Transmedics Valuation & Position Review

What to expect from the company by FY28

I’ll do something different today, something you’ll see more often as I concentrate both my portfolio and content around a few key names, with much more detailed follow-up on fundamentals, valuation and investment execution.

TransMedics is my largest position, about 40% of my portfolio in shares and calls as of this writing, and I still sleep like a baby. I’ve called it multiple times the best buy in the market and it’s finally starting to prove it. We’re still far from calling this trade an overwhelming success, but we’re getting there.

For now, I’ll detail what I expect for Transmedics’ next years, why I intend to hold my position and how I plan to manage my investment based on those assumptions.

I’m not here to guess TransMedics’ future stock price, but to detail why I believe the stock remains an excellent opportunity & therefore is worth holding at today’s price.

Transmedics Valuation.

If you’re subscribed and still don’t know TransMedics… well, everything is here. And you’ll find the detailed last quarter review here.

Before Starting.

The biggest limitation when valuing Transmedics is not having access to.

Clear quaterly or yearly data on transplant volume per organ.

Clear quaterly or yearly data on market shares per organ.

Clear quaterly or yearly data of service/product price per organ.

We also have many variables & external factors that could influence TransMedics, positively or negatively:

Market share dynamics & potential acceleration due to DCD

Global transplant volume growth and DCD impact

European expansion execution and regulations

Next Gen OCS services and products pricing

Kidney OCS commercialization timing

European service pricing

Those cannot be factored in with clear data so I’ll let you use your discount rate after my valuation to factor them as you see fit.

Methodology.

In 2023, management disclosed their market share per organ, perhaps the first and last time they did so. I built my assumptions for pricing per organ based on those market shares and public U.S. transplant data.

The transplant volume aligns with management’s FY23 total OCS case used of 2,347 so my math must not be that far off. The company generated $241.6M in FY23 or an average of $102,940 per transplant.

Moving into 2024, one major change happened: the scaling of their NOP platform and of the additional services offered. This increased pricing per organ as they sold more than “just” OCS products and demand followed.

At year-end, management reported 3,715 OCS transplants generating $441.5M, an average of $118,843 per transplant. A clear rise in service usage compared to 2023, when NOP was still scaling.

Management confirmed during many different calls that pricing was stable YoY which means the increase in price per transplant did come from growing usage of new services.

From here, assuming the average price per transplant rose 15% (the increase between FY23 and FY24 averages), we can estimate new prices per organ transplant and FY24 volumes.

This is where my assumptions aren’t perfect anymore. The volume modeled comes to 3,554 OCS transplants, about 150 fewer than management reported at year-end FY24. This suggests my pricing is slightly off for one or more organs, likely a bit higher than reality. To align with official FY24 OCS case data, I’ll reduce each by about 2%.

These are assumptions. They aren’t perfect. But this framework is probably the closest we can get to modeling Transmedics’ pricing based on public data.

From here, my methodology is simple: I assumed pricing per organ, use public UNOS transplant data and growth trends to project future transplant volumes, and attribute market shares to Transmedics under different scenarios to model revenues.

YTD Assumptions.

FY25 is almost over; if we take YTD data with FY24 assumed pricing - since the service proportion of revenues has been stable this year, market shares appear to be growing except for lungs.

With the next-gen OCS in clinical trials for hearts & lungs, and with improving market shares on livers, we can imagine what will happen if both were validated by the FDA with positive results.

Growing confidence in hardware that can manage multiple organ conservations will certainly drive more demand, as it will require less training, lower hardware expense and a consistent framework with a single partner for different organ procedures.

This would be the logical trend.

U.S. Revenues.

Looking ahead to the next years, few important factors to take in consideration first.

Transmedics enables DCD, which means an acceleration in volume growth as more patients become eligible to be harvested. But future growth rates are impossible to predict as this remains a new practice.

Service pricing for hearts and lungs could increase with the next-gen OCS, since those organs are costlier to maintain than livers, but without any ideas of the potential increase - if any, I won’t factor in at all.

