The Next Rotation Trade

An ignored, beaten-down sector at very low valuations with multiple tailwinds.

As you all know, I turned toward defensive assets a month ago, at least moving out of tech and into fairly valued assets with potential healthy upside at today’s prices.

That’s what we’ll talk about today; not necessarily about a defensive asset, but about a cyclical sector trading at very low valuations with potential tailwinds coming up in the next months that could push valuations higher on healthier fundamentals.

Materials & Chemicals

Both sectors have been doing really well over the last months, but let’s first talk about what they are. If we take a classic product manufacturing chain, it would look like this (very simplified).

Commodity → Transformation into materials → Material assembly/transformation to manufacture a product → Shipped to consumer

Most materials and chemical companies operate in steps 2 and 3, depending on what they sell. Some use molecules extracted from oil for example and transform them into chemicals; others buy those chemicals and mix them to form new products, etc...

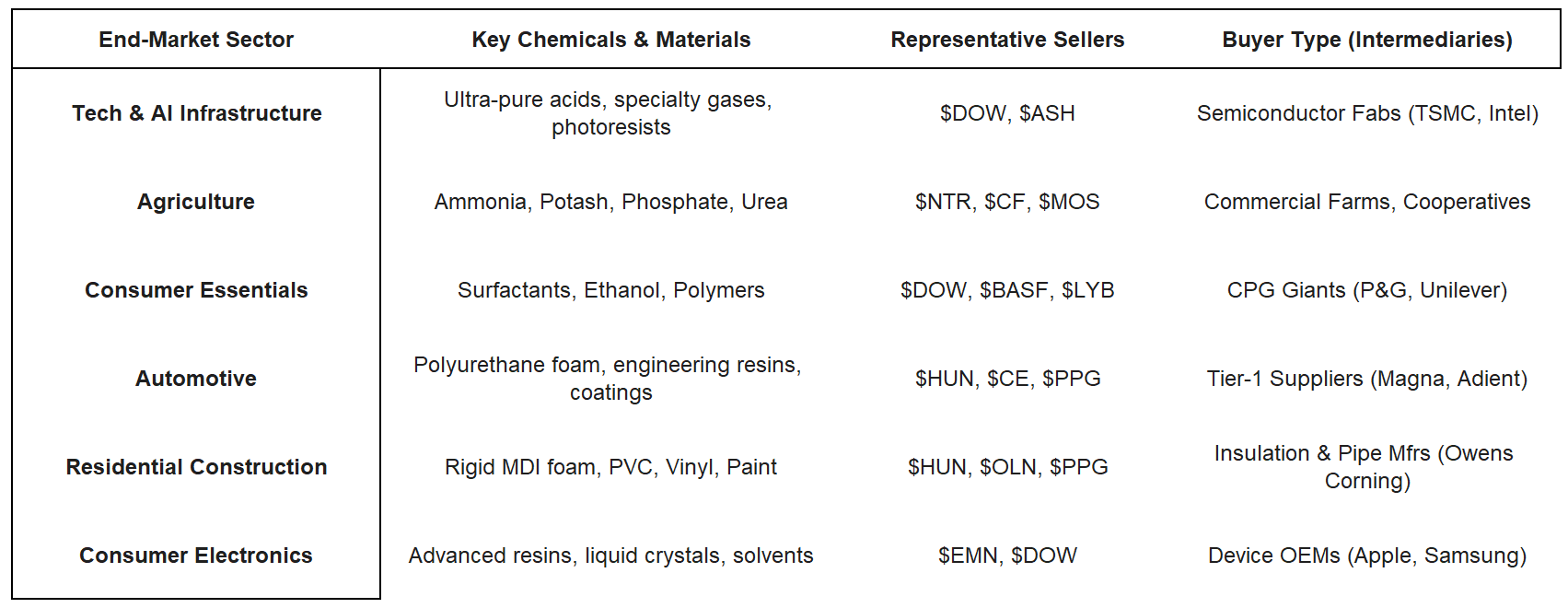

The materials sector includes a wide range of companies - from selling raw chemicals extracted from commodity to selling finished products such as construction materials. The chemical branch within the sector is also very diversified in term of products and usage. Here are a few examples to illustrate.

