The SaaSpocalypse is Justified, Here's Why

Why the market is done rewarding legacy SaaS and how to profit from the wreckage.

I have been going against the crowd for some time now, with the refocus of my content end of 2025, articles going against social media’s darlings - for good reason as the average performance of this basket is -25% in ~3 months, or with article preaching the respect of price action instead of DCA.

Not really what works on social media and as a fact, it cost me ~300 subscribers since the start of the year, who decided that my content was not for them as I did not want to participate anymore in this confirmation bias echo chamber X and Substack are slowly becoming. And it served me right - and you who chose to stay, as my stock picking delivered ~40% alpha YTD - which is pretty massive and you can follow it all for free here.

This article is just one more of those going against the crowd as trying to justify the current SaaS sell-off in an environment where most are saying those stocks are lifetime opportunities won’t make me more friends.

But I’m here to make money, not friends - although I’d love to make both. So let’s dissect what is happening on the SaaS sector, why, and how we will profit immensely from it, when the time is right - not before.

SaaS What?

I’m not sure everyone knows what a SaaS is so let’s start here as it is key to understand why they are dying. Software-as-a-Service.

Say, you have two ways to eat nowadays. The “normal” way - at least for me, is to go do my own shopping with my small legs and wallet, come home, turn on the gas, cut my vegetables or season my beef, cook it all and serve hot. The “occasional” way is to take the same legs but go sit at someone else’s table who’s going to ask me what I want to it, prepare it for me and serve me. And if I want salad instead of fries, or to remove tomatoes from my burger then sure, the cook will comply.

This is a SaaS; I do nothing but pay and consume. Someone else works at making it good enough so it is worth my money, and I just have to ask for what I want within the circle of competence of the provider - you won’t ask for caviar at McDonald’s.

Adobe is a SaaS, they allow me to download and use a software with built in tools, a certain degree of personalization but no control over the core code. I can use it myself and that’s about it, just like I can eat a restaurant’s food but can’t go in the kitchen to cook my own steak.

SaaS companies give you access to a controlled environment with pre-defined access, liberty and customization.

Most SaaS are meant to resolve pain points - which is key to why they are being sold off nowadays as AI is just better and cheaper at doing so, with the bonus of even understanding context. Some smart guys found out there was a strong need for a service which was complex or costly to set-up and built a generic system to resolve this particular one, sold it, improved it, expanded, etc…

Take DocuSign. The founders understood early the need to sign documents remotely, that moving our small legs with a pen on our pocket would become a pain point in the years to come; they built a service to sell trust online in the form of a document signing platform, integrated different document formats to heal their users’ pain points - and generated $3.22B of revenues FY25 by doing so.

Not bad, eh?

The entire SaaS sector relies on a handful ground rules.

Resolve a pain point many will accept to pay for.

Grow user base, revenues and margins.

Optimize and improve the service for retention.

Drink margaritas.

The SaaS sector is unforgiving before reaching the margaritas as everything depends on how fast it scales, retain users and prices its service. SaaS rely on massive volume demand to resolve a pain point and the value clients agree to pay for it to be resolved externally.

The SaaSpocalypse

This is the name given to the so called “silly” sell-off of the SaaS sector - which isn’t silly at all as I am about to explain.

