Transmedics Q4-25

When nothing is good enough

If you do not know TransMedics, everything you need to understand the company can be found here.

This quarter was excellent. The company delivered everything I expected and a bit more. I’m baffled by the market’s reaction even though it is a bit too early to draw conclusions only a few hours later - and it has its reasons.

We are not seeing competitive dynamic impacting our ability to execute in 2026 and beyond, and I will leave it at that.

Fundamentals.

The business is stronger than ever in every vertical and the bull case is not only alive, but strengthening each passing quarter. The company closed FY25 with 5,139 OCS case used compared to 3,735 in FY24, meaning approximately 38% YoY increase in transplant volume using TransMedics, growing their market share in liver & stable in heart - which should change with the new OCS.

For liver, in 2025, OCS liver transplant represented 4,197 transplants, or 36% of the overall liver transplant volume in the United States. That is up from 26% in the same period in 2024. For heart, OCS transplant represented 854 cases, or approximately 18% of the overall heart transplant volume, and modestly up from the 17% seen in 2024. For lung, the numbers are small. OCS lung transplants represented only 88 cases, or approximately 2%.

This represented approximately 26% of the total 19,833 U.S. transplants for heart, lung and liver combined in FY25, up from 20% YoY.

Importantly, for the third consecutive year, we saw growth in overall U.S. liver and heart and lung transplant volumes... We strongly believe that the OCS NOP once again played a key role in driving overall liver and heart market growth due to the increased use of DCD and DBD donors in the U.S.

This data is enough for us to conclude that TransMedics is everything they claim to be. A safe, trusted and efficient hardware for DBD and DCD which practitioners are using and trusting more and more.