The next-gen OCS might not be approved or not yield above average results and therefore not yield market shares increase in heart and lungs, nor growing DCD volume for those organs.

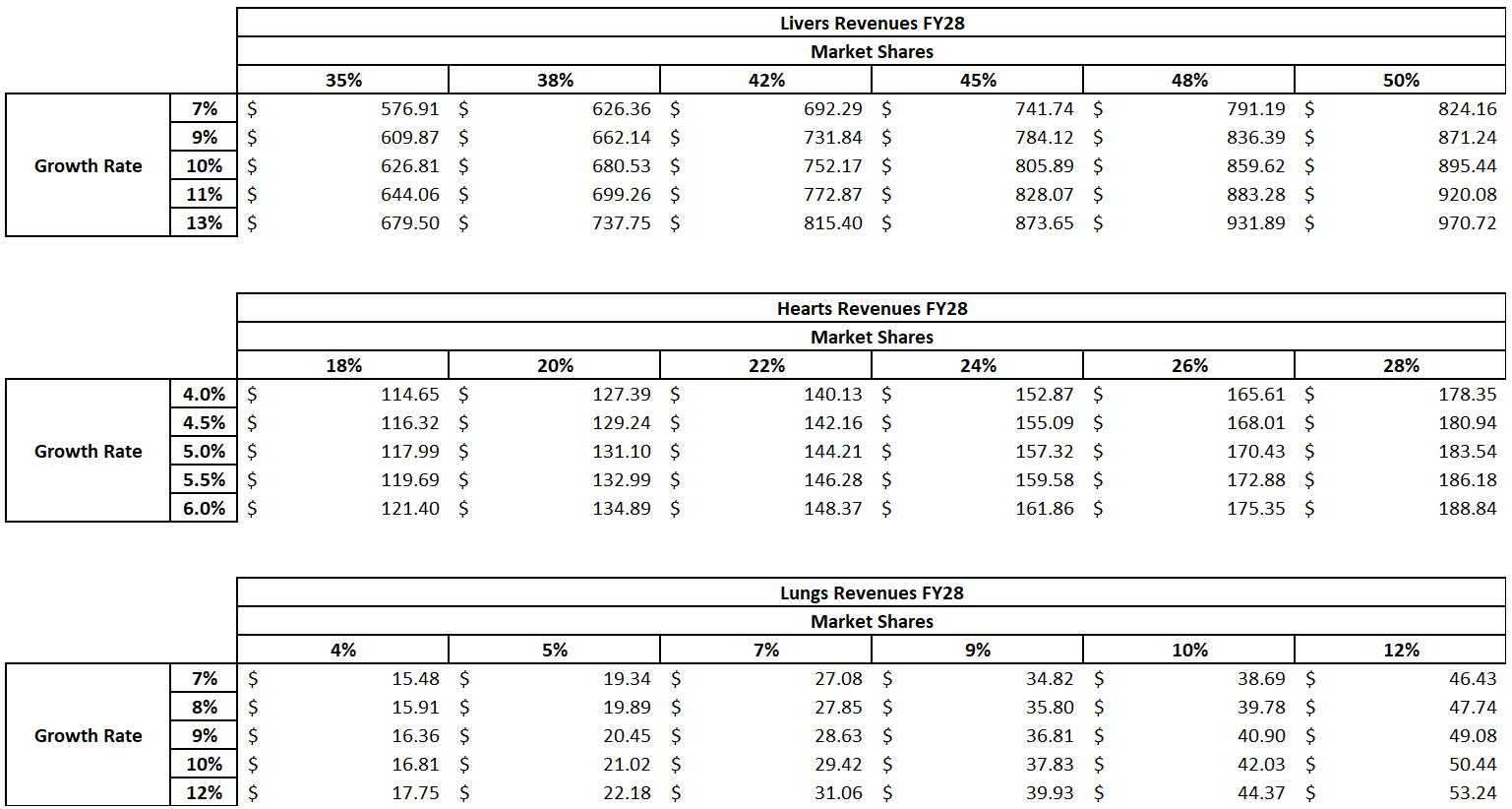

Here are U.S. transplant growth rates over the past 5 years and 2 years, showing clear acceleration due to DCD.