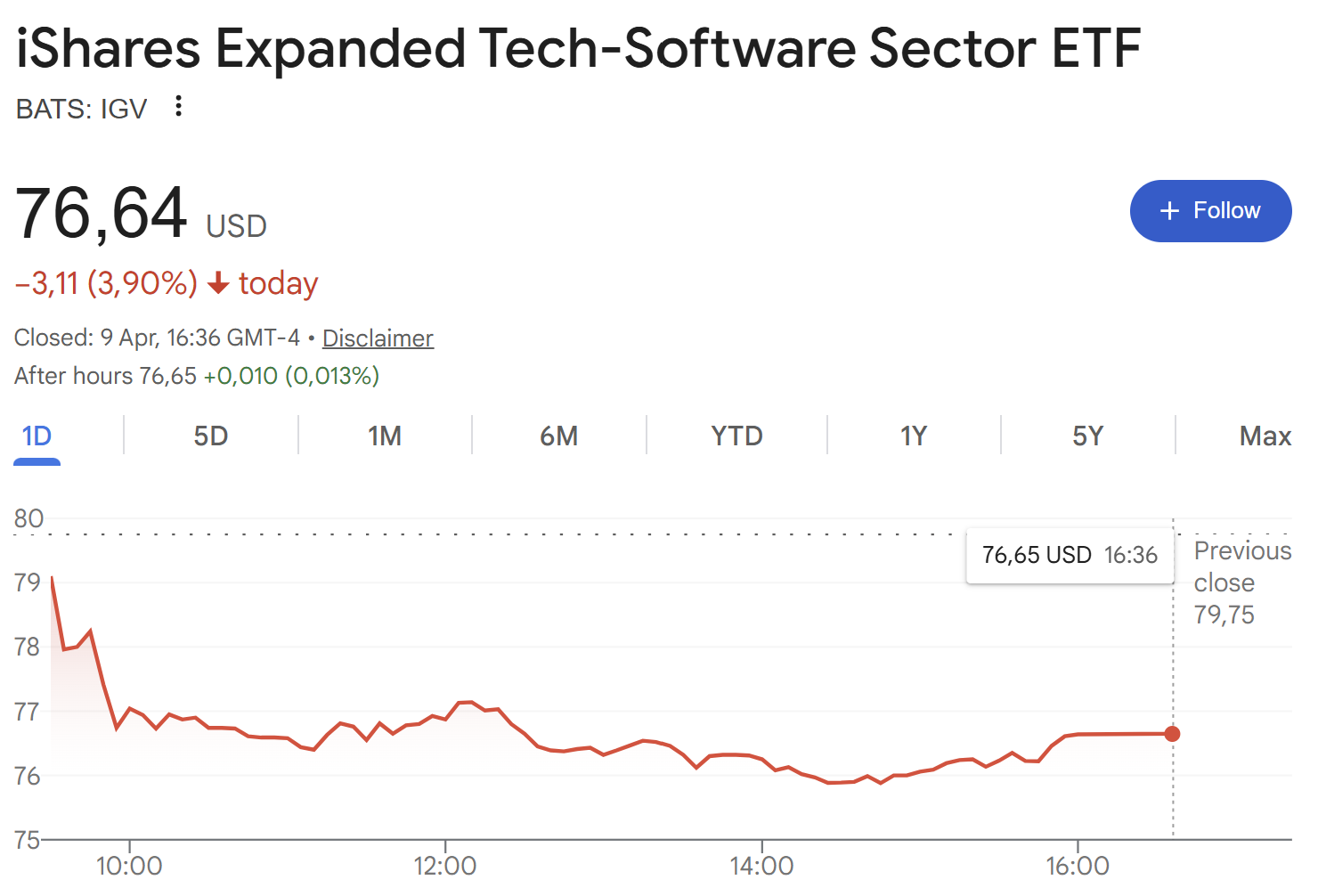

The SaaS ETF, IGV, is down an astonishing 25% since January. We are talking about an ETF here, not an individual name; this should give you an idea of some of the losers’ performance… We’re talking about casual -50% YTD on Duolingo or AppLovin’, and more… Some portfolios will take years to climb back this performance.

A literal bloodbath cause by AI, with reasons.

Let’s start with a few words to remember what the market is about: safe and growing cash generation, right? You’ve heard me say this so many times now - details on this write-up.

This is how the market works. Understanding this helps avoid value traps; companies that look cheap but have no path to margin expansion, revenue acceleration, or gain the market’s trust. Without a catalyst, the market simply walks away. A value trap can become a winner, but it needs one of those triggers first.

