still massive need for improved battery life.

This is the situation as of today. Wearables are going to improve rapidly in the coming years thanks to AI, but their battery life won’t convince any user to buy. Everyone wants AI but no one wants to spend $500 on ~4h effective battery life.

Enter Nordic Semiconductor’s nRF54L: not a battery, a chip designed not to expand batteries themselves, but to optimize usage to a point where your wearable’s battery size feels like it tripled - or more.

Nordic Semi - The 2019-2022 Boom & Burst

Before talking about AI and the nRF54L, we need to talk about cyclicality. It’s no secret that hardware - chips in particular, are a cyclical business that follows product cycles. As technology evolves, companies innovate with products requiring more advanced chips, triggering demand that creates a virtuous cycle; until demand normalizes as penetration reaches its limit and we wait for the next wave to generate momentum.

This is a well-known process in the hardware industry.

Nordic’s first major cycle happened during COVID, which raised a key question for investors: were their products only demanded because of the unique circumstances COVID created, or is Nordic a real cyclical hardware player that will see demand with new products generation?

My answer is it will. The market is still doubting.

As to what Nordic sells, it is pretty simple: chips. Semiconductors. Tiny, ultra-efficient wireless chips that let smart wearables and IoT devices run for days or weeks on small batteries by optimizing compute usage. That’s it. That’s what they do.

And their hardware became a scarce resource when COVID hit, for two reasons.

Stuck-at-home consumers spent more on IoT devices and Bluetooth wearables like earbuds, driven by genuine demand: wireless mouse, keyboards for remote work, audio accessories. This wasn’t purely a COVID story, some of these were already becoming mainstream. Take the AirPods, first commercialized in 2019. A flagship product that democratized Bluetooth earbuds and which everyone still uses today.

Supply chain shocks from the demand surge for all kinds of tech hardware made it impossible to match orders. Nordic is a fabless company, meaning they design chips and outsource manufacturing to TSMC and others. As foundries were filled of GPU demand, Nordic’s products faced delays too.

The product demand was organic; boosted by COVID, yes, but these products are still in use today, still in high demand. Take wireless earbuds as an example. Demand kept growing post-COVID notably in 2024 with 12% YoY volume growth. That’s a sustained organic demand, not a one-time spike.

Every major smartphone company now sells wireless earbuds & most of them still use Nordic’s chips. The company had ~45% market share in this segment while Apple has a ~35% market share using in-house hardware. Meaning Nordic’s extremely dominant excluding Apple.

Earbuds are just one example. Nordic’s chips are found in wireless keyboards, mouses, gaming peripherals, fitness accessories, smartwatches and countless other wearables including healthcare - I’ll list some later.

Back to cyclicality. As demand grew, hardware manufacturers built inventories to meet it while the supply chain was overwhelmed. Delays stretched, orders kept piling up & were eventually filled. To a point where final demand normalized and inventories were self-sufficient to meet it. So orders for Nordic chips stopped.

Nordic’s order book looked like demand had vanished. The truth was end demand was still there; normalized, but real. Their customers simply had enough inventory to meet it.

This is what cyclical revenues look like.

Bluetooth-connected & wireless devices have never been more in demand than today and they’ll be even more tomorrow when AI-powered. This was a story of inventory build-up and the delay to work through it, not one of a product in demand due to a one time foreign even which changed the world for a fixed period of time.

And it’s starting to show in the numbers.

The demand bottom was reached in Q1-24, and there has been a clear recovery since. A recovery that confirmed Nordic’s hardware was still very much in demand.

Q3 came in slightly above our guide, in the higher end of our guiding range at $179 million, and we are enjoying a gradual recovery continuing through 2025, which we are enjoying with strong competitiveness from relatively old products.

CEO Vegard Wollan, Q3-25

Growth from relatively old products. Key words. We might finally be entering a new cycle, driven by a new product category.

The AI Wearables

I’m not going to blow your mind by telling you that AI changed the game. But AI until recently has been what? ChatGPT, Claude, autonomous vehicles, a handful of notable software… Nothing transformative in mainstream hardware.

Innovation takes time, but as the technology is now two to three years old - outside of pure research, we’re beginning to see commercialization of serious products. One example stands out above all others, released in early 2024.

Of course, not many wanted them at first. It was a gadget, not a very useful one as AI was early and the glasses didn’t add meaningful value to most people’s lives. But as the technology improved, the hardware’s capabilities improved with it.