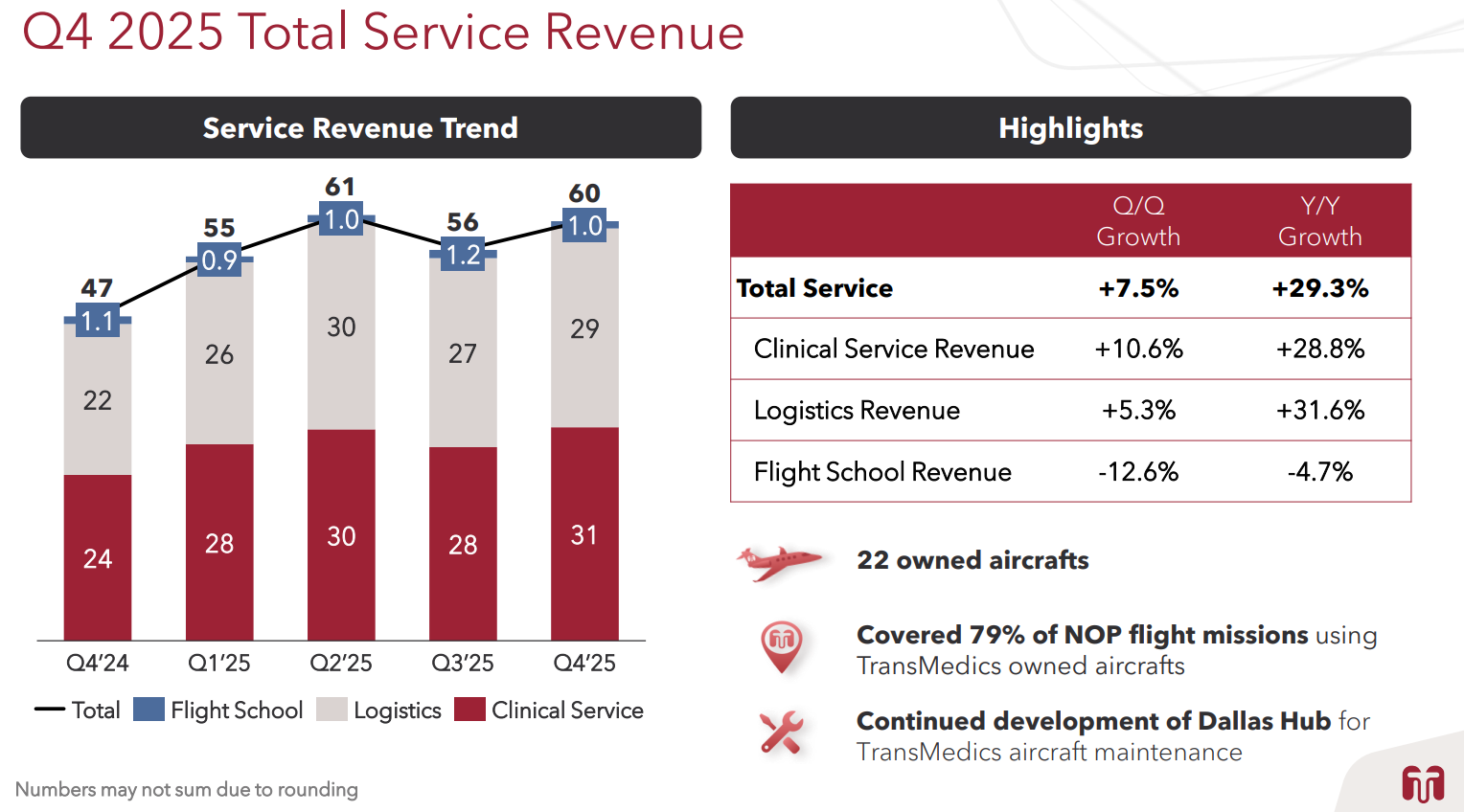

Besides the OCS itself which has proven and continues to prove itself, their service is also healthy in terms of growth with stable demand for transportation and clinical services; a 30% YoY growth for the second quarter in a row, confirming not only the demand for OCS cases but for the end-to-end service.

TransMedics didn’t need a proof of concept but seeing that kind of growth for a new and innovative end-to-end transplant service is very positive for the future and for its expansion in Europe as the need for transplant systems is the same around the world.

Speaking of Europe, it is interesting to see that since management said they would focus on the region for their hardware and plan their expansion, revenues rocketed, notably for their core product: OCS liver.

This isn’t anecdotal, it shows the clear strategy of expanding its service overseas and this should only accelerate while the potential is really large the old continent.

This program is actively launching in Italy, and few other European countries have expressed strong interest in exploring the NOP model in their local geography.

Expanding our commercial activities in Europe has the potential to nearly double our transplant total addressable market for TransMedics.

We’ll talk numbers later but fundamentally, my bull case written more than a year ago is perfectly materializing, maybe even better than what I expected back then.

Future Growth Levers

We did not have much news about the next growth levers, except to recall them to everyone’s memory:

European expansion ongoing & expected to be meaningful in terms of revenues by H2-26.

Heart and Lungs OCS trials ongoing in the U.S. unrestricted with great feedback so far, but it remains early to be overly optimistic.

OCS Kidney in preparation for FY26 to require FDA approval early 2027, unlocking a massive market as TransMedics continues to earn the trust of practitioners with other products and will logically use OCS Kidney when available considering the success of other OCS.

To our knowledge, the OCS Kidney will be the first and only warm perfusion oxygenated kidney platform for kidney transplantation used from the donor to the recipient.

OCS Gen 3 which is in parallel to the OCS Kidney although the OCS Kidney would already be Gen 3. Improved hardware, smaller and more efficient at controlling organ quality with more automated systems.

Those four points will require investments and that’s something we will talk about in the financial part of this write-up, below, but they should all be in full swing by 2028, earlier for heart, lungs and Europe, and contribute meaningfully to the company’s revenues.

Some interesting quotes though about the trials as management is facing some issues to move forward with the phase B of the trial.

Part B is designed to allow OCS to gain a potential new clinical indication in DBD heart transplant segment that are sub 4H preservation by demonstrating superiority of outcomes in a head-to-head comparison to current cold static storage modalities.

Progress in Part B has been slightly impacted by a competitive dynamic as it relates to cold storage arm of the trial. Specifically, there is a hesitation amongst competition to a head-to-head comparison between OCS and their static cold storage modality.

This is a CEO talking so I can understand why some wouldn’t take those words at face value. But I also can understand why many would refuse to compare their systems to the OCS as when we see the growth and demand for the product, we can understand there is something practitioners like about it.

What’s coming is really the unequivocal, drop the mic, statistical superiority in the most important outcomes after liver transplantation, which would justify and support all the evidence that’s been built in having more than 14 or 15 publications now already in print, out there. Those publications that are coming, they’re aggregated of thousands of cases, they’re coming out of our registry, and many of them are already under review.

Waleed said that publications were coming H1-26 for liver OCS while the rest would take longer. Hopefully those will be out soon.

