Portfolio Modifications & Plans

Down double digits in a week, and still bullish

This week was shit.

But it had to happen. We expected it, I wrote about it less than a month ago. The index and many individual stocks were extended, we had made too much money too fast, and eventually most had to take profits and trigger a real selloff.

I felt like writing this weekend. First because I need to, second because I believe most of you would like to read some words. My personal portfolio is down 28% this week, which is a lot. I am guilty of the same mistake, always: overtrading. I always take too many side positions when the market gets excited and end up with some poorly timed entries. When that’s done on margin, days like these hurt. A lot.

I’m not here to complain, but to learn; that comes through writing. This Substack isn’t like others. I am not perfect, I am not here to tell you everything I do is perfect or that everything is great, that I have all the answers. I am here to share my journey toward being successful in the markets, so we can all learn, reflect on our mistakes, improve our systems, and succeed.

Losing so much money is also, somehow, a blessing. It means I was where I had to be over the last months, as most of the drawdown came from last month’s winners. I should have managed my liquidity better these past weeks but I was down a lot only because I was up even more. There are improvements to be made, yes, but also successes: the right stock picks, the right sizing. Important not to minimize those, as they are massive improvements compared to a year ago.

My portfolio is up 110% YTD. The alert portfolio is up 54.84% and the core portfolio 93.92%. Important to keep perspective, this isn’t a bad year, just a bad week, and we still have months to go. As my portfolio compounded significantly - up ~300% over the last two years excluding deposits, the numbers are starting to feel real in a different way. Losing ~$10,000 a few years ago felt manageable. When a weekly loss is counted in yearly salaries… it hits differently.

Never waste a good crisis. Churchill was right.

The lessons are manifold and I’ll work hard to apply them. I know exactly what I have to do, now I have to engrave it in my brain, build habits that stop the impulse to always take that one extra trade. Improve.

I do not have the perfect recipe yet. I only have the blueprint.

We’re building the rest together.

In this write-up, I’ll zoom out, justify this price action, think through what comes next, review key fundamentals and news, and conclude with my plan for the days ahead.

Markets, Selling & Fundamentals

Now, let’s focus on data. What happened?

My only answer is: nothing. Every asset class sold off, every sector sold off. Crypto is down crazy, gold and silver lost key supports, leaders saw double-digit drawdowns. Global selloffs usually happen for two reasons:

Investors flee to safe assets out of fear, but that requires a reason, which I don't see, and would trigger inflows on safe assets. Gold was down 5% in a week.

Classic liquidity cascade; most participants decided enough was enough, took profits, and triggered margin calls, stop losses, and every mechanism that comes with peak FOMO and retail optimism.

On the negative, the Strait of Hormuz remains closed, some strikes were apparently exchanged, negotiations stalled, and we are waiting on Warsh’s first rate decision mid-June. I’ve flagged this as a potential negative catalyst, though the market had already priced in no changes which should be what will happen.

So beyond wide profit taking after months of up-only and an extended market, I struggle to see any reason for our actual long-term uptrends to stop here.

So, what’s next?

Market-wise, nothing is certain. The S&P and Nasdaq were both extended, needed to breathe, and are breathing. Both broke their D21, their short-term uptrend indicator on higher volume, meaning lots of organic selling with few buyers stepping in.

Can you blame profit taking after 34.75% return in 45 sessions, and some patience before buying back in? I can’t.

The problem is that when buyers don’t step in to hold a key level, it means more sellers than buyers exist at that price. If nothing changes, Monday’s dynamic shouldn’t be different. If I didn’t buy potatoes today, I won’t buy them Monday if nothing changes. That said, the last two years showed markets can change their minds overnight and without any reason. Buy the dip has been the mantra for a long time. But statistically, more short-term pain is the more likely outcome.

The healthy targets are both W21, 7% lower on the Nasdaq and 4.3% lower on the S&P. And honestly, that’s what you want. Portfolios shrink more, yes, but liquidity flushes, overleveraged players learn a lesson, and healthy capital can re-enter at better prices to reinforce a longer, healthier uptrend.