Last year, more than 7M glasses were sold. Meta sold ~2M of them in 2023 and 2024 combined, a 350% increase in 2025 compared to the two prior years combined. This product was the only responsible for EssilorLuxottica’s FY25 growth.

There is no denying the demand for smart glasses anymore. They now allow you to do what you’d do with a phone, except better in certain respects as AI wearables have a few key advantages over our phones.

They don’t need a screen. Voice and gesture are enough to interact wit them.

They can see and hear what you see and hear making them context-driven.

They can be integrated into socially accepted hardware like glasses, rings or watches. It’s better than using your phone in many situations.

And one key disadvantage, very important for Nordic.

They need to be constantly aware of their surroundings to answer commands.

Meta’s management kept production low because they weren’t sure consumers were ready. They were right at the start but numbers prove they are now and management asked for production be boosted next year to ~20M units to meet demand.

I’ll let you guess two things. Who manufactures the chip responsible for optimizing power consumption in those glasses? And what is the most commonly reported complaint from users?

Nordic. And battery life.

Which should bring us to the core of this article: the nRF54. But before getting there, a brief word on the broader ecosystem; smart glasses aren’t the only product Nordic powers, even if they are the most iconic in the AI era.

Rings (Oura Ring and Samsung Galaxy Ring), used for fitness and healthcare to monitor heart rate, temperature, sleep and more. Discreet and data-rich, with ~6M units sold in FY25, and a ~50% increase expected FY26.

Watches like Garmin, Whoop, Fitbit… market leaders across use cases from high-performance sport to casual, feeding users with personal data as everyone is now comparing their REM sleep cycle for some reason.

Healthcare devices from Dexcom and Abbott; glucose monitors, cardiac patches, all requiring long battery life and reliable real-time response. Nordic’s industrial and healthcare segment grew approximately 60% YoY in 2025.

With many more to come with categories and wearables we don’t yet know about as all tech companies are working on their own product incorporating AI services.

Which finally brings us to the core product.

The nRF54

To recap, the core problem of wearables is battery & as we add capabilities, batteries drain faster. AI makes this exponentially worse: AI inference consumes 3x to 5x more energy than conventional processing, and the Meta glasses’ ~5h battery life under active use is already a bottleneck.

This happens because wearables face a unique constraint compared to smartphones: they need to be continuously aware of their surroundings. You want your glasses to respond when you speak, but only when you speak, not when someone nearby does. You want it to see what you see but only when you need it, not constantly. The device needs to know everything and to answer when asked while consuming almost nothing to identify your asking. It needs to see with eyes closed.

To illustrate Nordic’s product, consider the human brain: it is lazy, on purpose. When you’re sleeping, your brain doesn’t activate with every minor stimulus. Imagine if you woke up every time your wife moved a finger, you’d never sleep. Your brain would wake up your body, muscle, organ functions, and consume all your needed energy. No more REM sleep for you. That’s not what your brain does, it has habits and wakes you up only if it notices something unusual, to keep that precious energy for later. It isn’t only when you sleep, but constantly. It knows what information matters.

Nordic’s chips work on the same principle. They keep hardware in a low-power “sleep” state until something worth acting on happens, and avoid the constant wake-wake-wake cycle that drains wearable’s battery in hours. But they are pushing things even further with their latest product as they engineered it to incorporate a Neural Processing Unit capable of decision making.

AI factories train intelligence, but Nordic deploys it on device, at the edge, where the world happens. Edge AI is no longer optional, it's the only way to deliver safety, privacy, and sustainability at scale. Nordic's edge AI solution enables millisecond decisions without round-trip latency to the cloud and delivers radically improved battery life for billions of connected devices. This is the new standard for ultra-low-power edge AI, and Nordic is defining it.

Vegard Wollan at CES 2026, announcing the nRF54LM20B

Detecting gesture, filtering ambient noise or looking for voice trigger will not be done by the main processor anymore, but by the nRF54LM20B - which is the “AI” version of the nRF54. All those overly battery consuming tasks will now be done by an optimized chip while costing almost no battery. It only escalates to the processor when a real computing task demands it.

Result? the CPU sleeps 95% of the time, instead of waking thousands of times per day. This is not a small improvement; we’re talking about a leap forward.

Tests suggest wearable battery life could improve 3x to 7x from today; smart glasses approaching a full 12h of use, rings lasting a full week, medical patches lasting weeks. I started this piece by saying the minimum acceptable bar is a full day, allowing us to charge them at night like our phones - outside of healthcare. This nRF54 version is what makes that bar achievable for AI-enabled wearables.

