Nvidia Detailed Q3-25 Review

No accounting fraud. No AI bubble.

Everything you need to understand Nvidia’s investment thesis is here.

Most of the world’s industries haven’t really engaged Agentic AI yet, and they’re about to. All of those different industries are now getting engaged, and they’re going to do their own fundraising. Do not just look at the Hyperscalers as a way to build out for the future. You got to look at the world. You got to look at all the different industries. Enterprise computing is going to fund their own industry.

We’ll go over the - very bullish, data first and I will conclude by a long write up I did yesterday on why most bears are wrong. There are real concerns around the sector but no weakness in the data itself.

Business.

Another very strong quarter, as usual for Nvidia despite the market’s reaction. Anyone looking at this chart should reach that conclusion. Yet, many bears remain with new original cases every quarter.

The data, however, is overwhelmingly positive, with plenty to look forward to. Their new GPU line, Rubin, is set for H2-26 while Blackwell continues to ramp up & is the main driver of this quarter’s revenue acceleration.

Demand is strong and not slowing.

The clouds are sold out, and our GPU-installed base, both new and previous generations, including Blackwell, Hopper, and Ampere, is fully utilized.

As for how long this will last, there were no indicators in the call. Nebius’ CEO said on its quaterly call that supply constraints shouldn’t be resolved before at least end of 2026, in their view. Jensen doesn’t give timeframes, but emphasized that demand is growing, with more to come as innovation continues.

Now, a new wave is rising: Agentic AI systems capable of reasoning, planning, and using tools. From coding assistants like Cursor and Claude Code to radiology tools like iDoc, legal assistants like Harvey, and AI chauffeurs like Tesla FSD and Waymo, these systems mark the next frontier of computing. The fastest-growing companies in the world today - OpenAI, Anthropic, xAI, Google, Cursor, Lovable, Replit, Cognition AI, OpenEvidence, Abridge, Tesla, are pioneering Agentic AI.

And many data sets proved that AI improves productivity and business metrics.

Salesforce’s Engineering team has seen at least a 30% productivity increase in new code development after adopting Cursor.

Meta’s Gem, a foundation model for Ad recommendations trained on large-scale GPU clusters, exemplifies this shift. In Q2, Meta reported over a 5% increase in Ad conversions on Instagram and 3% gain on Facebook feed, driven by Generative AI-based Gem

The AI revolution is real. It shows in the numbers. And Nvidia’s demand should remain not only because the world needs more compute but also because we are limited in energy sources and needs more efficient compute.

Each new GPU generation delivers more compute per unit of energy, meaning data centers can increase output without raising consumption.

It is the best Performance per watt, and therefore, for any amount of energy that is delivered, our architecture will drive the most revenues.

Economically, the choice is simple: more/new GPUs instead of data centers.

This is a huge part of Nvidia’s bull case and why companies adopt new generations.

We currently have visibility to $500 billion in Blackwell and Rubin revenue from the start of this year through the end of Calendar Year 2026.

But this is of course combined to a massive demand for more compute, so large that even their pre-2020 GPU generations are in usage, optimized by CUDA.

Thanks to CUDA, the A100 GPUs we shipped six years ago are still running at full utilization today, powered by vastly improved software stack.

This is Nvidia’s proposition: efficient compute. That’s why the world turns to them, not competition, because they can propose the most energy efficient compute with the longest life cycle thanks to software optimization.

Anthropic’s compute commitment is initially including up to 1 GW of compute capacity with Grace Blackwell and Vera Rubin systems.

I talked about this deal a bit more here.

Those deals, which many consider to be a circular economy with the same dollars being spent left and right, have two objectives for Nvidia:

Expanding the CUDA ecosystem and reinforcing its network effect. By investing and partnering, they drive CUDA adoption and new feature development.

Accelerating the AI revolution while profiting through equity ownership in exchange for services.

We are expanding the reach of our ecosystem, and we’re getting a share and investment in what will be a very successful company, oftentimes once-in-a-generation company. That’s our investment thesis.

Jensen also threw a subtle jab at AMD without naming them.

We invest in OpenAI for a deep partnership in co-development to expand our ecosystem and to support their growth. Of course, rather than giving up a share of our company, we get a share of their company.