Fundamentally, I believe the verticals I follow are stronger than they were a week ago.

Earnings this week from Credo, HP and Broadcom told the same story, again and again. AI demand isn’t just for off-the-shelf products, it’s for customized, optimized hardware that let hyperscalers deliver tailored compute to their clients.

Demand for XPUs and networking is simply insatiable. During the quarter, bookings for AI semiconductors were over $30 billion against the $10.8 billion we shipped.

Our visibility runs all the way to 2028 right now. Three months ago, I can tell you our visibility run pretty much 2027. Today, it runs to 2028. We're talking about capacity as measured by gigawatt power that are way ahead of what we have expected, say, six months ago.

Broadcom Earning Call

There's a reason when you've seen ASPs increase as much as they have over the last year, that customers are still saying, 'Hey, we want to buy. We're going to start new programs. We're willing to pay the higher prices because we clearly see that there's an ROI.'

When we talk to our customers, they're clearly at the early days of their Agentic AI journey. They see that they want their data to be more on-prem. They want to do more of the compute on-prem. We're seeing demand at the higher end of our platforms, so more memory, more compute power.

HPE Earning Call

Shocker.

On cybersecurity, both Palo Alto and CrowdStrike beat expectations and confirmed AI as a tailwind. Rubrik also impressed at its scale. This entire earnings season delivered one message: inference requires more hardware, more optimization, and AI is finally showing up in SaaS bookings and earnings.

I struggle to see how that leads anywhere but one direction: more.

Until now, infrastructure builders spent their cash flow, cash reserves and took debt, step by step. The only logical conclusion from those steps taken through two years is that they found ROI. If one were spending without reason, others would have held back. None did.

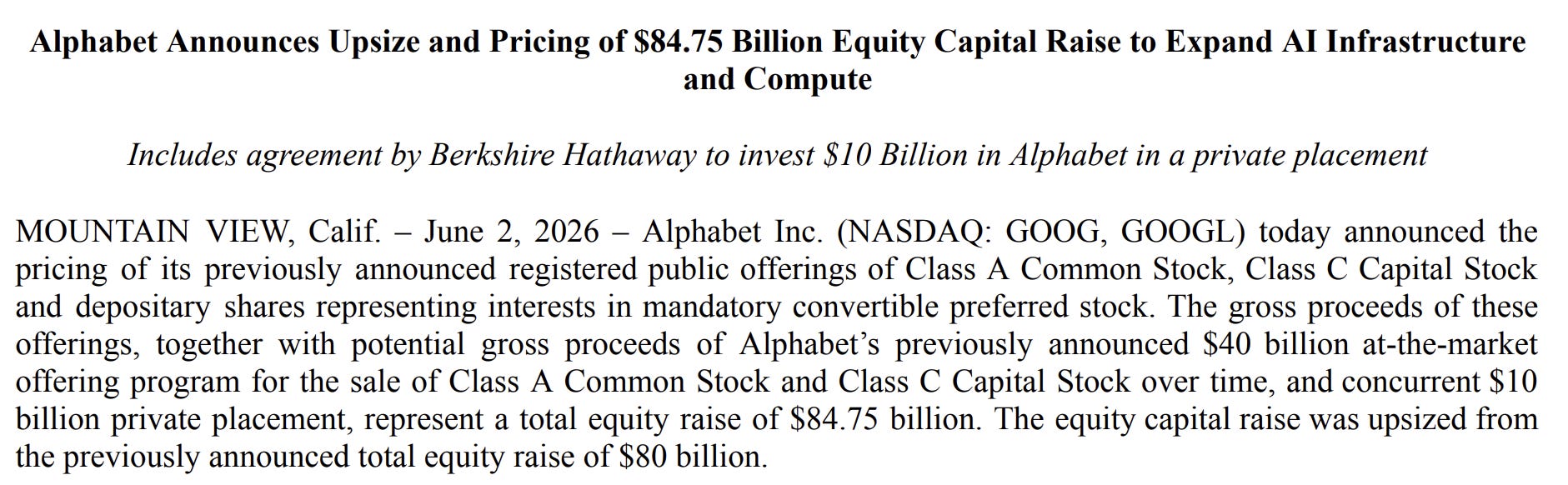

This week they took one more step: dilution. Google announced an $84.75B equity program. Meta announced plans for tens of billions.