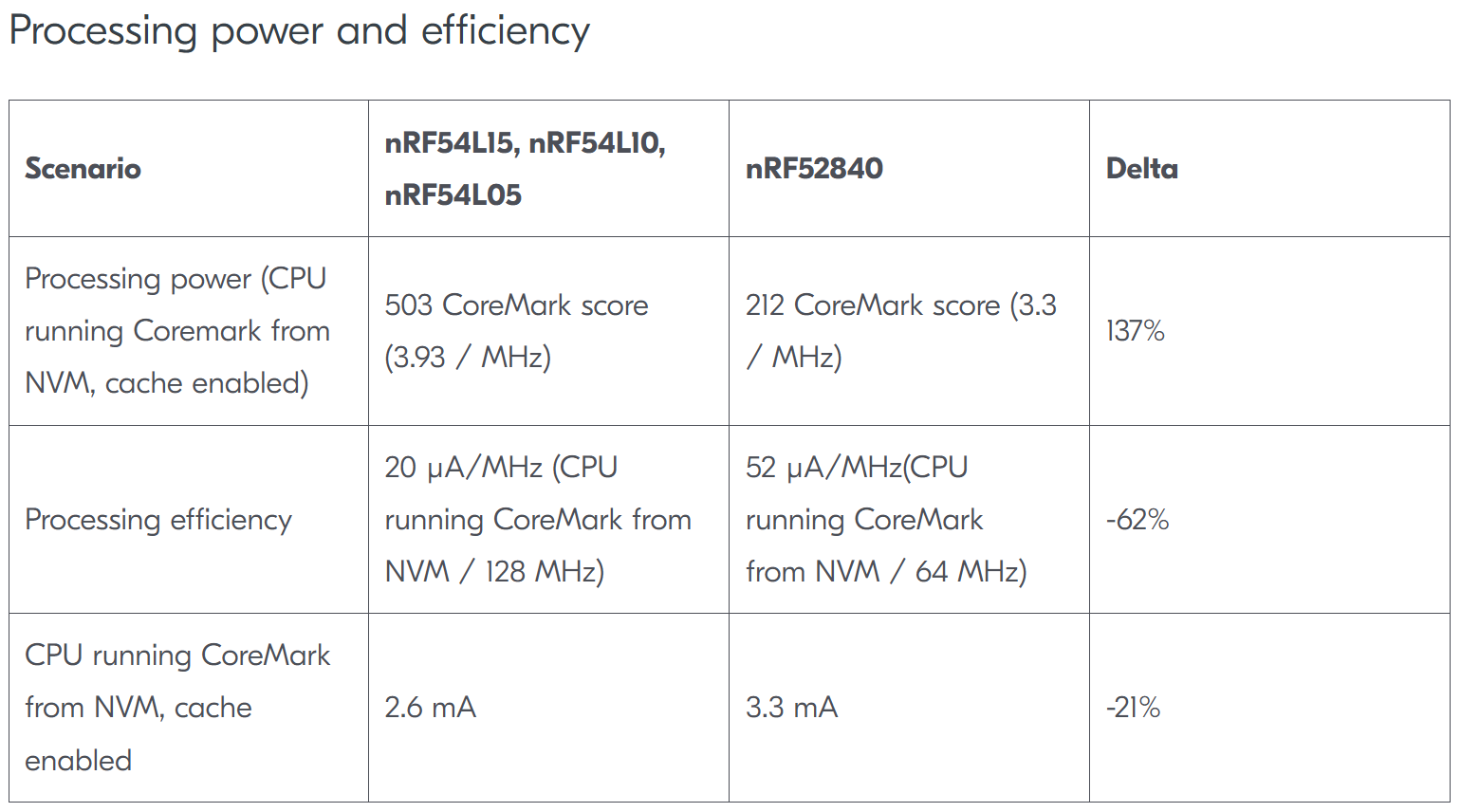

The nRF52 was released in 2015 and remains the industry standard for Low-Energy applications today, with ~30% of the global Bluetooth LE market shares - including Apple and its in-house tech once again. The nRF54 dramatically improves processing efficiency, is 50% smaller and has better memory capacities, enabling devices to run multi processes simultaneously.

More process. More capacity. Less space. Less battery consumption.

Competitive Advantages & Competition

Nordic is a one-trick pony. They have one product, different generations. What they do, they do excellently. Companies like Meta, Samsung, and even Apple in specific cases (Find Me service) use their products. There are several reasons for this.