Hearts: 5.26% & 5.48%

Lungs: 7.89% & 11.39%

Livers: 7.72% & 9.61%

Assuming the last two years’ growth rates as a base case & varying market shares per organ, we can project potential revenues for TransMedics through FY28 based on the earlier FY23/FY24 pricing assumptions.

The main takeaway: livers remain the bread and butter for TransMedics. It’s critical for the company to keep gaining share in this market, which should continue as the hardware proves itself and more practitioners rely on it for DCD - and DBD as it means consistant hardware usage, harvests.

This leads to a FY28 midpoint of $963M in revenues, a 20.79% CAGR from LTM U.S. revenues, with revenues probably closer to $850M - $900M assuming the next-gen OCS heart and lungs were not approved by the FDA and continuous market shares growth in the liver market.

Yes, growth slows, but that’s normal. Scaling a $600M revenue company is different from scaling a $100M company.

And there are other growth levers at play.

International Expansion.

Again, some important factors cannot be modeled:

European pricing could differ from U.S. pricing, though overall transplant costs are comparable between the two continents.

Expansion success will depend on execution and external factors like adoption and regulation.

All considerations that apply to the U.S. market also apply in Europe.

European expansion is expected to begin in H1-26 with 4 hubs in Italy - Milan, Rome, Padua and Bari, providing access to central and southern Europe through third-party flights until TransMedics builds its own fleet.

I believe adoption in Europe should be faster for several reasons.

Management experience in organizing, scalling NOP and managing a fleet.

Smaller market and geographic area to cover compared to the U.S.

OCS is already in use in the U.K. hence regulatory approved.

OCS already passed many certifications from other European countries.

Trust built from years of concrete U.S. data proving OCS performance.

For context: NOP began scaling in the U.S. in early 2022. By 2023, two years later, Transmedics had 14%, 16% and 4% market share in liver, heart & lung transplants respectively, with 17 centers and 22 aircraft.

This was achieved in two years without historical data to back performance, the FDA trials helped but they had to make their reputation in real time.

By end-2028, I assume TransMedics’ penetration in Europe will at least equal FY23 U.S. penetration per organ, potentially higher for the reasons outlined above although lots of questions remained around execution and adoption.

I still model lower penetration to remain conservative and factor in potential setbacks.

Transmedics has worked in Europe for years. Adoption was slow because the company didn’t focus on the region. Now they do, with a much stronger position and capacities than a few years ago.