I need to take a minute to explain the magnitude of this.

For decades, the Mag7 were the best investment; they were cash cows returning profits to shareholders through buybacks and dividends. Hundreds of billions went back to them, excluding price appreciation. They made so much cash they had nothing better to do with it than give back, please investors.

Google’s equity program tells you management now believes raising liquidity by any means necessary for AI buildouts is more important than decades of shareholder coddling. I’m not sure the market will like this, but it’ll have to make its peace with this decision. This is the new paradigm, join it or don’t.

This is a very powerful signal.

And it wasn’t the only one. Berkshire Hathaway participated for $10B to this capital raise. Buffett’s company, even if he’s no longer making the calls. The symbol matters, and the fact that they have ~$380B left in cash, meaning this could be a first injection. This is the first major institution, external to the AI ecosystem, injecting capital into AI buildouts. Until now, hyperscalers relied on VCs, cash flow, debt. Today, an outside institution is funding AI, and could open the door for many others.

Like… This one.

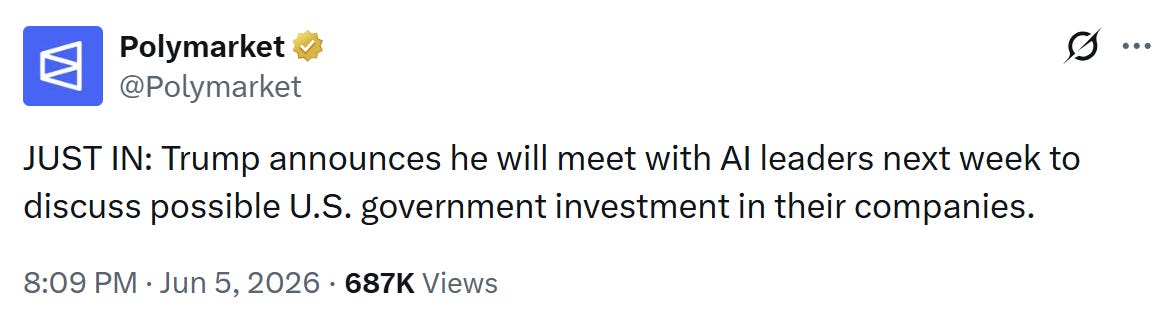

Today, AI is seen as a tool to increase profits. Eventually it will be seen as critical infrastructure for energy efficiency, medical research, public systems optimization, and maybe more... There is a case where states participate in buildouts or support through other levers as the technology becomes a national interest. Trump's administration already took stakes in companies like Intel, I see no reasons for this trend to stop.