We don’t buy those. We look for the names the market is about to fall in love with; companies that can accelerate growth or increase cash generation, creating a double appreciation: rising cash and expanding multiples.

That’s what stock picking is about.

The SaaS sector has been rewarded by high premiums for two decades because they were the only economically viable solution to structural pain points. If a company needed to sign 10,000 documents per day, it was cheaper to contract DocuSign than to develop and maintain an in-house software, just like it’s easier to pay a bit more to go to the restaurant than to cook sometimes.

This created an entire sector where winners had a strong, safe and recurrent cash generation. As long as the pain point existed, companies would rely on the company which solves it and as by design, successful companies grow, their usage of pain point resolution increase and SaaS revenue grow. With stable margins also comes increased cash generation, etc… A virtuous wheel which pushed the market to increase those companies’ premium while fundamentals were improving.

Take Adobe as an example.

The stock’s multiples followed free cash flow margins to perfection through the years, up and down alike, until… 2025. This is where we’ll need some critical thinking. Most stop at “what was will be again” and buy those stocks. This is the problem of fundamental investors: they look at the past only.

But the world moves forwards, thankfully, and what was could not be anymore. You do not ride a horse to go to work nor wash your clothes in the lake. What was eventually stopped to be when new technologies disrupted old methods. And that was for the greater good.

This is what the market is pricing now.

What is AI?

We’ve already answered that question many times from a technological point of view, but never from a usage point of view. Artificial Intelligence is an automated and intelligent tool which can be used for any kind of tasks, including… resolving pain points.

A versatile technology trained for everything whose progress has been baffling, especially these last few weeks/months. I mean, I am a nerd and most of you also are - that’s a compliment coming from me. We are aware of the new technologies and developments; heck, most of you read a 15min write up about photonics. Only nerds do that, most people I spend time with daily have no idea that the word “photonics” even exists.

I use AI every day now and see it improving each passing week, I see answers, services or corrections I was frustrated not to have six months ago finally happen. We all see Anthropic’s new Claude releases, monthly, shipping new functionalities like if they were socks, and how transformative they have been - notably Claude Code with most CEOs telling us than a significant proportion of their code is now written by AI.

I’d say maybe 20% to 30% of the code that is inside of our repos today... are probably all written by software.