Financials.

Now, we saw that fundamentally, everything was going good to great. But as usual, and I hope you know it by now, the market cares only about… Cash generation.

And even there, TransMedics has been nothing but excellent.

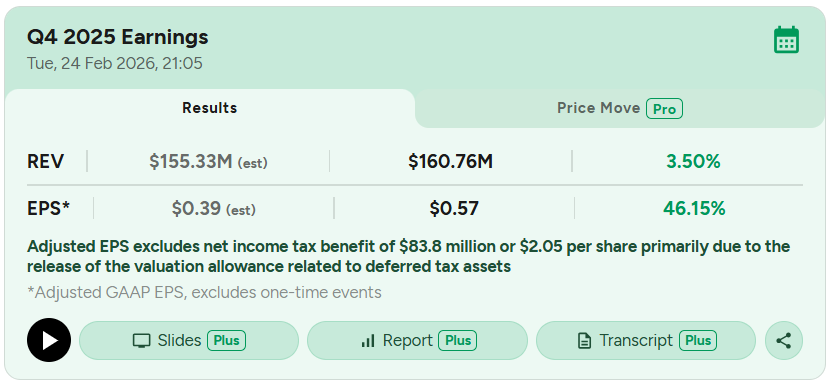

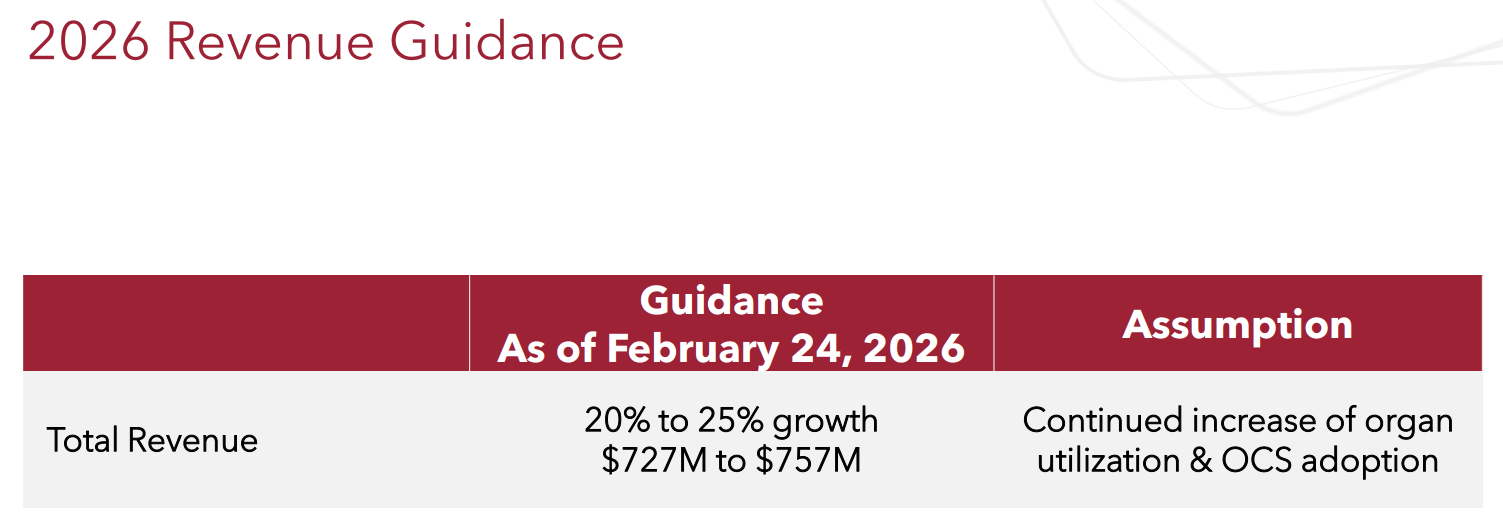

Revenues beat the Street expectation at $160.8M, up 32% YoY and at $605.5M for the year, up 37% YoY. As a reminder, the FY25 first guidance came in at $575M and was raised three times through the year to $600M. Management raised their guidance three times in three quarters and still beat it.

On the “less good,” which I personally do not consider less good because of context but needs to be said, margins are slightly declining.

This is normal. As their service revenue continues to grow, their expenses also do but this is the counterpart of growing market share and a better service. Without those, TransMedics wouldn’t have comparable revenue growth nor market share.