They are the best on the market due to their specialization. It is always easier to do something exceptionally well when you have only one thing to do.

Their SDK enables deep customization; increasingly important in the AI era, where we already see demand for custom compute systems with GPUs and specialized accelerators. The same dynamic will apply to hardware chips.

Switching costs are massive. We’re talking about a tiny chip present in millions of devices designed to millimeter-level precision. Changing them mean redesigning the entire hardware to optimize space, weight, form…

The nRF54 is the first 22 nm Bluetooth Low Energy chip with an NPU to reach the market. As of today, there is simply no direct competition for this specific product. Nordic is setting the benchmark.

By Q4-25, the nRF54 accounted for ~15% of new Bluetooth LE certifications, up from less than 10% in Q3. A pretty clear momentum.

We have leadership in hardware with our 22nm and in software with Nordic Connect SDK. Our position as a connectivity hub makes us a unique life cycle management partner for customers.

Competition is limited. The most credible competitor was Silicon Labs which was acquired by Texas Instruments last year. They still are serious competition with much more resources now, but TI is already challenged to meet demand for general-purpose chips and it is unclear how they will use this new resource.

Designing a new competitive 22nm chip with NPU would require at least a year or two of engineering alone, time during which Nordic can deepen its partnerships and take place in generations of AI wearable designs with high switching costs.

There are Chinese alternatives, the European STMicroelectronics and others but none come close to Nordic’s level of power optimization and customization - yet. And for any premium wearable manufacturer, the geopolitical and tariff risks of partnering with a Chinese supplier is seriously taken into consideration nowadays.

The Opportunity

I try to avoid projections - they are nothing but optimistic maybes. But I’ll share the known partners and products using Nordic’s nRF52 that are likely to transition to nRF54. It won’t be revenue projection but it certainly gives an idea.

Meta Smart Glasses, projected to push production to ~30M by FY27. Compared to the 7M units this year this means a 3x net revenue increase only from Meta which should translate to ~$150M added revenue, ~25% of the company’s FY25 revenue. From one product.

Samsung Galaxy Ring, doubled production between FY24 and FY25 with assumptions pointing to ~3M units sold, another double, in FY27.

Oura Ring (all generations), projected to grow ~100% YoY.

Whoop, growing slowly compared to others at ~12%, but a consistent volume.

Garmin, low double-digit growth with increasing Nordic chip content as the growth shifts toward AI-enhanced models.

Google Pixel Buds, Logitech wireless peripherals, Dexcom and Abbott CGM patches… large-volume, steady-growth products already running Nordic chips, whose next-generation versions will require nRF54’s efficiency for AI features or just massive improvement in battery life with the non NPU version.

The growth over the next two years looks strong even ignoring any new AI wearable, while many should be commercialized by then given that Google, Amazon & Apple are all reported to be working on smart glasses and OpenAI is working on a secret hardware; plus countless existing wearables which will upgrade their product with AI capabilities and smaller companies creating new ones.

It doesn’t mean Nordic will have a 100% of market shares, but it sounds like they will either increase or stabilize it while volume will grow. A stable 30% share of an industry growing 30% is a pretty strong growth & that’s what we start to see in the numbers.

Some customers are concerned about potential component shortages, which may lead to restocking. We are fairly optimistic that we should be getting the capacity. Excellent collaborations with TSMC and GlobalFoundries as our two main foundries.

Wollan on the Q4-25 call.

Do I hear inventory stocking? Possibly. And if so, this could mirror the early stages of 2020-2021, with demand driven by real AI wearable and without a supply chain shock this time, which will not allow backlog to reach covid-period’s order books but still yield a pretty strong enthusiasm.

The 2022 demand was “phantom” due to inventory building. Those are now empty and Nordic is back to a clear growth trajectory with FY25 up 31% YoY and the latest quarters stabilizing at a healthy double digit growth.

With the nRF54 chip supposed to ramp up volume from 2026 and the actual trends in AI wearables, this could end up in growing demand, anticipation, inventory building and trigger a covid-like reaction in the stock, fueled by optimism.

The market already reacted after Q1-26 guidance that came in more than 15% above consensus at a 19% YoY revenue growth; analysts raised their expectations from ~12% to ~19% FY25 while the IoT sector is expected to grow in the high single digits.

Something is happening at Nordic, and it has a name: the nRF54.

We believe we are on track for our long-term 20% annual growth target, supported by our product portfolio renewal.

This is where I remind you that besides all the great stories, the only thing the market cares about is projected and safe cash generation, which can also play in our favor with Nordic.