Satya Nadella, Microsoft CEO

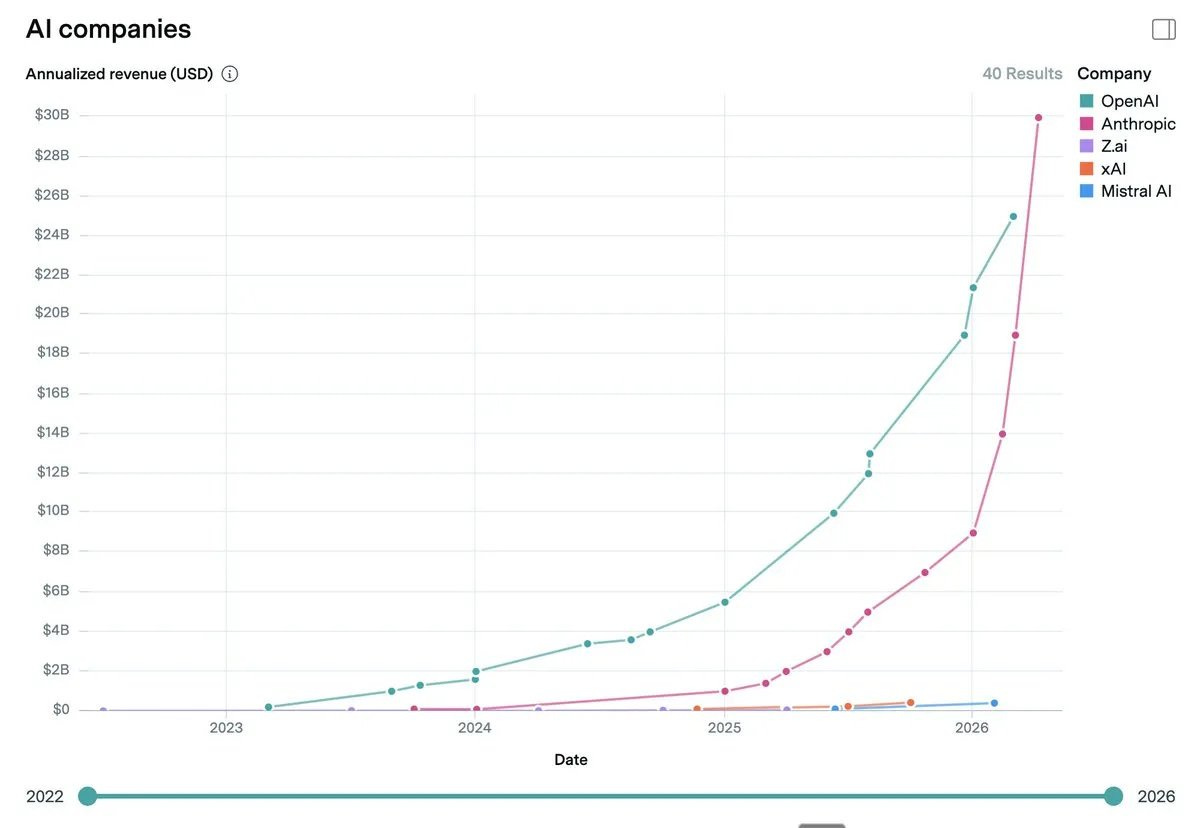

Over the past 6 months, I built 3 websites and ~100 scripts for automation tools for my investing, writing and research. I could never have done so much before. This made Anthropic the fastest growing company in history, reaching a $30B run rate in less than 3 years of activity while ChatGPT continues to scale and without including Gemini or other AI functionalities and compute demand.

AI is baffling and its progress is even more baffling, to the point that this week Anthropic CEO said they developed a security focused AI model called Mythos, which was so performant they couldn’t release it to the public for fear it would be too easy to use it to hack into current system and decided to team up with security specialists to avoid this situation and find a way to integrate this model for defense first.

This is AI. This is a massive structural shift improving at the speed of light. And you guys want to tell me that what was true a decade ago will still be true in a year, while Palo Alto, which developed the most powerful and comprehensive security service is now being pushed to its limit by a new AI model?

Cmon…

The Disruption Risk

I will steal the wise words of a reader to go straight to the point.

The market correctly sees the risks (regardless whether the risk is justified or not which is a matter of personal opinion), and, as such, is no longer willing to give them premiums as safe, stable compounders. Hence the stock price crashed despite the numbers of most earning reports are still looking great…

The sentence in bold is the most important sentence on this entire write up. As always in the market, personal opinions simply don’t matter, and they don’t make money - not by themselves. You can take 1 year or 10 years to realize this, but it will still be true even with AI pace of progress because the markets are about future’s expectations based on individuals’ sentiments. Unless AI can predict the future, the market’s structural behavior won’t change.

Back to our the point and why the current SaaS disruption is justified: because AI is a structural change. What was a large pain point might just become a 10 days of work using Claude Code and what was 10M daily users might become 5M as AI agents replace workers - or hire fewer workers/consume fewer licenses, reducing retention, recurrent revenues and therefore cash generation, even if margins stay stable. SaaS mostly resolve tech pain points and AI will reduce the friction to solve pain points.

As for the argument “Don’t be stupid AI cannot build Adobe’s software”, it completely misses the point of what a disruption and stocks are. We are not talking about replacing those companies or software, we are talking about reducing the need for them which means reducing their cash generation.

Once more: the market only cares about future and safe cash generation.

