Weekly Recap | August - W4

Weekly Buying List Update, Detailed Macro Review Plus Investing Consequences & Weekly Planning.

I joined FiscalAI affiliate program this week and will regularly share my referal link for you guys to have a 15% reduction on all subscription plans.

https://fiscal.ai/?via=wealthyreadings

FiscalAI is the tool I use on my write-ups for any KPIs & honestly the best platform on the market to follow companies. If you’re interested, feel free to use my link!

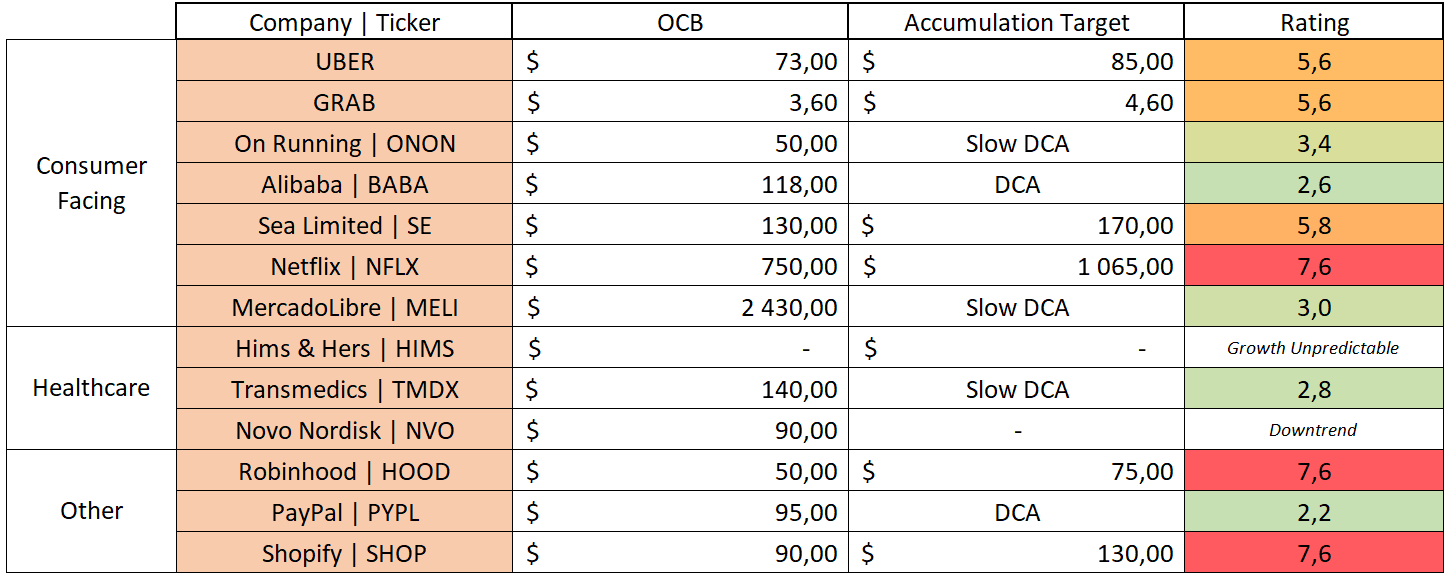

Weekly Buying List Update.

Here is my watchlist & buying plan. Reaching those prices does not mean I always pull the trigger; those are only my view of valuation & price action today. I only pull the triggers on the ones I believe to be the best liquidity attribution at the moment - purchases are shared on my Savvy B&H portfolio.

https://savvytrader.com/wealthyreadingspro/buyandhodl

Optimized Cost Basis (OCB) - optimum average price for a long term position.

Accumulation Target - buying target based on price action, to average up.

Rating - Buy < 3.5 < Hold < 7 < Trim.

“(Slow) DCA” - trading at proper conditions to open a position or accumulate.

Bold cells are updates compared to last week.

Macro.

The only important event of the week was Jerome Powell's speech at Jackson Hole on Friday, with a very positive effect on the stock market as you probably saw the SPY massive 1.54% candle.

Why is that? In a few words, because Jerome confirmed that it is time for the FED to have a less restrictive monetary policy, which means they consider cutting rates.

Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.

My take? This speech was not bullish for the economy. But confirmed that liquidity will continue to flow as the U.S. simply do not have any other alternatives. Which is usually the characteristic of emerging economies, not dominant economies.

That should be scary for Americans without assets. And bullish for any American and internationals owning American assets.

As usual, we have to use two different lenses. Market's perception, which only worries about liquidity to push prices higher, and the economy's perception, which worries about stable prices, a healthy job market with healthy paychecks.

Until Friday.

I have shared many macro reviews and two dedicated write-ups whose resumes can be that the FED has an impossible job, they have no viable solution and need to give up one of their mandate at one point, which will end up crushing the economy to some extent.

This was shared in my first macro review back in November

Economic data takes months to come, and we usually look stupid trying to predict the outcome of policies. But this was to be expected and we finally are here.

In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside - a challenging situation.

We reached the point where the FED can’t effectively balance both mandates anymore and will have to give one up to save the other.

And as Jerome talked about "adjusting our policy stance", inflation is to be sacrificed, and won't come back to the 2% goal, almost certainly not this decade.

Let's pass to where we are now, and where we are going.

Unemployement.

There are no problems in the labor market at the moment, we are stable around 4%, an average value in the U.S. although the trend is trending upward, which is the reason for the FED's concern.

We have already commented these last weeks about the rising layoffs while lower job openings, with a massive data revision earlier this month.

The labor market is slowing down in terms of demand, but also in terms of supply as Jerome explains clearly, due to much lower immigration.

Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.

In brief, we are still in an acceptable situation but the risks of a large shock is growing and the FED does not want to take chances on it happening. As for everything lately, I also want to stress that this shock is not true in all the sectors. As we saw, tech giants are healthy and continue to hire qualified engineers. The problems are with less qualified profiles and lower income households.

Inflation & Consumption.

The problem that the FED is now choosing to deprioritize as they believe it is better to have inflation than a recession. That is certainly true for the high-income households and those who already have low-rate debt or assets, as their purchasing power from salaries might decrease but as their assets increase, their global net worth is not really hurt, on the contrary.

I've talked about this back in November already, although it is true since decades now and will only accelerate.

As I have said for months on the contrary to many, inflation is not controlled in the U.S. and tariffs are only throwing oil on the fire - despite what the government says. Again, impacts take time to circulate through the real economy, but they always do.

At the same time, GDP growth has slowed notably in the first half of this year to a pace of 1.2 percent, roughly half the 2.5 percent pace in 2024. The decline in growth has largely reflected a slowdown in consumer spending.

Turning to inflation, higher tariffs have begun to push up prices in some categories of goods. Estimates based on the latest available data indicate that total PCE prices rose 2.6 percent over the 12 months ending in July. Excluding the volatile food and energy categories, core PCE prices rose 2.9 percent, above their level a year ago.

The effects of tariffs on consumer prices are now clearly visible. We expect those effects to accumulate over coming months, with high uncertainty about timing and amounts.

This cannot be clearer, and the market already knew it as it punished consumer goods while rewarding defensive assets.

Those are only four examples but the trend is larger and the market is not treating all sectors equally at all, which will make the next years really interesting.

Money Creation & Interest Rates.

Anyone comparing today’s market to any other points in time should not be listened to - either because it is clickbait or because they do not understand what they are saying. Not once in modern history have we reached this kind of situation, which makes the U.S. look like an emerging economy and it is entirely due to fiscal dominance.

To re-explain it rapidly - more detail in my November write-up, money creation has two sources.

Fiscal policies. The government contracts debt to finance itself - pay bills, employees, debt, etc. The debt can come from external investors buying U.S. treasuries or from the treasury itself, buying its own debt through money creation.

Monetary policy. Classic debt contraction through banks from the private market, accessible to any company or individual to buy… Whatever.

All kinds of debt are contracted in exchange for an interest rate which is controlled by the market, not by the FED. The FED only sets rates for interbank loans, which is why this rate is used as a ground floor for banks to loan to clients, but it raises as they include their business plan, risks and margins before loaning to clients.

