The Ignored Part of the Market

Excellent trades which have been left behind while social media chase the AI frenzy

Most of you will probably close this post in a few seconds. These assets aren’t what you expect from me, or from any investment subscription.

We aren’t talking about “the future” or potential 1,000% returns stocks. We are talking about old, boring companies. But sometimes, boring is where the money is. My job is to find profits, not thrills. I’ll leave the thrills to others, I don’t care about those.

A few months ago, I shared several ignored setups on X and here. No one cared then, but the results spoke for themselves: Dollar General (+72%), Dollar Tree (+74%), Schlumberger (+29%), and Halliburton (+47%). If you used the option strategies I shared for SLB and HAL, those returns were multiples higher.

These “boring” names outperformed the market and were much safer bets. Focusing on growth is great but making money is better, it is never boring, regardless of where it comes from.

Today, we’ll look at two assets. I’ll provide a review of the fundamentals, the upside potential and a clear trade plan for investing, as usual. I’ve planned this write up to be about four assets originally, including Target, JD.com and Devon Energy. I decided to cut those & focus only on the two best setups. I’m here to share the bets that actually matter, not just a long list of “meh” trades.

I intend to buy these two. The others? I wouldn’t have. So two it is.

I’m still heavily invested in “risk” assets like crypto and tech (Nebius, Astera Labs, UiPath, Alibaba). Currently, TransMedics is my only defensive holding.

But things are changing.

I expect my portfolio to be very different in six months as the market dynamics are clearly changing. I’d expect to be out of crypto and mostly out of tech by mid-26, depending on how the market will behave obviously but that’s my base case today. I won’t cut all my positions neither, but I want to take profit from this sector & follow the rotation. These setups are the best candidates for that rotation.

I’ll buy at least one of these in the next semester. Let’s see if “boring” continues to beat tech, as it has. And remember: returns are returns.

Option Basics

Before we dive in, a quick word on how I use options, cause we’ll talk about them. I use only two types, and both are bullish.

Selling Puts: I promise to buy a stock at a specific price by a specific date. A buyer pays me for this promise.

Buying Calls: I pay for the right to buy a stock at a specific price by a specific date. I pay upfront for potential upside.

I combine both. I sell a put and use that cash to buy a call, and I focus on getting the call for free at worst - I usually try to be paid for it meaning the puts’ credit is higher than the call debit. I am buying a bull position without effectively spending a dollar.

The counter part is if the stock price is below the price agreed on the expiration date, I must buy the shares, which means you still need to have the buying power to do so, and keep it in case the situation leads to it. This can be in cash or margin, up to each of us. But if my trade is wrong by expiration, I have to buy the shares.

The beauty of this setups is that the expiration is months in how I use it, so I won’t need the buying power today unless the stock crashes. Since I focus on stocks that have already bottomed - or high probability to, and trade at a low valuation, long timeframes give me plenty of time to react.

In the best case scenario, this acts as a leveraged version of owning shares. You are positioned for a rally without spending a dollar, only with ~20% of collateral using margin. If the trade goes well:

You never spend a cent.

Your upside is unlimited because of the call.

Your margin requirement eventually goes to zero.

Your cash/margin is free to be used on other assets.

The downside? If I am “assigned” - forced to buy the shares, it means the trade went against me and I have to spend the cash to buy the stock and decide my next move. Even then, I end up owning shares of a quality business - because I only trade quality business, and I’ll need to figure out what’s my next step.

United Parcel Service

I’m sure you know the company, if only for its big brown and yellow trucks. And you are probably asking: Why on earth would I buy an old, dying delivery service?

Fair question. Social media teaches us to invest only in “the future,” hold for 20 years, & hope for the best. But UPS is a defensive asset. If you haven’t noticed, defensive assets have been firing for the last six months, they outperformed the market by a wide margin.

There’s a reason for that: Risk Appetite. Liquidity is flowing out of tech and into “safe havens”; companies that keep working regardless of what happens with AI buildouts, tariffs ruling or interest rates.

I’ll let ChatGPT tell you about it, so we still use some compute in the process.

