Transmedics Conference & Position Review

Resume of the conference, review of my positions and convictions short & medium term.

Transmedics participated in the Piper Sandler 37th Annual Healthcare Conference, and the information shared was bullish - nothing shocking, but it reinforced many of the points I’ve been highlighting recently.

One of the main bull verticals - and there are more, relies on two core ideas:

Their hardware meaningfully improves post-transplant success rates.

Their ability to harvest DCD organs, expanding overall organ usage globally.

Put together, these two drivers should grow the market and increase TransMedics’ share within it.

For that to play out, Transmedics needs to keep proving the added value of the OCS and the NOP, and in medicine, credibility spreads through publications. The heart & lung OCS trials are ongoing and will lead to papers, but the company should also be louder about its liver data. The liver OCS has been used for years and steadily gained market share - hence clearly brings value.

Waleed confirmed that new publications are coming in early 2026.

As anything in medicine, it takes time. Publication need to come out. We are working on that pretty aggressively, both in DCD and DBD. We are making good progress towards achieving that goal. We’re working very hard with our lead users to make sure that these, major publications from those, you know, tens of, I mean, thousands of liver registry data come out, the first half of 2026.

This is not a small deal. If Transmedics proves clear improvements in post-transplant outcomes, adoption will rise as practitioners just want the best tools, and could even trigger regulatory requirements as governments also want better outcomes & cost-efficiency systems - which NOP is.

OCS machine perfusion based on 9,000 livers we have done, we are convinced that it should be malpractice if the livers are not put on the OCS. I mean, we are talking about significant survival difference, significant improvement in post-transplant complication rate. There are 70% of the DCD livers being thrown away every year. There is a huge opportunity for growth there for us. We know it because it’s coming out of our registry, and it’s gonna be unequivocal, showing the same great results that we’re achieving with DCD could be achieved in DBD.

If TransMedics becomes the standard for both DCD & DBD, backed by superior clinical results and a potential governmental push, growth could accelerate fast. Worst case: stable, steady growth for a long time, with a huge number of underpenetrated centers still up for grabs. That’s why the upcoming papers matter so much.

We are in the majority of the centers for liver. There are still few centers that are still holding back. Those are opportunities for us for growth. We have three categories of centers. We have the early adopters, and centers that have been using the NOP. They are penetrated at, you know, 80%-90%. You have the middle tier, 40%-60%, and you have the lower tier, which is 20%-40%. Those are the newer centers coming into the NOP family, figuring out reimbursement, you know, updating their Commercial Contracts, etc. Our goal, our plan is to move them from right to left, and our goal is to increase utilization.

This market will be conquered by growing usage & usage will be fueled by published clinical data. More OCS liver cases naturally means more OCS usage for other organs.

There’s a multi-flywheel in motion.

Looking forward, I used the company’s internal target of 10,000 transplants by 2028 in my valuation model. That would mean roughly ~$1.18B in revenue, putting the stock around ~$295 at a 9x P/S. Waleed confirmed the 10,000 number, but also implied it’s conservative.

The 10,000 is, as far as we’re concerned, something we are highly confident that we will achieve by 2028.

I interpret that as a floor, not a ceiling. Doesn’t mean it will happen, but this is what is said today.

Management is also targeting a 30% operating margin by then or about ~$355M in pre-tax income, or a ~30x earnings based on my previous valuation, still below industry comps.

On future growth levers, kidney is the big one and should start around 2027, as I’ve repeated many times.

In 2027, guys, we’re adding a new kid in the block called kidney. That volume alone is one and a half times the heart, lung, and liver combined. 23,000 kidneys transplanted last year in the United States, deceased. On top of that, there’s 10,000 kidneys that were rejected for transplant because of prolonged ischemic time. All of this will become accessible through OCS and NOP. That’s a huge volume that TransMedics has never experienced before.

They also talked about their planes and double-shifting.

Right now, NOP flights are capped at one per day per crew due to FAA rules - pilots need at least 12 hours rest after a mission. This limits OCS case volume today and will become a real bottleneck once they get toward 10,000 cases a year. Management is already working on solving this by doing more flights, before buying more planes. This starts next year.

The planes, our planes should run like Delta, like American, like United. They should be running 24/7. Now we need to generate the case volume to do that. To do that, we need enough pilots to do double-shifting per plane.

On heart and lung trials, Waleed confirmed they already did a handful heart with OCScases, and lung enrollment should start around Christmas. Same value prop as liver: more usable organs, more time, better planning, lower cost…

Those trials were, the heart and lung trials, simply stated, were designed to replicate the huge success in liver, which we can do morning-hour transplants or scheduled, scheduled transplants for the first time in history of organ transplant. That was a major catalyst for liver adoption, and we think that’s gonna be the same for heart and lung. It has never been experienced in heart and lung, for all the obvious reasons, the concern about ischemic damage. Now we have a mechanism that is gonna be hopefully reproducible and that’s just one major value that we are, we’re looking forward to achieving.

They also repeated details about the billing process - nothing new, but good to reinforce, because it could affect margins: TransMedics only bills transportation, while covering clinical costs.

Overall, nothing shocking in this interview. Many bullish confirmations for the short and medium term. I would have liked more color on Europe, but that’ll be for next time I guess.

Position.

As you guys probably guessed, this does not make me bearish.

The potential is unchanged, and management keeps reinforcing the bull case with data and execution.