The market then decides bonds’ price with a demand/supply mechanism. The FED cutting intereste rates does not mean the 10Y will automatically be lowered. If the market doesn’t want to buy bonds for any reason and would rather buy stocks or anything else, the 2Y, 10Y, 20Y, 30Y rates and co might not decrease.

This is important to understand as it will affect investments.

Conclusion.

As usual, we have to see all of this from two different lenses.

For the economy, this is bad. The U.S. reached a situation where the FED cannot do anything for both of its mandates (inflation and employment) and has to constantly favor one. As both can be fixed with diametrically opposed actions, they have to hurt one to save the other.

As they now favor employment, it means inflation will be left unchecked and as tariffs continue to ramp, prices will increase, consumption will decrease, and the low-income households will continue to suffer. Once again, economies are slow, this will take quarters, years to unfold. But it will.

Being an American without assets in America… Will be even harder.

For the market, this is neutral to good, even great depending on the sectors.

Fiscal dominance continues to be a massive tailwind for many sectors, like tech. Those companies have massive balance sheets stored in high-yield treasuries, and do not feel much pressure from inflation in their core business.

Less restrictive monetary policy means more access to debt for growth companies although a 4% or 4.5% won't make a massive difference as lending remains very expensive, but will help nonetheless, at the margins.

Both of those lead to more liquidity, and the market loves liquidity.

In terms of investing, I continue to have the same view I had in November. Every sector is a good sector as long as its business doesn't rely on U.S. consumption. I continue to be very bearish on U.S. consumer as the lower-income households' struggles will only deepen while more medium-income households will become low-income households in the years to come and slow consumption, or max out on debt which then will slow consumption.

It will take long, as said many times through this write-up, but it is inevitable.

So I'll continue to focus on tech and tech growth names and outside of the U.S. consumer-oriented companies - China & Asia mostly.

To resume:

Inflation is unchecked and will continue to ramp due to tariffs while the labor market is now weakening. Both FED mandates are in a critical state and require completely opposite measures to be fixed.

The FED intends to cut rates, probably in September, to release some pressure on the labor market and avoid a potential recession, easing the requirements for debt creation in the private sector.

Both fiscal dominance and potential easier private debt lending will continue to bring more liquidity within the market, while inflation will continue to crush Americans' have-nots and slow lower-income households' consumption.

To finish, I found this meme shared on X, and it perfectly resumes the situation.

I do not worry for the stock market which remains the best place to store liquidity and will continue to receive most of it. I continue to believe we're heading to a bubble as more and more liquidity will go there until it becomes impossible to sustain - and we are not there yet, and I continue to believe we should expect more volatility than ever globally.

But as fiscal dominance continues, nothing stops this train & the market will continue to yield returns to those who play the game properly.

As for the others… I wish them luck.

Watched Stocks and Portfolio.

August is really quiet in terms of news and I really wanted to focus on Macro and use today to do a review of the situation, so I won't share much more.

I'll just rapidly talk about Friday as many stocks flew after Powell's speech, few days after I gave my accumulation prices in this write-up.

Really hope some of you had time to read it, and buy some names.