Add to this rising expenses for trials, next gen OCS and European expansion. As I said earlier, this costs money but it will yield constant long-term growth in return & signs give me reasons to be optimistic; when market share rises in a sector like healthcare, your future products have a large head start as trust is already built.

We also need to understand that those expenses are one-off expenses. Once spent, the products/services built from it will be here and generate cash for decades. But it does require spending and this spending will continue 2026 as it will be the year of innovation, with all projects running during the period.

Based on the current revenue guidance for 2026, we expect operating margins to be approximately 250 basis points below 2025 full-year levels, primarily reflecting the timing and scale of these investments.

As investment levels normalize and the business continues to scale, we will expect operating margins to resume expansion. We continue to expect operating margins to approach 30% by 2028

Once we complete those elements, that’s what gives me the confidence that spend should normalize, and then we should be able to start capture and operating leverage as we continue to grow.

So yes, cash generation wasn’t the perfect case and won’t be in FY26. That being said, we are talking about a company with $107M of income, up 203% YoY - excluding the tax benefit, with approximately $440M of net cash which will also help on CapEx. The progress has been very impressive and the results even more.

We are talking about a company which wasn’t fully profitable a year ago and now runs at a run rate of 30% revenue growth with ~13% net margins, earned the trust of many practitioners in a very complex sector and continues to push to expand.

Guidance.

On the main meal, which once again is not falling short of expectations.

Keep in mind FY25 early guidance, read those comments from management.

In our guidance, we factored in all of the above, and issued what we believe is a realistic guidance that would enable us to execute and let the execution and performance dictate what do we do, or if we need to revisit the guidance.

We feel confident on the guidance that we are putting forth here, as it bakes in all the uncertainties, all the opportunities and uncertainties in front of us.

You know, again, we will go and execute, and we let the execution and the results and the performance dictate, if we need to revisit the guidance as we move forward throughout the year.

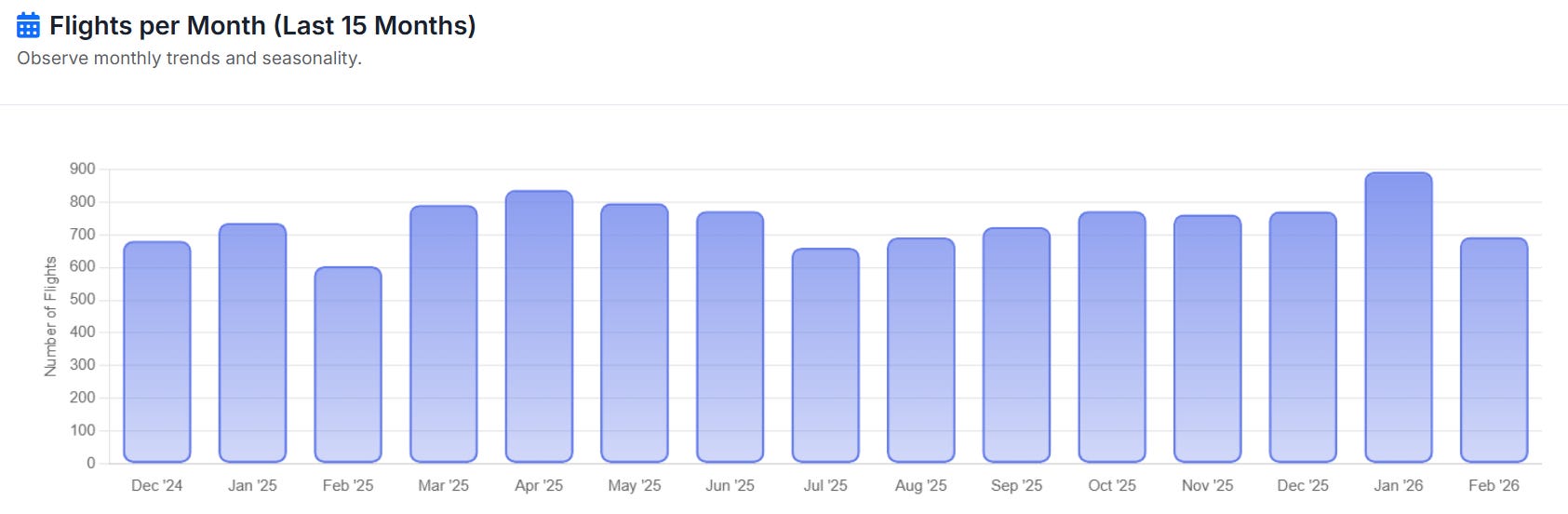

And look at the flight profile of the first two months of 2026, which according to my methods - which has always found the revenue floor of every quarter for more than a year now, should put TransMedics at approximately $110M of revenues with 37% of the quarter left to go.