We’ve already talked about Nutrien for example, which has largely outperformed the market since and is part of the chemical sector for agriculture.

As you can guess, these are very cyclical businesses; companies usually focus on one or two verticals serving specific sectors, demand for their products varies depending on demand for the final products. This creates boom-and-bust cycles and if we aren’t yet confirmed in a boom cycle, we’re certainly near the end of the current bust cycle.

Which is why most of these names have been very interesting in recent months, and why they could be interesting over the coming years. They’re not tech, sure. But hey, returns in tech or in chemicals are returns.

The Bear & Bull Case

Besides inherent cyclicality in their business models, chemical companies have faced other headwinds over the last few years.

Today’s Bearish Situation

China. Probably their biggest issue as over the years, China has specialized in exporting everything the West needs, including chemicals. And over time, the country has flooded the market with cheap ones. The infographic doesn’t detail per chemical but it shows the market shares change over the last two decades.

Demand has also slowed. Higher interest rates and weaker consumer purchasing power across the West reduced demand for end products, which in turn reduced chemical demand. Coupled with high volume from China and inventories, this did not help U.S. producers.

Profitability suffered, as you could expect. Lower demand, rising competition and oversupply; the worst combination for any capital-intensive sector. Growth slowed, margins shrunk and cash generation fell off the cliff, some even turning unprofitable.

This is why most chemical companies were crushed over the past 5 years.

Tomorrow’s Potential Bull Case

But dynamics may be shifting with a handful reasons for it.

Tariffs & local production. Trump focus on the U.S. will put pressure on imports - already is, combined with potential subsidies or tax reductions when producing locally like for solar systems, this could reduce competition as they become price competitive and increase profitability.

Inventory destocking. Companies ran through inventories instead of new orders after pilling up cheap Chinese products for years. As supply chains normalize and inventories are now low, any rebound in demand will lead to restocking while the global profile of demand will globally be healthier.

As we have reported in the past few quarters, we've seen volumes improve as de-inventorying has ceased and demand has rapidly returned.

Management characterized current inventories in the supply chain as 'quite low,' flagging potential for sudden product shortages should demand rebound rapidly.

From Huntsman Feb-25 call

Interest rates. Lower rates benefit capital-intensive businesses (refinancing, new loans) and indirectly by supporting demand for financed goods like autos and housing, which are very demanding sectors in chemicals.

Restructuring. Many companies implemented layoffs, debt renegotiations and plant closures as they reached the bottom of the cycle and need to improve efficiency and cash generation for the next cycle.

Valuations. The entire sector got smashed for half a decade and many now trade at historically low multiples - for valid reasons as fundamentals also declined. If tailwinds materialize, repricing could follow.

Liquidity rotation. Capital has been shifting away from tech and growth toward cyclicals and defensives lately, we’ve talked about this at length already. And as the market cares about liquidity first, rotations are important to look at.

An entire sector with a few tailwinds after years of headwinds, dragging valuations to historical lows. There are execution and external risks to those tailwinds materializing, but valuation makes the risk-reward interesting here while the market is enthusiastic about those names.

Concrete Examples

As I shared in my March Investment Plan, I bought a position in Huntsman Corp., and shared Nutrien a few weeks earlier. I’ll focus on the first later but I will share others as all those names have one characteristic I like above all else: the market loves them.

This investment is a stock picked within a strong sector with high demand more than an investment on strong fundamentals of a single name. So it isn’t the only name worth looking at, the entire sector is.

I found ~10 chemical names on my screener the past 2/3 weeks as they all answer my conditions: clear higher low, rising volume, higher high breaking above the weekly 50. I won’t go over all the charts, just Huntsman to illustrate; know that many, many look like this (LYB DOW EMN CE ALB OLN).

This is the kind of chart I look for; they signal a clear demand for the stock.

Large volume while price action stabilizes means lots of shares exchanged without enough sellers to push the price lower. And as the price goes higher and volume continues to rise, the amount of shares exchanged continues to rise with demand at higher prices.