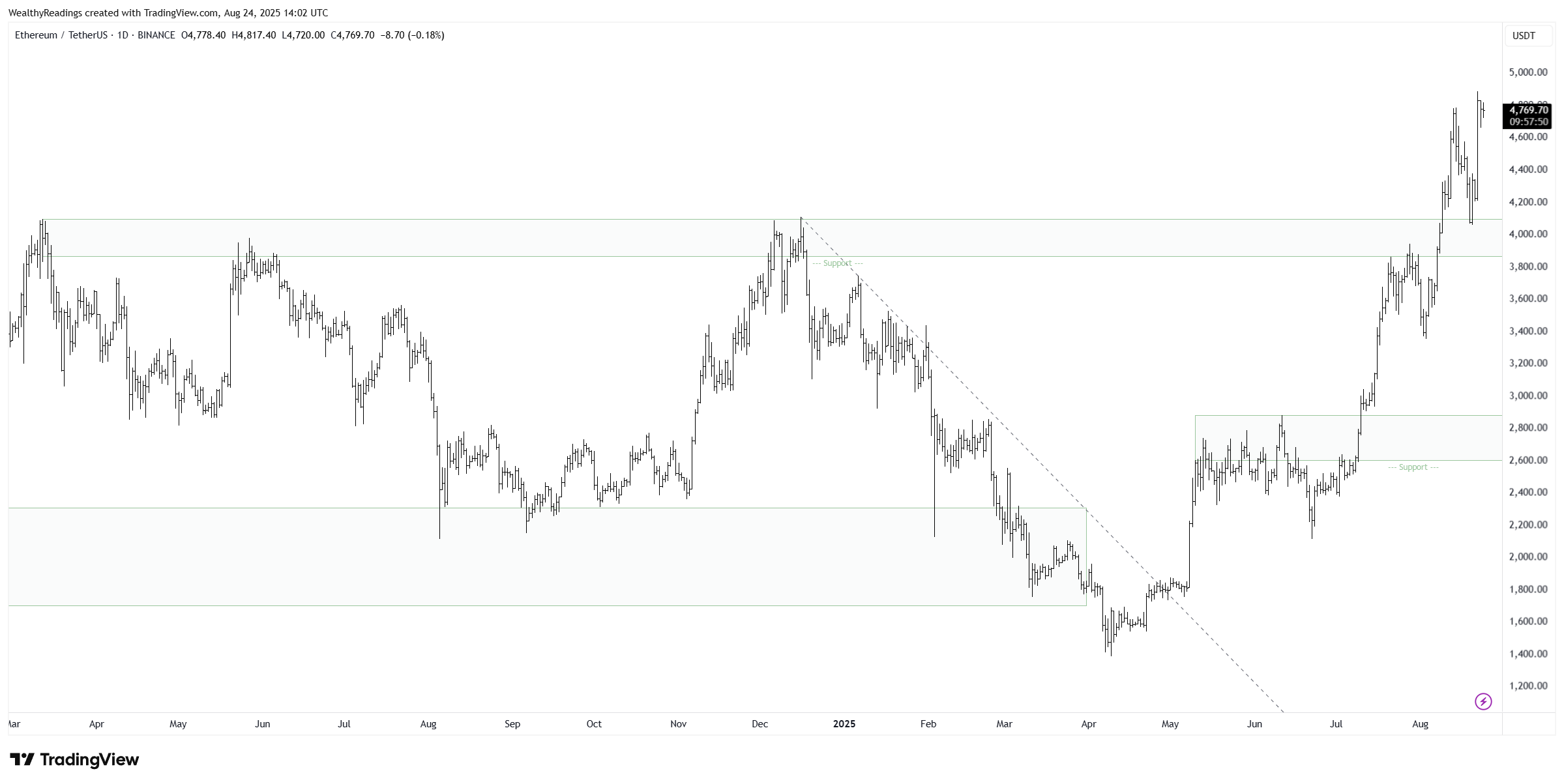

Ethereum jumped massively right after giving my $4,200 target, BMNR did the same and both those positions are up more than 10% since I bought. Notifications were sent to those who follow my Savvy portfolios.

More notifications were sent on the B&H portfolio after buying Nebius for example, already up 10% as well.

I still believe we will see some red in the next days and consider Friday to be a massive overreaction, but as usual: what matters is to have a plan and stick to it. My plan still is the same as when I shared this write-up.

Weekly Planning.

In brief:

Tuesday - Nebius Investment Thesis.

Thursday - Nvidia Q2-25 Earning Review.

I changed my mind & will send a renewed and very, very detailed Nebius investment thesis on Tuesday instead of the Arista Network investment thesis, which will come next week. I consider Nebius to be a correct buy at today’s price while Arista is still expensive, so it seems more important to have Nebius fundamental review right now for you to know everything about the stock and make your own decision.

Nvidia reports earnings on Wednesday so you can expect a detailed review Thursday, as usual. I'll also comment on some other earnings as we'll have PDD on Monday, Crowdstrike on Wednesday, and Iren on Thursday.

Thanks for the reminder that bond yields may not come down with the interest rate.

They could! But it's not automatic