Management is conservative by design; they learned their lesson in 2023. Seasonality is complicated to anticipate and it is better to overdeliver than overpromise.

Will they? I don’t know. No one does. But I won’t be surprised if they raise guidance through the year, even if the market would have loved a strong guidance today.

So… Why is The Stock Red?

There are no valid reasons in my opinion and we’ve seen that the market bought the stock today, passing from -7.5% to -0.9% at time of writing. There’s demand at today’s price and that’s what I’ll conclude later. But it’s important to remind ourselves that our opinion just doesn’t matter.

And we have to remain factual and keep our feet on the ground. The market, even if it sees the positives, focuses on the negatives. And there are two.

The margin pressure is real and will persist through 2026 as detailed above.

The company has execution risks: the trial results are still pending, even if the first feedbacks are positive, OCS Kidney is in development, European expansion will require expenses before yielding results - even if it takes only one semester.

TransMedics has execution risks which comes with shrinking margins in the meantime. The market is not punishing the stock, it is simply acknowledging the risks, the “what if it doesn’t work?”.

That being said, we’re also cognizant of operational challenges that could influence the pace and timing of these initiatives.

First, as stated, we are still building out our logistics infrastructure in Europe, which could moderate the initial pace of our EU NOP launch as we ensure we have the right foundation in place.

Second, timing of the full De Novo trial accrual will depend on how long and how the lung transplant market adopts machine perfusion and NOP, which remains to be proven.

Third, timing of Enhanced Part B completion will be influenced by some of the inertia created by competitive dynamics for the cold storage arm in the marketplace.

Fourth, the very common and now, I hope, well-understood annual phenomena of potential Q3 seasonality in U.S. transplant market that temporarily slows down transplant activities.

Finally, ramping our infrastructure and clinical staffing to meet the growing demand for OCS NOP will be critical to achieve our full growth potential in 2026.

The market is always worried about spending, even if we are bullish and if the team has proven to be great at executing. The advantage with TransMedics is that their plans have deadlines. Europe should give results this year, like the trials, and the OCS kidney should be approved before end of year. This isn’t a story of “we don’t know when,” this is a story of “give us two or three quarters.”

Personally, I continue to believe TransMedics is insane value at today’s price and it is the kind of stock I want to own: fair price, perfect execution, massive potential. We also had talks about integrating official government workflow which I talked about already and would honestly make sense considering the product.

Specifically, we are exploring if TransMedics can be a more integrated contributor to the national transplant ecosystem in the U.S. The goal is to maximize donor organ utilization for transplantation and continue to save more American lives and save significant healthcare dollars.

This is a long shot but one more example of the opportunities such company has.

As for my valuation model of TransMedics, which expects ~$1B revenues FY28, I stand by it today, after what I saw and the FY26 guide. My bull case with great execution pushes up to ~$1.3B of revenues by then and could happen if Europe picks up rapidly on a clearly superior technology and yields its expected growth.

As for the market, I continue to believe 7x sales is below what TransMedics deserves even with execution risks & potential margin pressure. But the market isn’t rewarding anything below perfection anymore, so we’ll maybe have to be a bit more patient on this one, until perfection happens - the European expansion yielding results would already be a great sign.

In the short term, I’ll wait to see what the next days offer. It is disappointing so far but again, there is clear buying pressure today at this price and it would be surprising to go lower on such a print for a defensive name, but who knows... I also know most data platforms are displaying a wrong EPS print due to miscalculations, which could impact algo-trading and explain the weird +10% to -7% swing post-earnings. Who knows? I wouldn’t enter into that kind of speculation, though. Let’s wait and see the next days.

The long-term goal remains Intuitive Surgical, a company growing ~20% CAGR with a very comparable profile in healthcare and 30% operating margins... Trading at 17x sales and 62x earnings. This is what a deserved healthcare premium is.

If TransMedics were to execute on its promises by FY28, this is what it could reach.

——————————————————

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.