Various Earning Reviews

Bears are either dead or dying

So… I did not want to spam you with two or three articles this week and thought a condensed one would be a better idea. I might have been wrong, as you are now in the presence of a massive write-up…

Tons of information, but only valuable information - and mostly bullish.

The Hardware Saga

As usual, I will treat hardware names as one as they are all part of the same narrative, one of continuous demand for optimized architectures to improve GPU computing capabilities.

To spoil it, this week confirmed what we knew from the first and second earnings’ week. Demand is not slowing. No point in doubting anymore.

AI Core Infrastructure

Let’s start with core AI hardware first, with a quote from Arista’s management, to put you at ease on the current state of hardware demand.

The supply, however, is a slightly different and opposite tale. We are experiencing industry-wide shortages across the board, be it wafers, silicon chips, CPUs, optics, and of course, memory that I referred to last quarter, coupled with elevated costs to procure these. I think the supply chain problem is not a one or two quarter phenomena. We now think it’s a one or two year phenomena.

This quote is already extremely bullish, and SMCI confirmed this shortage in their own earning call. When all key actors tell the same thing, we should listen. Their knowledge is thousands of times better than ours…

Now, earnings were great but the stock still tanked, for two reasons.

As components are in shortage, price increases could hurt margins. The market doesn’t accept lower margins lately, for any company, not even AI hardware stocks apparently.

They shared they’d continue to focus on XPO for scale-up while the market is focused on photonics and CPOs - not the perfect narrative.

Within a rack and scale-up, there’s still a number of choices. I think within short distances of 2 m- 3 m, you’re still gonna see a lot of co-packaged copper. I think XPO in terms of density will be another alternative. I don’t rule out open CPO as well over there if they’re really looking to maximize their density in a minimum amount of space. I think XPO will be particularly prevalent in scale-out and scale-across, and will be one of the choices in scale-up.

Arista is one of the key giants in the industry so again, we should listen. If they say XPOs are in high demand and will be the most demanded hardware until 2027, before CPOs, they know better. Also worth noting that Astera Lab’s management said the same thing and confirmed growing demand for XPO. If necessary, XPOs are copper-to-optic pluggable while CPOs are optic-to-optic ones.

But earnings were excellent; management increased growth guidance and confirmed that scale-out/across was healthy and growing, while they’d work on scale-up from 2027 with copper solutions first, optic later. This isn’t bearish on photonics, but we have to keep in mind that the technology will take time to be finalized and scale, and shouldn’t rule out copper until then.

Arista is down 19% since earnings and buyers aren’t really stepping in. There is a case to buy the W50 ~$130 for a trade. The chart is wonderful but we are trading at a high valuation with declining volume and margins concerns - which seem a bit overblown but the market is always right, so…

This cannot become a core position, but a trade is possible with a tight stop-loss.

On CPUs, AMD and ARM confirmed that more of them will be needed to orchestrate GPUs compute for inference.

I personally was a bit bearish on AMD as the narrative was that their GPUs would overtake Nvidia as a cheaper alternative. Always called this bullshit, but I missed the bigger picture: CPUs. AMD had everything to be a massive player within this narrative, and I missed that.

The take-away from this quarter is simple and comparable to what I’ve been writing almost every day for months now: AI infrastructure is focused on customization as GPUs need support to be used at 100% of their capacities.

Data center is now the primary driver of our revenue and earnings growth, and as AI adoption scales, demand is increasing not only for accelerators, but also for the high-performance CPUs that power and orchestrate those workloads.

Inferencing and agentic AI are increasing the need for server CPU compute, as these workloads require additional CPU processing for orchestration, data movement, and parallel execution, in addition to serving as the head nodes for GPUs and accelerators. As a result, we are seeing both stronger near-term demand and deeper engagement with customers on long-term capacity planning.

At our Financial Analyst Day in November, we outlined the server CPU market growing at approximately 18% annually over the next three to five years. Based on the demand signals we are seeing today and the structural increase in CPU compute requirements driven by agentic AI, we now expect the server CPU TAM to grow at greater than 35% annually, reaching over $120 billion by 2030.