The message is clear… If you’re dominant, you take, you don’t give.

Some words on their networking solutions which are also expanding rapidly, which could concern Arista Networks shareholders by now, as highlighted a few weeks ago.

[…] networking more than doubled given the onset of NVLink scale-up and robust Double-digit growth across Spectrum-X Ethernet and Quantum-X InfiniBand.

Our networking business, purpose-built for AI and the largest in the world, generated revenue of $8.2B, up 162% YoY, with NVLink, InfiniBand, and Spectrum-X Ethernet all contributing to growth. We are winning in Data Center Networking as the majority of AI deployments now include our switches with Ethernet GPU attach rates roughly on par with InfiniBand.

It isn’t the end of the world as there are many situations where Arista will remains the better hardware, but losing or slowing market shares growth in high-end GPUs environment could be worrying.

Lastly, we need to keep in mind that this quarter was achieved without new orders from China.

H20 sales were approximately $50 million. Sizable purchase orders never materialized in the quarter due to geopolitical issues and the increasingly competitive market in China.

Which reflects a massive and unexpected demand from the west.

And we had news Friday that Trump’s administration is considering authorizing H200 sales. Nothing official but it would be massive for Nvidia and the market if approved, as it meand allowing better hardware shipments to China despite Trump’s public stance against it.

I said weeks ago that China wouldn’t cave on GPUs and would leverage its position to regain access to Nvidia hardware. This could be it, and the market would welcome the news as after the proof of such demand from the west, having access to an equivalent market on the other side of the world for a more powerful generation of GPUS would unlock massive growth.

The Bear Thesis.

Even after such a quarter, bears remain. I made some comments on the most shared bear case posted after the quarter in an article called “The Algorithm That Detected a $610 Billion Fraud: How Machine Intelligence Exposed the AI Industry’s Circular Financing Scheme.”

There you’ll find in the note below explanations of why Nvidia isn’t inventory stuffing, why receivables aren’t an issue and why delays aren’t material. Adding context to the data is what makes a good investor and is something algorythms cannot do.

Financials.

We are talking about 22% sequential growth for the largest company in the world, for more than $50B in revenues. I’m not sure we fully realize how extraordinary numbers are. Gross and net margins were steady around 73% and 54% respectively, and cash generation was as strong as ever.

Once again, if you’ve heard about channel stuffing, inventory issues, or payment delays, the note above goes into detail on why adding context to data is key to understanding the situation.

In terms of cash, Nvidia holds $50B in net cash, repurchased $5.7B worth of shares, and generated $22.11B in free cash flow.