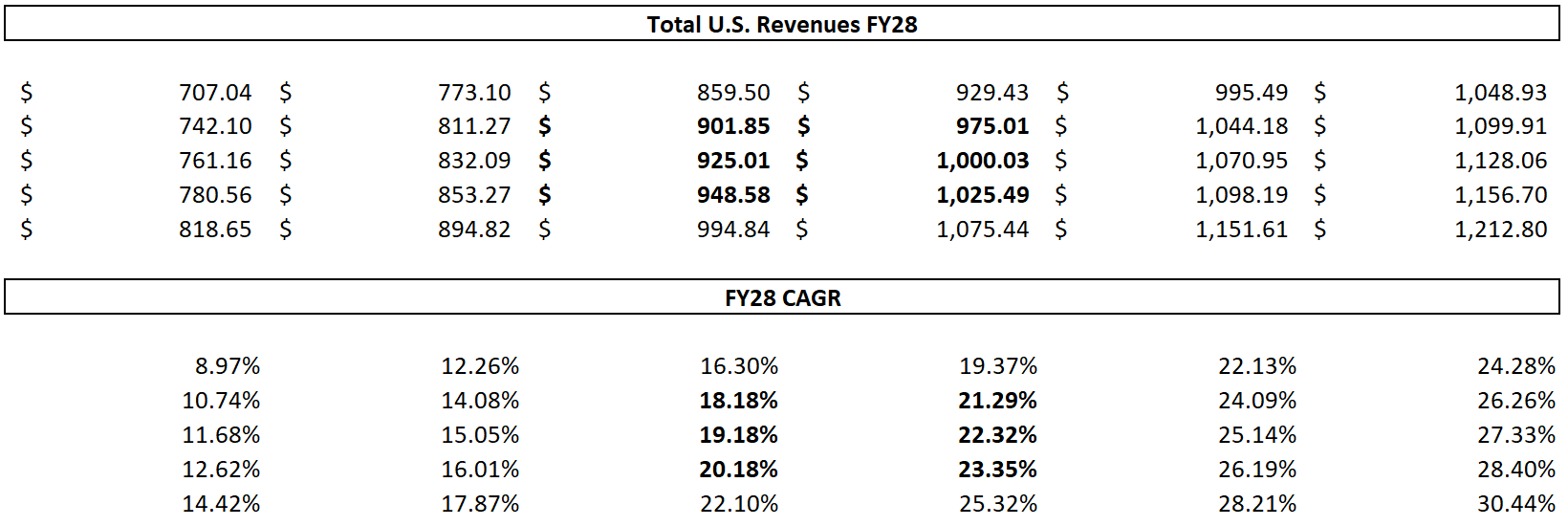

That would yield revenues with a midpoint of $421M, implying ~199% CAGR, as the business outside the U.S. is essentially nonexistent today.

Other Growth Levers.

TransMedics originally planned to expand to kidneys by 2028, but the timeline has been accelerated. They now plan to unveil their kidney OCS in H2-26 & start trials by 2027, which means revenues could begin by then.

I won’t try to model this, as pricing assumptions and penetration are impossible. But assuming favorable rulings and FDA adoption post-2027 trials, the kidney OCS could scale as early as 2028 with demand boosted by Transmedics’ network effect. Market share could grow quickly in a 27,000 yearly transplant market - and rising, not even including the European market.

Transmedics Group.

If we aggregate assumptions for the U.S. and European markets - without factoring kidneys, we reach a FY28 revenue midpoint around $1.383B, implying a 32% CAGR from FY25 midpoint guidance of $600M.

Which could be lowered to $1.2B assuming no market share gains in the U.S. heart and lungs market due to the potential reject of their next gen OCS, implying a 25% CAGR.

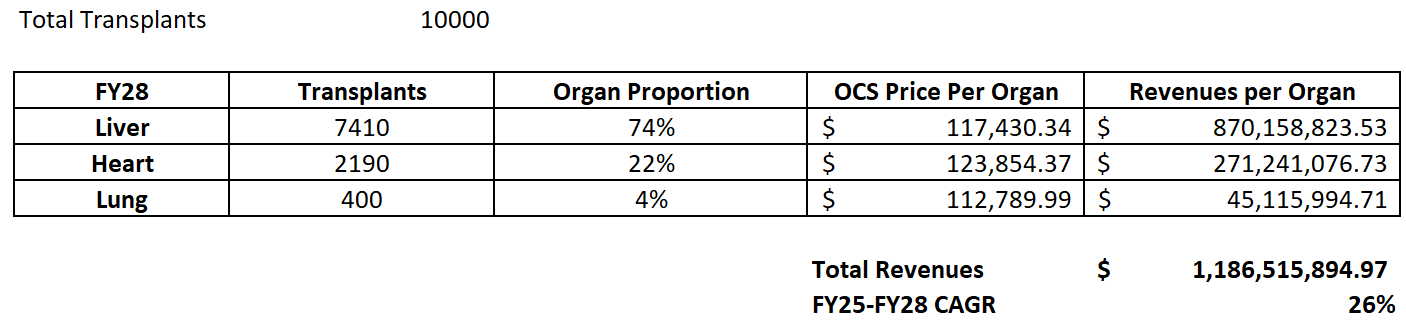

Worth mentioning: TransMedics shared a plan to achieve 10,000 yearly transplants by FY28. Assuming the same proportion of transplants and price per organ - which is unlikely, here’s what we could expect by FY28.