While we are still in the early stages of the AI infrastructure cycle, the pace and scale of deployments we are seeing today reinforce both the magnitude and durability of the opportunity ahead. As inferencing and agentic AI deployments scale, they are fundamentally increasing compute requirements, driving both larger scale accelerator deployments and significantly more CPU compute.

You know, it’s very hard to call exactly, but we certainly see the movement where in the past the CPU to GPU ratio was just as a host node, you know, in like a 1- to- 4 or 1- to- 8 configuration, now changing and getting closer to a 1-to-1 configuration; you can even imagine if you get lots and lots of agents that you could have more CPUs than GPUs.

AMD expects its CPU branch to grow 70% YoY. This quarter was also bullish on Silicom as AMD confirmed a growing demand for FPGAs for inference architectures.

Design win momentum grew by a double-digit percentage year-over-year with billions of dollars in new wins across markets, reflecting the continued expansion of our embedded business from a primarily FPGA-focused portfolio. Our semi-custom engagements also expanded in the quarter as data center, communications and other embedded customers leverage our broad IP portfolio and high-performance expertise to build differentiated solutions.

This confirms my bull case, although Silicom already received an inference PoC order so the bull case was already confirmed, but more confirmations never hurt. And we had one more with ARM as management confirmed that SmartNICs - not just FPGAs, were also accelerating in demand for AI inference purposes.

It’s hard not to be overly bullish on this inference PoC and Silicom.

ARM estimate CPU demand will quadruple by 2030, confirmed their architectures will be part of all hyperscalers’ next designs and that demand for their AGI CPU doubled in a few months to ~$2B run rate for the next year.

Market’s problem was the same as for Arista; management confirmed they secured the components for ~$1B of orders only and that the rest would come at a more expensive price point - if they were to find supply, while the transformation from 100% licensing to manufacturing will reduce margins long term. Extremely bullish on the market’s dynamics, but if you do not have the components to meet demand and reduce margins by doing so…

I chose to close my trade with a nice ~20% gains post earnings as ARM is valued for perfection and the promises of a quadruple demand volume for the next three years is great, but execution remains a question mark at this valuation.

Lastly, Lattice also reported great numbers. I look at it as a proxy for Silicom as they are a pure FPGA play, key component of Silicom’s SmartNICs. The quarter beat expectations with record revenues, growth and margins, and highlighted the bull cases for FPGAs with different partnerships; inference but also the future bull case: robotics.

The story is centered around AI data center and compute because of the current bottlenecks FPGAs and SmartNICs can – and will, help with, but robotics will be built around FPGAs. It won’t be here to help, it will be designed around them.

Coming back to partnerships, Lattice announced one with Nvidia’s robotics programs and TXN for the same reason. If those constructors need FPGAs, even if not sold within NICs by Silicom, it means that demand is real and others will need complete and personalized hardware including FPGAs.