Gross margins are what you’d expect from a fabless semiconductor company: 50%+ and rising. That rise is driven by three factors.

nRF54 is a higher-margin product, even if price is comparable to the nRF52.

Software revenue, introduced in 2023, is now bundled with chips to help clients customize and optimize usage, and they will use it even more with AI needs; a new standard in the semiconductor industry.

Revenue mix is improving with smaller specialized customers, notably healthcare who pays a premium with lower volume.

Global efficiency after inventory destocking and larger orders to TSM and other fabs - more volume means cheaper units.

These tailwinds are structural, not temporary. Management has guided toward 55% gross margins, long term, hence stabilization.

Net margins are weak though for a semi company at ~2-3%, but these are set to expand as revenue scales as expenses shouldn’t increase as fast as revenues and there’ll be a point where any net growth will expand margins & cash generation.

That double acceleration is the core financial argument for the stock; it’s what we need to have a stock repricing.

Investment Strategy

This one is straightforward to me: common shares. I see no value in using options on a company of this size, at this valuation, with this level of timing uncertainty. I usually use options to boost returns on high-conviction, low-volatility names with clear near-term catalysts and low valuation. Nordic doesn’t fit.

We are not talking about a multi-billion-dollar blue chip at low valuation, but a $2.6B Norwegian company at fair multiples. This is a small-cap and it comes with risks and volatility of a small cap.

Nordic is not cheap today. At ~NOK 140 or ~$14.50, it would be if the AI wearable thesis plays out - if we are indeed entering a new inventory cycle driven by nRF54 demand. But until that is confirmed by more than one strong guidance, we are trading at or slightly above fair value for the current business.

We’re all used to 20x sales being called cheap by now but we shouldn’t.

I don’t expect Nordic to deserve a re-rating outside of my bull case. That said, a 20% growth rate at a stable multiple would still yield strong return, and that seems to be where we’re headed on the base case. But expanding margins, growth acceleration and inventory building are the bull case and cause for re-rating and a deserved ~8x sales multiple. That’s where we have real fun.

What makes this play very interesting to me is the limited downside, or reasons for a downside. Every fundamentals point to positive outcomes and the stock is trading at a fair valuation excluding this positivity, as if we were going for years of low double digit growth and stable margins. The bear case would be Meta shifting to in-house chips or another provider but as said, while possible, it is unlikely.

A 3x - 4x sales is fair for a company in Nordic’s actual state and comparable to peers. Anything lower would require an external event and we saw even in the worst of the inventory situation, Nordic fell at 2.2x sales. We shouldn’t get any close to this kind of situation in the next year or two.

What I would call a great opportunity at acceptable risks.

Price action wise, you can clearly see the post-COVID inventory crash and we’ve been in a gradual uptrend since, without fireworks but with an established bottom in March at peak order book weakness followed by healthy higher lows.

The stock reached a higher high ~8 months ago and has been consolidating since. The market is waiting for nRF54 to actually ramp in the numbers and even if Q1-26 guidance confirmed this, the market isn’t getting too optimistic yet.

It’s clear that the nRF54 Series is contributing very small in 2025. It is a year where our workhorse, the nRF52 Series, is predominantly our revenue - products that are relatively old. The Nordic team has done a great job defending that position up until having the nRF54 Series. What’s really energizing for us is that we see the strong competitiveness of our new 22nm platforms.

We are currently just below the prior higher high, above the weekly 50, on the second-highest volume spike of the decade following earnings. Good setup to my opinion.

Another issue with the stock is visibility. We’re talking about a Norwegian small cap & price action mostly moved on earning days. Boredom is a bear case and we could have to wait weeks with no price action until volatility kicks, down or up, during earnings. Under the radar opportunities need to shine to be bought.

I personally bought a starter position of ~40% final allocation. I’ll continue adding the next months. Only shares. Small-cap, uncertain timing, not worth boosting with option risk on top. I believe this could become a nice 2026 play as AI democratize outside of ChatGPT and demand for wearables is very healthy and growing. It seems like a great set up from all angles, assuming one can be patient enough to hold until the catalysts materialize.

This closes my review of Nordic Semiconductor. Hope you enjoyed it; if so, feel free to share your thoughts or give it a like. I’ll see you for the next one, have some things up my sleeves for the coming weeks!

——————————————————

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

Interesting idea and investment thesis. We complain daily about battery life, yet so few look into companies that can solve that. Thanks

Great find!