I shared a few weeks ago my expectations that Transmedics would beat on Q4 based on flight data. November slowed down a little.

October: 773 flights → 24.9 per day

November: 763 flights → 25.43 per day

Based on my model, this means ~$104.8M revenues. Q4 could hit ~$158M at this pace, the high end of FY25 guidance; assuming no acceleration in December which should be the strongest Q4 month.

Speculations as always, but again: execution is strong.

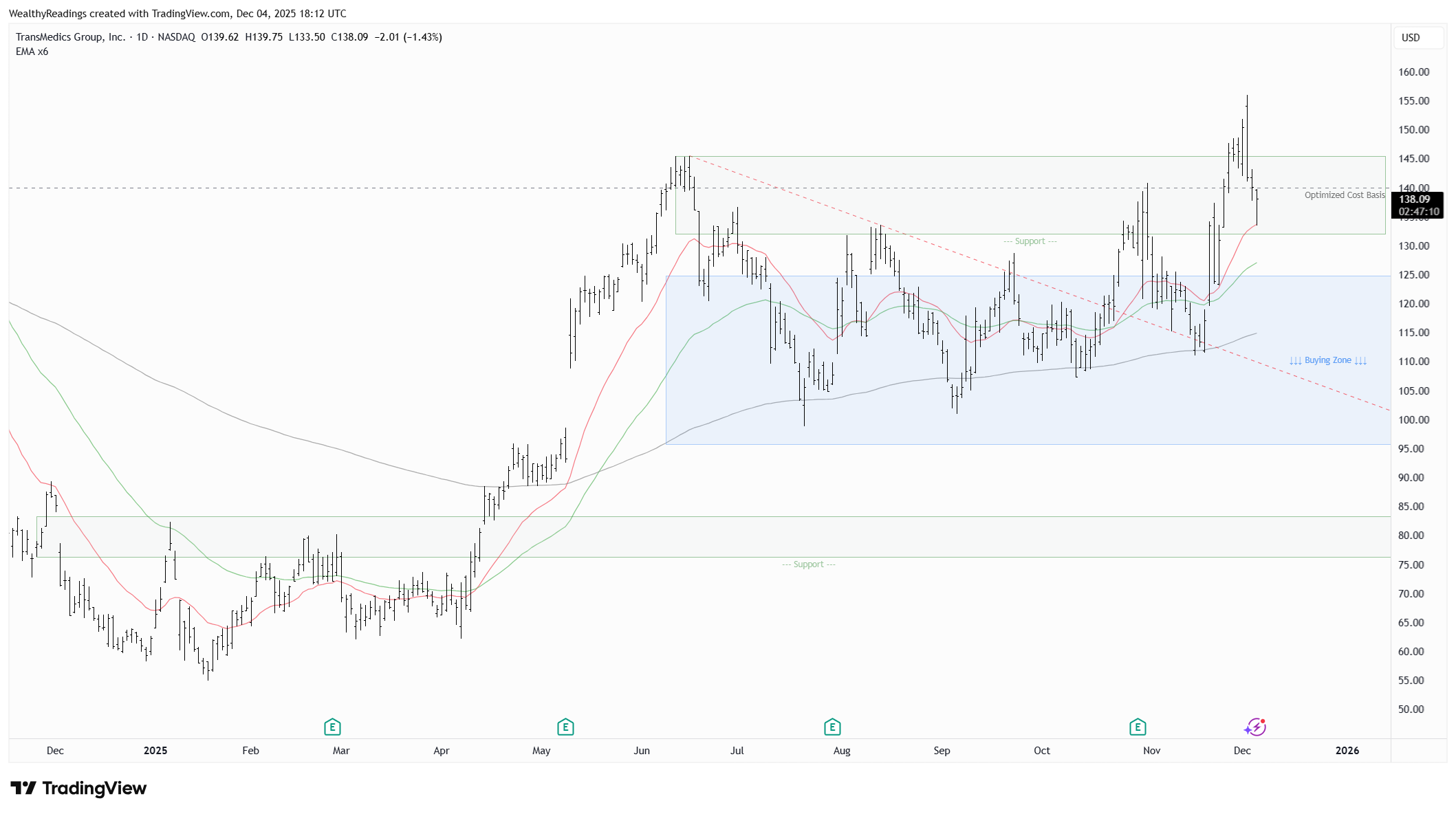

And price action is great. We had today a perfect retest in the $130s, bouncing right on the daily 21.

I said I wouldn’t buy more Transmedics two days ago, unless the stock came back into its range. I assumed we’d run higher first, then retest the $150 breakout. I also said on my valuation write up that I would certainly accumulate the $130 zone if it came.

Price action has been pristine and we are past the perfect accumulation point. We could see a deeper retest of the breakout, down to daily averages around $130. I would buy that retest, assuming no negative news.

If the retest doesn’t happen and we continue higher in the coming weeks, we’ll need to be ready for the $150 breakout to be retested at some point. That could also be a great entry, but I won’t speculate on what I’ll do then, it will depend on timing and context.

And so the retest came before the large breakout - which is healthier, and I ended up grabbing a bit more at $134 today, with buy orders right on the daily 21.

We could dip lower, we could take longer to bounce, we could visit the daily 50. No one knows. But everything is aligned to my opinion so I’ll keep betting big. And big can get bigger if the market keeps giving me opportunities.

I personally expect a new yearly high before 2025 ends, or very early in 2026.