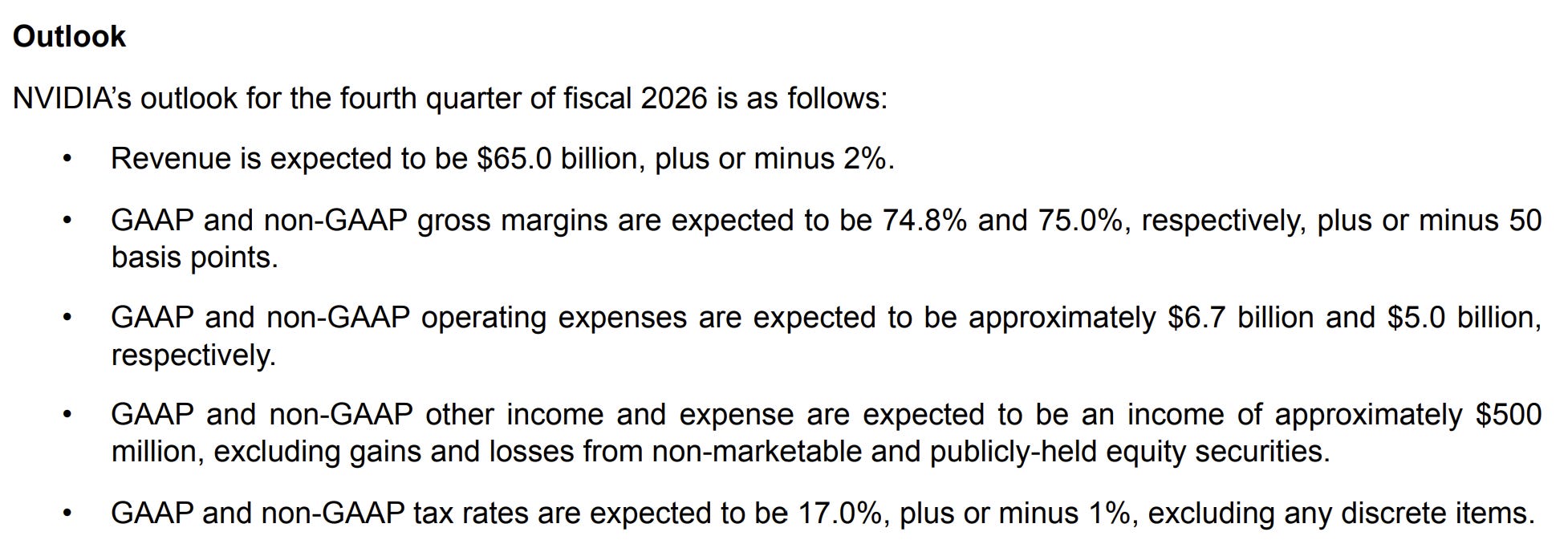

Guidance.

More of the same: a 14% sequential increase for the next quarter. Without China.

And we had some comments on the future.

We are working into our $500B forecast, and we are on track for that as we have finished some of the quarters. We have several quarters now in front of us to take us through the end of Calendar Year 2026. The number will grow, and we will achieve, I’m sure, additional needs for compute that will be shippable by fiscal year 2026. There is definitely an opportunity for us to have more on top of the $500B that we announced.

The forecast for FY25 and FY26 combined implies roughly 50% YoY growth FY26, once again, without China.

Investment Execution.

I can’t understand how one can be bearish after this, or after this earning season with most tech companies reporting really strong demand and results, mostly in line with expectations, or above, and pointing to more.

This is a bubble sustained by growing revenues, expanding margins, rising demand for a product reshaping industries worldwide. I want more bubbles like this, and I’d like it to go even further.

That said, there are valid concerns around commitments - particularly from OpenAI, and the fact that organic financing seems to be fading, with even financially strong companies turning to debt and convertible notes to fund expansion - namely Google Meta and Amazon lately.

So, two outcomes are possible:

AI continues to generate enough revenue growth and margin expansion to justify those commitments, maybe even more, and pay for them.

AI fails to generate returns quickly enough & some players will face consequences.

For now, evidence points to the first but market is anticipating the second happening sooner rather than later. Will it be right? Impossible to say; it’s our role as investors to take a directional bet based on our opinion, or to ignore the sector entirely. Market’s large enough to avoid tech altogether.

I’ve picked mine and I remain involved in tech for a portion of my portfolio and will grow this portion in the next months if prices remain attractive and I see no data to disprove my thesis that there is demand for AI and that it is improving business & generating cash.

I won’t change my valuation model, as I was already expecting this kind of growth for Nvidia.

This model assumes a 45% & 30% CAGR growth until FY26 & FY29 respectively, 50% net margins, 1% return to shareholders and a P/S & P/E at x12.5 & x45 respectively.

It’s worth noting: if the U.S. modifies curbs on China and allows sales of newer GPU generations, my valuation model would be bearish given the size of the Chinese market.

The market has been pessimistic lately. It no longer believes in rate cuts and is worried about tech in general, with some calling Nvidia a fraud while more measured voices raise red or orange flags about demand and payment capacity.

The stock has been quiet, retesting its weekly 21 perfectly around what I consider to be fair value assuming no China sales.

I’ll conclude as I did last quarter.

I probably won’t be a buyer of this retest as seeing Nvidia around $160 without signs of lower compute demand would bring stocks like Nebius or Astera to interesting buying targets, and I’d prefer those higher risks/reward stocks in today’s market.

But Nvidia remains one of the best stocks on the market & most important company of the world, and any long term investor holding shares should hold onto them to my opinion. I see no reasons to close that position and many reasons to grow it.

Appreciate the humility to look at the bear case and study it.