Buying Plan & Portfolio Strategy

My portfolio, performance, views of the market and decisions

This can be considered a mid-month report, not something I usually feel the need to do, but I believe today’s conditions deserve some comments, on the conditions themselves and on the management of my positions for the next weeks.

The Current Market

I’ve been very bullish over the past weeks, and extremely bullish on AI hardware over the past months, making the sector my biggest position. But we are reaching some high momentum now, in terms of extension and short-term performance.

The S&P 500 is up 16.57% in a month and a half, the Nasdaq is up 26% in the same period. The first trades ~7% above its W21, 9.1% above at the top of the week, and the second ~12% above. This kind of extension is where retracements/stabilizations happen. I was the first one claiming for weeks that this was one of the most hated rallies I’ve seen and that we shouldn’t try to anticipate its outcome, but those words were written two weeks ago now and the situation is a bit different for me.

This is one of the most hated rallies I have seen. Don’t fight it, don’t try to assume it can’t run higher or longer. It can. The game is different when liquidity concentrates into a few names or narratives, and a hated rally can last longer than any bears would have assumed. It will end, no doubt here, but what we need to do is to be ready for when it does, not try to guess when or why.

This is where we think about turning down risk depending on our situations - and I’ll describe mine after.

Extensions aren’t enough to trigger a breather, even at this level. The market needs a catalyst, and even if it ignored it until now, it has one: inflation. Been talking about it for months now. It was - and still is, inevitable.

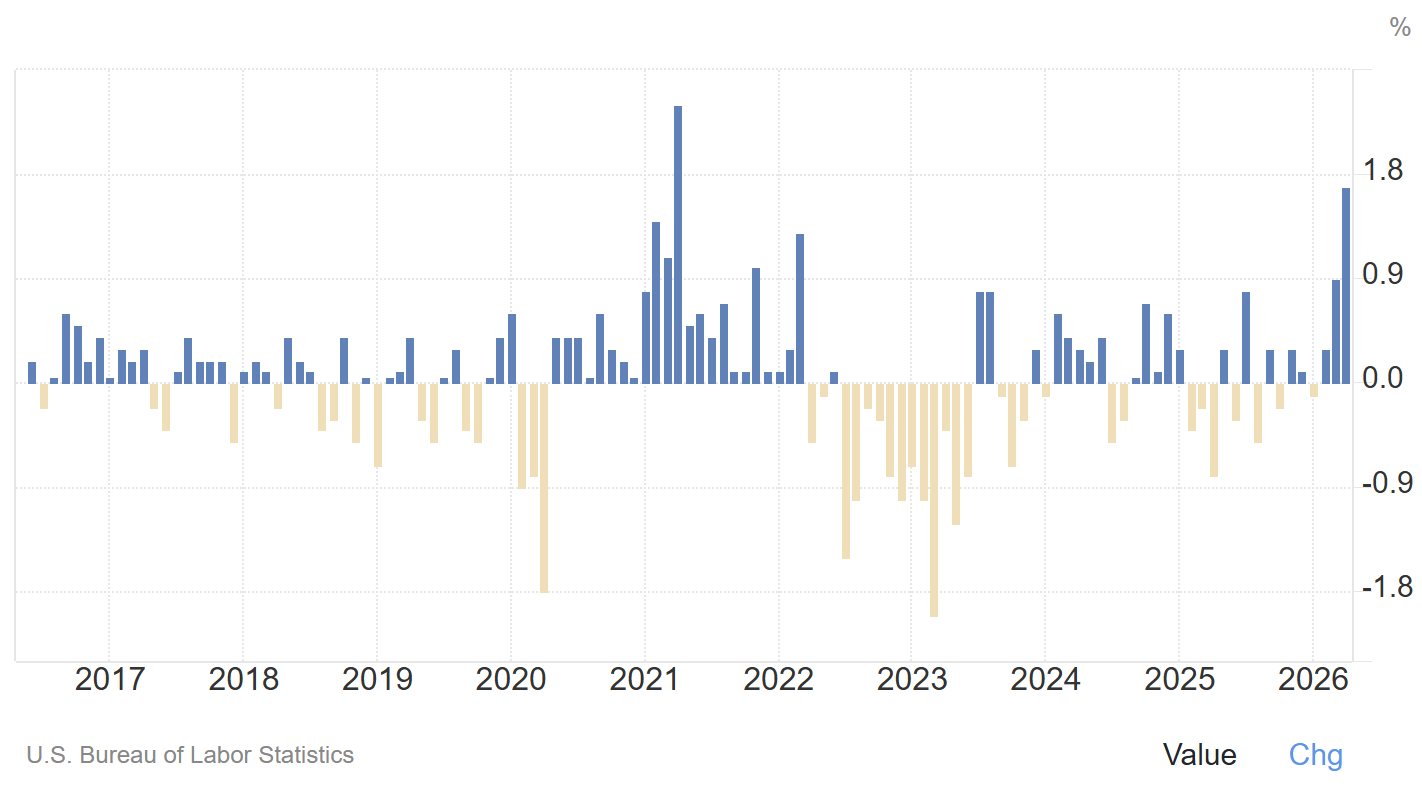

The Production Price Index jumped 1.4%, the biggest jump since covid’s supply chain disruption. Logical, as we are going through a supply chain disruption again, centered on oil/energy in general.