More investor accept to buy higher.

And there’s a reason for this.

Huntsman Corporation

Let’s look at Huntsman itself. The company is focused on downstream chemistries.

Polyurethanes (60% of Revenue): They are a top-5 global producer of MDI, the key ingredient for Rigid Foam (energy-efficient housing insulation) and Flexible Foam (mattresses, furniture and car seats).

Performance Products: They create amines and carbonates used in detergents, energy coatings, and agricultural chemicals. If a liquid needs to "stick," "foam," or "clean," Huntsman likely made the active ingredient.

Advanced Materials: Epoxy resins and adhesives used in Aerospace (gluing carbon-fiber wings for Boeing/Airbus) and Automotive light weighting.

Products for different industries but most of their revenues come from housing and auto. As I said, tightly correlated with interest rates which hopefully should go down.

Huntsman went/is going through restructuring with the objective of $100M of saved expenses, impacting margins and cash generation.

Headcount Reductions: They have cut or relocated approximately 500 to 600 positions, representing nearly 10% of their global workforce.

Asset Rationalization: They closed seven manufacturing sites, targeting high-cost loss-making plants in Europe for example.

Dividend Reset: They slashed the quarterly dividend by 65% back in 2025 to preserve cash.

Free Cash Flow Focus: Aggressively clearing out inventory late 2025 and entering 2026 with a leaner balance sheet.

Valuation was back to all-time low a few weeks earlier, with reasons. Lower growth, declining margins and cash generation with little perspectives of amelioration won’t get a premium.

So yes, we are talking about a struggling company fundamentally. But many potential tailwinds from fundamentals, from the economy and from the market.

As usual, nothing is given in the market. But this setup looks like a pretty good setup to me - not the perfect one but an actionable one, which could hurt short-term like most of the market with the geopolitical conditions, but has potential for the years to come.

Execution Plan

The market is a machine to anticipate; struggling companies can have a rising stock as the market anticipates a reversal or is optimistic about tailwinds. This is why I look so much at price action; it tells you what the market expects. Looking only at earnings & fundamentals tells you what happened, not what can happen. What is done is done, the market cares about what’s next.

Stocks trade on expectations, not past fundamental performance.

If the market’s expectations were to materialize, we’d be talking growth instead of decline and improving margins, which might not go back to pre-COVID but could reach 4%-5% operating margins and EBITDA profitability. If the actual optimism is confirmed by expanding margins during earnings, we will see a repricing. Maybe still below historical average but even then, we’d be talking about a ~40%+ upside.

I personally bought options, details on the strategy here.

The risk/reward is very healthy today and the stock is grinding higher with demand, as volume shows. I do not want to tie too much liquidity to this position, it remains an opportunistic trade based on market’s optimism more than a strong fundamental investment like TransMedics. It allows me to diversify and participates in a sector strength without committing too much.

Reversal structure, as usual:

Jan15’27 $10 sold puts, below the last weekly 50 and breakout retest, which should be a strong demand region for buyers and hold - assuming the thesis holds.

Jan15’27 $18 bought call, or ~50% gain. I wouldn’t expect it to be reached by January but I don’t think I will hold than name until then - I could. I am giving myself room to capitalize on optimism & liquidity rotation, which should both accelerate H2-26, or so I expect.

This trade would pay you $0.67 per contract, meaning you would make money as long as the stock trades above $9.33 by January, which is pretty close to yearly low and largely below all breakout/averages.

Huntsman cut its dividend as shared earlier, meaning commons are less interesting but as usual, a thesis is only a thesis, execution depends on each of us, our profile & objectives.

Huntsman is a great diversification play in a cyclical industry which is demanded by the market and with a few interesting tailwinds, while most of the headwinds have been priced in after four years of bear market.

It isn’t the only interesting asset in its sector, I chose it because I believe rate cuts and return of demand for financed goods will generate optimism for final demand plus its diversification with other chemicals for key industries in the future; but other chemical names could follow the same pattern.

It is a stock pick within a strong sector.

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.