Photonics

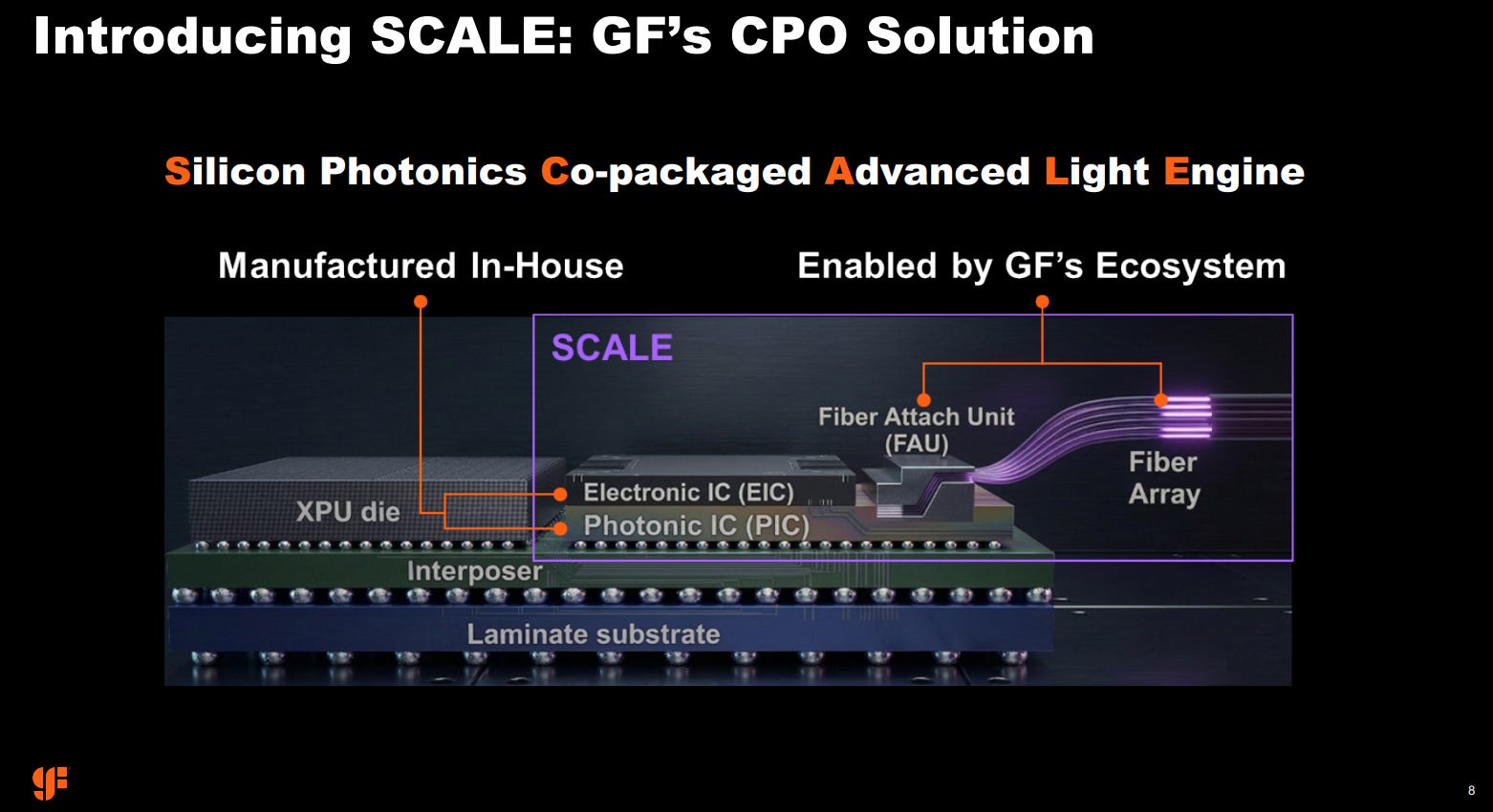

Global Foundries, one of my core holdings. The quarter showed what I wanted: healthy enough core business with an explosive vertical, its AI data center business growing 32% YoY and expected to grow ~100% FY26 - including its SiGe business which is oversubscribed until 2027. The market continues to treat it as a slower giant because of its other verticals, which aren’t that sexy.

I believe those verticals are what makes Global Foundries a great pick. Management is optimistic on their trajectory for 2026, except for their smartphone vertical - although they highlighted a growing demand from AI wearables which could balance lower smartphone demand and is a great indicator for my Nordic Semi thesis. Second, those verticals are the source of cash generation allowing expansions without dilution, an advantage compared to Tower semi.

The company is winning designs, 50% more wins than last year at the same period, is oversubscribed on photonics/SiGe demand for data centers, forced to increase CapEx to meet a growing demand for higher-margin products… This is a great position to be in, having the cash to expand while expecting a ~100% growth from an accelerating vertical on which management announced its new CPO technology, not only meeting clients’ expectations, but exceeding them.

We shouldn’t expect explosive returns, but slow and steady gains as core business bounces while higher-margin photonics grow in volume. Guidance came at $1.76B Q2-26 and management recommitted on its $1B run rate from photonics by FY28, up from ~$200M last year and planned to double this year.

Last interesting note, management had a $500M buyback plan and bought back for $400M worth of shares, almost consuming entirely their program. This shows what management thought about valuation – just like I did.

On optics, the signs are crystal clear: supply is just not keeping up with demand.

Coherent reported accelerating growth and margin expansion, hence pricing power.