Business:

UPS transports small packages, freight, and supply-chain solutions worldwide, serving consumers, SMBs, and large enterprises across B2C and B2B channels.Business model:

Asset-heavy, network-driven model built on owned hubs, aircraft, vehicles, and routing software. Revenue is generated per shipment, with pricing tied to weight, distance, speed, and service level. Scale, density, and network optimization drive margins, while long-term contracts and enterprise customers provide recurring volume.

The bull case isn’t much about firing up fundamentals; it’s about stability. Even if tech melts down, UPS continues to generate stable revenue. Right now, stability is on sale.

UPS is trading at a valuation much lower than its historical average, and it pays a 6% dividend while you wait. I’d rather buy “boring” stocks that make money than “sexy” stocks that lose it.

And if it isn’t sexy, remember: the ~50% of average returns of the other unsexy stocks shared above yielded enough money to buy lots of sexy things. I’d rather buy sexy things that make money on sexy stocks. But that’s me.

Investment Execution

As usual, there are hundreds of ways to play a stock. You can buy the common shares, sit back, and collect that 6% yield. That’s a great plan. If you know me, you know I’ve a more aggressive plan, an option plan made possible by the situation.

Very low valuation.

Very low risks.

Very low volatility.

Perfect price action.

UPS has been in 4Y downtrend. It hasn’t stayed above its Weekly 50 or 21 - green and red line respectively, for more than a handful weeks.

What do we see now? A local bottom. A break above the Weekly 21 and 50. Price is sticking above these lines, meaning buyers are awake. And massive volume. Nobody talks about this stock because it isn’t a growth or an AI name. But if this stock were called Palantir, the entire world would be talking about it.

The trade is simple. Since the risk is low and demand is clear, I’d be aggressive and use options. Because “nobody cares” about UPS, the premiums are attractive.

Timeframe. Taking the previous companies as example, it took them ~6 months to go from the perfect setup I shared to where they are today, up an average of ~50%. UPS is in that perfect setup now, so if the rotation continues, we can expect great returns in the next 6 to 9 months.

Target. We’d need a 50% gain to reach UPS median P/S, pushing the stock ~$150. A bit higher but let’s keep it conservative.

The Setup. UPS trades ~$108 at time of writing. The perfect entry would be on the $100 retest, or close to it, while the bottom is supposed to be set around $90. The trade already seems great at today’s price, but I’d still wait for that retest to buy in, meaning an even better setup/prices.

Expiration January 15, 2027, giving us more room.

Sell 1 Put at $85: Collect ~$430 in premium.

Buy 2 Calls at $150: Cost ~$201 per call (Total $402).

You get paid roughly $28 per contract to enter a trade with unlimited upside and a contract to buy shares at $82.2, hence a required collateral of $8,220 assuming no margins are used. With a year to go, I’d gladly use lots of margin & would reduce it during the next months if the trade doesn’t shape well.

I know this isn’t drones, robots, space data centers or flying unicorns. But while the unicorns are struggling to make new highs, these defensive setups are becoming the real unicorns of 2026 from a return perspective. Diversification won’t hurt, it might actually be the thing that saves your year if the rest goes south.

And having one unicorn in one’s bag can make a huge difference.

Novo Nordisk

You’ve heard of this one everywhere I guess. I did not like it then. I still have doubts & believe most who write about it are wrong. But it’s worth a few words, and maybe a few bucks by now.

And that is for one reason only: Novo now has a new lever for growth: The Wegovy Pill, their GLP-1 newest product, which hit the US market earlier this month.

This isn’t just a “cheap and stable” play. This is healthcare - a defensive sector, with a potential real growth lever in weight loss category - priceless product for millions. But I’ll start by setting the stage because social media is right about the opportunity. But too many ignore lots of parameters.

So, context first. Novo Nordisk took a beating in 2025 because their GLP-1 injectable is inferior to Eli Lilly’s. That’s fact. The market chased Lilly and ignored Novo’s just like patients chased Lilly’s products and ignored Novo’s. And it shows.