Lower than my base case assumptions and much closer to my non next gen OCS approval model; still very encouraging.

Stock Price.

This is probably what interests most of you, but let me stress on thing: assumptions are the most important part. Understanding the business and what could affect future revenues is what matters as it is what the market will focus on.

This valuation exercise is not about finding the perfect number. You shouldn’t look at the highest price and think, “damn, the gains I could have if this were true!”

No. The point is to build models that factor both bear and bull cases, understand the why and how so we can focus on controlling the business’ direction and focus on the minimum requirements for Transmedics to deliver solid returns.

For my price assumptions, I included a 1.5% dilution by 2028, hence a total of 35.73M shares by then. This could grow if management decided to dilute further to finance European expansion. I don’t expect it as they now generate enough cash to self-fund, but it could happen if they wanted to be more aggressive.

The growth rate is the base case used in the FY28 revenue projection. The P/S range between the Transmedics’ lowest and its 2023 high, with 12 as the median since IPO.

The reason I’m bullish on TransMedics isn’t because my base case scenario would yield 40%+ CAGR from today, nor because my most bullish case would yield 93.57%.

The important question is: what are the minimum requirements for correct returns?Keep in mind that my assumptions are biased bullish - not very conservative.

Continuous growth from DCD volume.

Rapid European expansion.

Next-gen OCS adoption.

No, what makes me bulish is that based on this model - which has imperfections, I’d need TransMedics to grow at 15% and trade at a minimum of 7x sales to outperform the S&P’s 10% average.

Does that growth rate seem unreasonable? Not at all. It could be achieved in many bearish scenarios, like the non approval for the next-gen OCS or a much slower than expected adoption in Europe. Heck, it could be achieved only with an hyper focus on livers as it represents around 45% of market shares in the U.S. market. Some verticals could go wrong and Transmedics could still achieve that growth.

Does 7x sales seem exaggerated for a company growing 15%? Intuitive Surgical grew around 20% with a median P/S of 11x over the last three years. Here are some other healthcare examples.

The average of those examples would require Transmedics to grow at 20% CAGR up to FY28 to deserve an 8.67x ratio.

Does 20% CAGR seem out of reach for TransMedics? It’s still below my base case, so my answer is clear. It is a growth rate which could be achieved without next-gen OCS and with a stable European expansion. Or achieved only within the U.S. market with next-gen OCS adoption and increasing market shares.

But one has to happen. Which gives us what we need to look at at a bear minimum to remain bullish on Transmedics future.

This is what matters in those exercises. Understand what to look at and what will be important to control. In Transmedics case, the European expansion or the next-gen OCS approval have to happen for the stock to remain a great hold.

Final Words.

Once again: the conclusion should not be that TransMedics will reach $1,000 per share by 2028 in the best case. Not at all.

It’s that even if everything doesn’t go perfectly, TransMedics should not be considered overvalued today and still has upside. Even more if everything goes as planned. The company has multiple growth verticals to justify revenue expansion & higher multiples.

TransMedics is around 40% of my portfolio at an average of $106.86, excluding option calls with strikes at $120 and $150 by January 2026.

My plan today is simply to hold.

Price action has been pristine and we are past the perfect accumulation point. We could see a deeper retest of the breakout, down to daily averages around $130. I would buy that retest, assuming no negative news.

If the retest doesn’t happen and we continue higher in the coming weeks, we’ll need to be ready for the $150 breakout to be retested at some point. That could also be a great entry, but I won’t speculate on what I’ll do then, it will depend on timing and context.

So, except for the $130 retest scenario before year-end, I’ll sit on my hands and wait for the new ATH, which should come in the next months as flights remain strong going into December, historically the strongest Q4 month.

Appreciate the thoughtful analysis!