On track to double internal InP output by year-end and more than double again by 2027.

Applied Optoelectronics reported the same. Revenues grew 12.5% sequentially with a 154% growth for their datacenter products, guidance is planning a 19.2% sequential growth for Q2 and management confirmed this trend should accelerate.

Looking ahead, we continue to anticipate a strong volume ramp of our 800G products starting in Q2 and we anticipate sequential revenue growth throughout this year, with significantly larger growth expected starting in Q3 as additional capacity comes online.

And Lumentum said they were short of supply of everything and are fully booked for what they have.

Those three report confirmed two things.

The increasing demand for optic hardware to scale scale-out and scale-across.

The increasing demand for optic hardware for scale-up through photonics.

A crystal clear supply shock for most of the required components, from InP substrates (Axt and IQE are two great names to buy in this vertical if given the opportunity) to lasers, and more.

AAOI’s management expects this supply shock to continue until at least mid-2027 and plan to ship ~900,000 monthly 800G/1.6T optic transceivers then, from ~100,000 today with most of the new production within U.S. fabs - a great bonus for hyperscalers who do not want to rely on geopolitics and complex supply chains.

This is the size of the demand and the infrastructure expansions happening to meet it.

Few bonus, AAOI management also talked about reaching profitability early this year which means not only accelerating growth but also improving cash generation. This is the double re-rating situation we’ve been talking about and the golden standard for investing. This is what we want to own, even if in AAOI’s case it will take a few more quarters to materialize.

For the broader market, this indirectly confirms the growing demand for Soitec’s wafers and Global Foundries’ capacities to manufactured finished CPOs.

As for market reactions, most names ended up green after some volatility; keep in mind that most of them ran 1,000%+ and need to breathe a bit, while being priced for nothing less than perfection - and more. The narrative just strengthened after this week and I’ll buy any dips on the key names of those verticals - if given.

I also had a look at Fabrinet (hardware packaging company) and On (semiconductor fab), both reported excellent earnings. The first one is expanding its capacities to meet increasing demand - optics are the star of the show while CPOs haven’t started to scale. The second yielded 30% sequential growth on its AI vertical and is expecting to double revenues this year, following TXN’s example as AI infrastructures expand. Also interesting to note a growing demand for storage related hardware, which plays into my SolarEdge thesis and its B2B new business - more on this a bit later.

Compute Providers

Few words on CoreWeave and Iren who follow the path of hyperscalers with the same trend of demand outstripping supply, especially for CoreWeave and its Google-like RPO growth, reaching ~$100B with an average contract length ~5 years.

Gone are the days - or should be, where the market doubted compute demand or clients’ capacity to pay; this backlog isn’t just OpenAI, it includes Meta, Microsoft, Jane Street, Mistral, Perplexity, Anthropic… Some concerns still exist but the market should open its eyes on compute demand and financial commitments, especially as token price is getting cheaper and usage is accelerating as clients find new economically viable sources of consumption. Consumption isn’t slowing, on the contrary.

The market continues with the same narrative though, “neoclouds don’t make cash”. Margins decrease and explosive RPOs mean more spending, not less, which comes with more depreciation, lower margins, etc…

This is why Meta was punished, why I believed Nebius would also be, what CoreWeave is struggling with today and why I prefer to invest in hardware despite the potential in compute providers and my bullishness on token consumption, and AI at large.

Cash generation is what matters the most for a stock.

Iren is Iren, not my personal favorite as I consider it a great energy/infrastructure player but not a neocloud, like most of the Bitcoin miners reconverting in compute - I might be wrong here but I’ll be fine with this. Still, they received a partnership with Nvidia which helped the stock, while missing on market expectations for both revenues and earnings.

The partnership is classic, Iren will be a privileged partner to Nvidia who will rent part of their compute once installed, plus have the right to buy up to 30M of shares at $70 in the next five years. This is a net positive for Nvidia who get orders for its hardware, compute it needs and in exchange, gets the right to own a portion of the company who took all the risk. Iren will have a guaranteed client for its compute which derisks the investment for the next years, but will still need to fund the hardware as Nvidia isn’t helping here.