This was while GLP-1 were injectable. But GLP-1’s future is about pills, Novo’s already hit the market and Lilly is one or two quarters late with its own - Orforglipron. But it will hit the market during 2026, hard to know exactly when. If Novo can capture the needle-phobic now, they’ll take shares with sticky consumers before Lilly even arrives.

This is the bull case. First mover advantage, a sticky product at an aggressive price to onboard many, and therefore the potential for growth to restart. If that happens, then yes, Novo is an opportunity.

But let’s remain factual: The market only cares about Growth. Novo is not cheap at today’s multiples without it, and it would be only with 15%+ quarterly YoY growth returns. If consumers wait for Lilly’s pill, or if the results aren’t as good as expected, Novo is not a fired up sale. It is a healthy company at a correct valuation.

Technically, we’ve seen massive volume and a potential bottom. We saw a “lower low” right before the FDA approval, followed by a strong pump after. Do not rush, do not FOMO, we haven’t missed any train yet. We always have time before buying & we’d better be sure when we do.

There is volume. There is interest. But there is also a healthy dose of skepticism. While we are closing above the Weekly 21 for the first time in months, we haven’t seen a new higher high yet, nor have we confirmed a “crystal clear” double bottom.

I strongly believe we will see ~$55 again, very probably $50 during a retest. This is when decisions will matter. This was a “falling knife,” but now we are in a potential turnaround situation. The potential is here - the Wegovy pill, but the results aren’t in the books yet. The market isn’t pessimist anymore, but it isn’t overly optimistic neither, not yet at least.

This is the perfect window to start a pilot position and wait for technical confirmation.

Investment Execution

Once again: Without a 15%+ YoY quarterly growth, Novo doesn’t deserve to trade at a premium. It’ll deserve to trade north of 6x Sales from this growth rate, not before, based on its historical multiples.

If the bull case is correct - the Wegovy pill expands the market and steal shares from lilly, a 15% growth rate becomes the base case. This justifies a multiple of 6.5x to 7x Sales, which would put the stock price at roughly $75.

This has to happen in the next 6 to 9 months, before Lilly goes to market and either takes its shares back, or compete with an equivalent product. If Novo show its 15% quarterly growth then, it’ll deserve its 6x sales floor, give us our returns, and start a new narrative of which GLP-1 pill is the best.

The perfect bull case is for Wegovy to be the better, in which case Novo will become the new Lilly. But that’ll be step 2.

That gives us our timeframe (September to December), our target (at 7x sales we’re looking at ~$75), and we know our bottom (~$45).