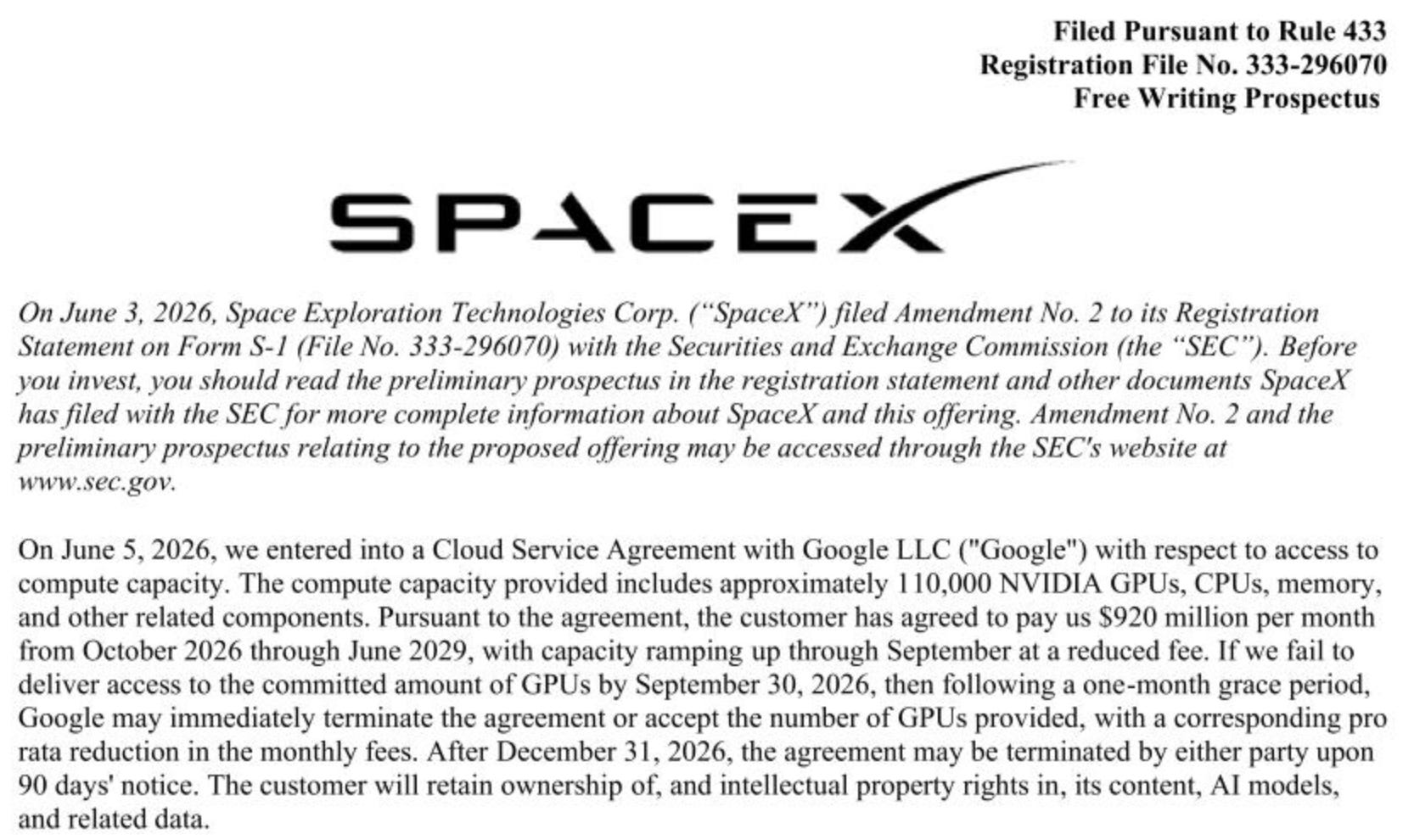

Lastly, we learned Google contracted SpaceX for $920M/month of compute over ~3 years, guaranteed for one. SpaceX is the only company left with available compute following its migration of Grok to Colossus II, freeing Colossus I.

I’ll conclude this fundamental parenthesis here.

Looking at my portfolio is rough, but writing this section is exciting. Every company involved in AI is telling you they’ll spend more or make more - or both, and what everyone called overspending last year will turn out to be the beginning of even more spending. Every analyst and management forecast 2027 CapEx increases each passing month. Google opened Pandora’s box with dilution. It is very hard now not to expect Microsoft, Amazon and others to follow, while external participants are also helping to fund those buildouts…

This is the state of AI demand. Even while stocks go down.

On the premium section, I will go over the opportunities and liquidity attribution as the market is shifting and it is important to follow, identify the best narratives/assets, as you understood my overall assessment of the situation.

Yes, stocks are falling. But it looks like only so they can bounce back harder.