Sure the market likes it, and it’s not a bad deal. It’s just clear who wins the deal and who needs it badly. There are better fundamentals out there - Nebius notably.

The Software Saga

In this bloodbath, one irresistible Gaul resists, and his name isn’t Obelix, but Palantir. We have rarely seen such companies on the market outside of AI hardware – even within there aren’t many with such execution.

So I’ll be brief, another quarter, another masterclass.

More acceleration, more cash generation, more deals, more demand, just… more. That’s all there is to say and that shows how important AI enhanced services will be in the future. Can’t forget that as a day will come where performance will be in those assets, not hardware anymore.

But. Because there is a but. The market isn’t reacting, the stock is down 7% since the print and I see excellent reasons for that.

The stock front ran earnings. This always happens in growth, and this is why investing based on multiples never works. As the market anticipates, multiples rocket and then stabilize, giving time to the stock to catch up. This is where we are with Palantir. This stock will go higher, but the probability of nothing happening or it going lower first is much higher than others.

The market has new shiny toys. Excitement is not in AI models or Palantir anymore, it shifted to new hardware technologies with photonics, CPUs, memory, etc… As I’ve said a few times now, liquidity is thinner and concentrating, leaving the old toys to go towards the new shining ones. Liquidity makes stocks move.

What I know is that a stock not running after a beat and raise revenues means there is no demand for it. However amazing the company is, I’d rather be in other stocks.

To comment rapidly on Duolingo, well… AI services aer still a niche with only a few massive winners. Management said monetization would slow down in exchange for user growth and a focus on retention and acquisition. Can’t say it isn’t working.

But as usual, the market cares about cash generation. It’s great to grow users but if it is just to add more users who do not pay, well… what’s the point? So until cash is generated, the stock won’t see any progress.

Shopify is in a different boat but with the same kind of reactions as the stock sold off 15% after strong earnings. What matters is the future and not the past and guidance is looking a bit slower. Any SaaS with slower growth isn’t worth a premium, this is the market’s current rules.

In a market where Palantir is down 7% after such a quarter, I wouldn’t look at any SaaS as potential plays… Just accept it. Their time will come. The only winners this week were Fortinet and Akamai, two cybersecurity oriented services. Not surprising at all to see cybersecurity being the first sector pushed higher by AI, and I will keep a close eye - and maybe propose some trades, on Palo Alto and Crowdstrike earnings, as those could follow.

Defensives

Starting with SolarEdge which delivered healthy earnings considering Enphase’s results a few days ago - which confirms my choice of picking SolarEdge. Revenues and guidance were in line with expectations with strong demand from Europe, as expected now that interest rates are lower and the Iran situation is pushing energy prices with no end to this in sight. Europeans who are stuck between Russia - fom whom they refuse to buy oil, and the U.S. who overcharges for LNG. Energy prices won’t go down and many Europeans know that.

In the U.S., residential remains slow but the narrative is on commercial and AI datacenters whose energy consumption is through the roof and constantly growing, looking for cheaper and grid-compatible alternatives while their new platforms are meeting interest.

I didn’t see anything wrong with this quarter, nothing which would go against my thesis and the market sold the stock for no specific reason but maybe the EPS miss which was due to a one time bad debt write off, while overall the company’s margins are getting much healthier.

I personally sold more puts on the W50 at $36 and bought a ~70% position in shares, I’d buy more on the W50.

Now I want to talk about Fluence Energy on which I bought a position today pre-market. I invested in SolarEdge partly for their future AI datacenter batteries they are developing as we know the grid cannot support many more data centers and those want - or will be forced, to use alternatives not to impact global electricity prices. Batteries have a great potential to help.

But they need to be adapted to the grid and datacenters, to be the bridge between two different electrical structures which is technically complex, which is why I am bullish on SolarEdge developing their new hardware.

Thing is, Fluence Energy announced yesterday having signed MSAs with two hyperscalers for their batteries and said they were the winner of a 25+ provider study.