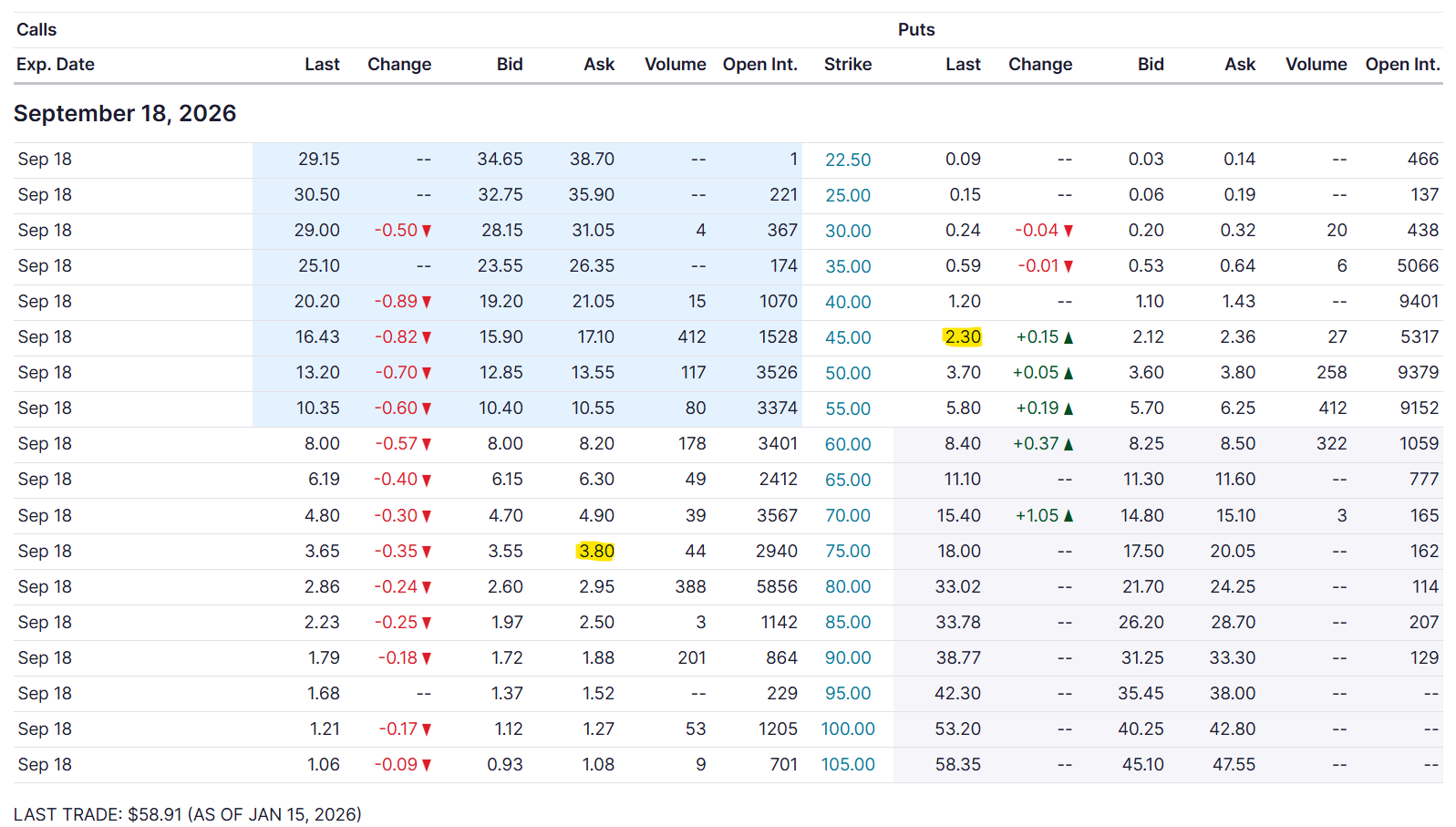

Options pricing isn’t very cooperative with the recent volatility. At current prices (~$58), the setup looks like this:

Sold put $45. Collect ~$2.30.

Buy $75 Call. Pay ~$3.80.

Roughly a $1.50 debit per contract.

It’s possible to sell two puts to buy one call for a $0.80 credit but that’d engage more collateral for one call of unlimited upside. And as usual, there are thousands of ways to play that name - buying shares being a great one as well.

Personally, I’m waiting for the stock to breath and my target to trigger my buys is ~$50. The same trade could be much more interesting by then, so I’ll be patient & adapt when the time comes.

Novo’s success now relies on execution. I’ll wait for that double bottom & $50. At that price, I believe the downside risk is limited, and the risk/reward is great now that we have a clear growth lever. If the pill succeeds, the upside is explosive. And there is a timeframe free of competition.

Once again: the risk reward seems great to me.

Conclusion

These are two solid names and solid setups to watch. We’ll check back in six months to see how the played out.

I’m personally interested b both . My ideal scenario is to see the retests hit in the next 60 days so I can take profits from my crypto trades - hopefully, and maybe from my AI trades. The risk/reward on those two is far more attractive than chasing tech at all-time highs to my opinion, especially with the option plays.

So my plan is clear: wait for the retest and the situation to shape up, then strike. I’ll without any doubts buy one of those setups. Maybe both.

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.

Question about the option strat. How far out do you sell a put and buy the call? Also, if you are assigned, do you sell calls against the holdings?

Could you explain the logic of waiting for pullbacks on stocks already breaking out? Why weren't you buying UPS and NVO at their lows with the SAME logic?