Obviously, SaaS won’t die. Today, the market treats them all equally because it has no capacity to distinguish the future winners from the future losers. In doubt, sell everything, reassess in a few months.

Even structural AI winners like Palantir are being sold off while AIP is exactly what the AI revolution strives to create: an AI centric software.

And we’d expect non AI-centric names to thrive? No. The market has no view on what the future looks like for those names - neither you nor I do. We all have bias, opinions, but there is a possibility for 90% of nowadays’ SaaS to be entirely disrupted and rendered useless by AI in the next 5 years. You might judge it small, maybe even use the word “ridiculous”. But it exists.

I would never have imagined AI become so performant, so fast. Who says the next years will not again bring exponential improvements? What then?

The SaaS Future

Today, the market doesn’t see a future for those companies. It knows they won’t disappear, everyone knows that, but it has no idea what to do with them and so it sells. Liquidity goes away as uncertainty is real, whether we like it or not.

Obviously, SaaS will survive. Some, at least, maybe with another form, business model or value added. I cannot imagine Palo Alto or CrowdStrike be disrupted by AI as their cybersecurity service is more than just an AI model, and their need is exponentially growing with the democratization of AI ironically. These companies will adapt.

First, they will need to become AI native. I’ll always remember Brian Chesky’s words during an Airbnb earning call in 2024 about how this wasn’t a choice, but a necessity, while it would take a few years to get there as AI applications are structurally different from normal software.

The founder-led companies and the companies that are prepared to change and transform are the companies that are going to benefit from AI, because AI means everyone changes. And if you don't change, you're going to be disrupted... If you don't disrupt yourself, someone else will.

This is the first complexity, while model are by design AI-centric, SaaS have to pivot from classic software to AI-centric model, which makes them late by design; it’s always more efficient to build a house from scratch than to remodel one while being careful to keep the foundations and some furniture.

Second, resolving a simple pain point won’t be enough anymore. SaaS will need to create value which goes beyond facilitating workflows as this will be done cheaper and faster in-house with AI now. The cost and time of developing and maintaining a DocuSign equivalent got divided by 50x and will be even more in a few years; companies can’t compete on pricing with AI agents. The standards are different now.

Third, the economics might need to change as AI is structurally deflationary. A business model based on low prices - which can now be competed with, and high volume - which will structurally reduce… Well, you can do the math. Again, not all SaaS are impacted but most, while the market has no clue on which.

The SaaS sector, or what it will become, needs to prove itself. It needs to prove the market its business can adapt to AI, leverage the technology to its benefit and accelerate user acquisition or monetization. If we take Adobe as an example, again… We’re not there. Some are doing well, no doubts there, but again: the market treats them all the same because it has no certainty what AI will be in five years and considering the recent pace of improvements, it assumes it will continue and could disrupt more verticals - and might be right.

The market cares about predictable and safe future cash generation and stocks trade on liquidity first, sentiment second and fundamentals third.

Liquidity is tight, sentiment is in the gutter as SaaS future is everything but predictable and their fundamentals - hence cash generation, is threatened. In the meantime, many sectors have large tailwinds and are worth betting on while the SaaS downtrend has no end in sight. It will end when most companies show that their AI centric service has a large potential, not before, and this might come in years for our legacy players, or in a few quarters for new ones. Cheap is a bullshit word in the face of a technological revolution, and being early is not a great position to be when investing, contrary to what most preach on social media - and their portfolio shows this today.

I will without any doubt be one of the biggest SaaS stock buyers in the years to come, and I’ll very probably make a killing on those names once the market sees the potential and corrects its mistakes. It will happen, but today is way too early to anticipate tomorrow’s winners - even if some look very tempting like the cybersecurity vertical. You don’t want to hear this, but most will become value traps. Let time filter those and let the market give signs of who will win the AI enhanced software era.

What was won’t necessarily be again.

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

Enjoyed reading this !

Well said, well said..