The selection process for both of these MSAs was subject to multiple rounds of review. In each case, Fluence was chosen after meeting criteria specific for each customer. In one case, the customer's process began with 26 different best vendors. Fluence was the first to complete all qualifications to sign a global MSA. In the other case, the customer had requirements which made it hard for many competitors to comply with. In both cases, we believe Fluence's understanding of customer requirements, rapid response time, and differentiated products were key in driving this engagement. These MSAs established Fluence as a qualified supplier, positioning us to bid on expected near-term data center projects for both hyperscalers.

MSAs are technical reviews and purchase agreements for their solution, without financial commitments. Meaning their batteries will be bought but we do not know for how much and this commitment isn’t represented in the company’s financials.

Talking about the financials, Fluence increased its backlog by 40% over the last six months to $5.6B, without including those two hyperscalers - while one is expected to sign the financial contract and disclose its purchase by Q3-26. In brief, demand is accelerating without including on hyperscalers.

The company is valued at $3.5B at the time of writing, at 1.3x sales. I bought a position even after a 60% jump in two days. It is scary to buy after such pump; there is a part of speculation since MSAs still have to translate into financial orders, but I have shared many times that I am bullish on batteries for datacenters and this kind of event is exactly my bull case. If my thesis is materializing while the stock is still cheap, I want to be a part of it as it also is plausible that SolarEdge’s batteries were tested and didn’t meet requirements.

It is risky, but the potential is here.

Nutrien also reported earnings on Wednesday and numbers are good. The take-away is simple: demand for fertilizers is growing while supply is tightening and prices are rising. Not great for inflation outlook, but great for defensive names.

We increased production from our low-cost North American assets and positioned our supply chain to reliably supply our customers amid tightening global fertilizer supply and demand fundamentals.

Global potash demand remains strong and we have maintained our previous forecast range for global potash shipments of 74 to 77 million tonnes in 2026. We anticipate relatively tight potash fundamentals throughout 2026 with demand trends expected to test existing global operating and supply chain capabilities.

This is bullish for my Intrepid Potash position at least in terms of market trends, as the company remains more speculative than giants like Nutrien and will require good execution to yield returns. But this at least confirms the global thesis.

The Space Narrative

RocketLab delivered a record quarter filled with confirmations of the growing and accelerating demand for space launch, systems and services, which is my thesis. We are talking about record launches backlog and the largest ever Neutron contract, which is a great confirmation as it is a direct competitor to SpaceX.

I closed my trade opened and shared on the Substack chat today at $98, returning 25% in three weeks.

Firefly also released a correct quarter with good demand, revenues and backlog but the market did not like comments about no NASA contract coming for the next three to six months… Except RocketLab, most of the sector relies mostly on public contracts so no new ones means no increased expectations and no re-ratings.

The bottom line remains positive for the sector as the interest continues to grow and I continue to be bullish, but still less than the AI hardware sector, meaning my liquidity will continue to go there more than anywhere else.

Transmedics’ Fiasco

I shared on my monthly review that I opened a trade on Transmedics; My thesis was that the margin narrative due to fuel prices was overblown and that I expected revenues to beat expectations. I was wrong.

Revenues fell in line with expectations but operating margins fell to 7%.

On a narrative that fuel prices would crush margins and cash generation, any misstep hurts badly, whatever the reasons. In this case, margins decreased as investments continue - on their clinical trials and expansion. Normal and healthy business is being punished. I talked about this potential scenario during my last quarterly review, and it materialized.

There are no valid reasons in my opinion and we’ve seen that the market bought the stock today, passing from -7.5% to -0.9% at time of writing. There’s demand at today’s price and that’s what I’ll conclude later. But it’s important to remind ourselves that our opinion just doesn’t matter.

And we have to remain factual and keep our feet on the ground. The market, even if it sees the positives, focuses on the negatives. And there are two.

The margin pressure is real and will persist through 2026 as detailed above.

The company has execution risks: the trial results are still pending, even if the first feedbacks are positive, OCS Kidney is in development, European expansion will require expenses before yielding results - even if it takes only one semester.

TransMedics has execution risks which comes with shrinking margins in the meantime. The market is not punishing the stock, it is simply acknowledging the risks, the “what if it doesn’t work?”.

I called that trade an everything or nothing trade. It’ll be nothing. I sized it to be minimal and not hurt me, so it won’t. I played and I lost, moving on!

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

Amazing write up, thank you 👍