The PPI reflects price changes for manufacturing goods. Say I produce wooden chairs, I need wood and some other materials; the PPI will reflect the price increase of those goods. PPI usually is a pre-indicator to global inflation as if I, as a producer, have to pay more to manufacture my chairs, I’ll probably sell my chairs at a higher price to compensate.

We are at a month of disruption now, effects on the economy are real and won’t be fixed that easily even if we were to reopen the canal today, and no countries will be immune to the consequences. Even America, which has no/very limited exposure to Middle East oil will see inflation due to globalization. Any product manufacturing process goes through clear steps.

Material extraction → Transformation → Manufacturing → Commercialization.

If any of these steps get more expensive, the final product will be more expensive and as everything - most things, in the U.S. are imported then the life cycle of their products manufacturing will also be impacted by oil spikes.

So without any surprise to me, PPI is increasing, and prices should follow.

To be honest, there are no certainties yet as a temporary inflation could be absorbed by manufacturers who’d accept some hit on their margins in order to keep volume. Either way, cash generation declines for them.

But what matters in the markets is perception, and perception this week was that inflation is back, for real, with the 10Y back close to yearly highs, and that will raise concerns around rate cuts - and potential hikes.

We’ve talked about Kevin Warsh, the new Fed chair that was sworn in this week to take over Fed FED after J. Powell.

The market tanked following his nomination as investors worry Warsh ends up head-to-head with Trump and refuses to cut rates, which is what Trump wants.

I think Warsh will walk in and cut rates. Why? Because it’s the only reason Trump put him there. If Warsh wanted independence, Trump would have found someone else, someone more malleable.

The second problem is that obeying Trump creates even bigger issues as it means the FED independence is gone. If Trump - or any government, controls both monetary & fiscal policy, it’ll push America toward disaster: the last step necessary for collapse. It would take years, but it would be unavoidable as politicians abuse both frameworks and crumble the currency for political (and personal) gains. On the good side, assets would appreciate if that were to happen, but I am not sure what would be best.

The Fed next rate decision will be in June, all eyes on what Warsh will say for his first minutes, but as the Strait is still closed and we’re already seeing the accumulation of a year of tariffs and energy disruption… This kind of disruptions don’t disappear in a week, but in months from the moment flows restart - and they haven’t.

We have another variable with Trump meeting with Xi this week. Not much news yet but this renewed relationship could change lots of things for the world’s economy. The only valuable comments I’ve heard so far concerned agricultural imports.

Back on inflation, the only companies benefiting from this kind of environment are commodity sellers - usually, and we’ve been talking about lots of them over the last months so you guys should have options in terms of accumulation.

This is the market’s situation today. Extension, clear sign of inflation and fear of it. But that is only macro, and the market isn’t only affected by macro.

The AI Dichotomy

This is where things get extremely interesting. As the earnings season is over, we can all reach one clear - and unsurprising, conclusion.

AI is bigger than we originally thought, is generating more cash than we originally thought and will trigger more spending than we origin… You get it.

I’ve written four different earnings reports and covered ~50 companies, and all said the exact same thing: that they didn’t have enough compute, need more hardware, infrastructure, energy, and had so many clients fighting for their services that they ended up with pricing power.

The interesting part is that those companies’ final products are services, not goods; I’d go further as to call them deflationary services. Sure, to deliver those services, they need hardware and infrastructure whose prices are rising due to inflation and supply issues, but those companies have the cash to accept price hikes. Look at Google or Meta. When your core business is advertising, cash generation doesn’t change; clients rotate but cash still flows.

In brief. Companies with massive and constant cash generation can buy hardware at a higher price to sell a deflationary service to companies going through an inflationary spike, so they want to buy it.

So… Why would the AI cycle slow down, even if inflation spikes?

That’s from a business perspective. The issue with stocks is that they are impacted by liquidity. Investors sell during inflationary times not because they do not believe in the companies but because they need cash/are afraid of the market’s reaction/anticipate a correction. Better be the first one selling than the last.

It’s impossible to predict what will happen when it comes to the AI sector. But with potential inflation spikes, AI hardware seems to be the only sector that could thrive, so my conclusion remains the same as months ago: why touch any other sector than AI hardware and defensives?

Impossible to know what will happen, but it is possible to plan for the different potential outcomes. As long as I have a system and a plan, I’ll do well.

My Situation

My portfolio is up 141.20% YTD running at ~60% margins - I have cash outside of my broker so more like ~45% in reality.

Portfolio’s well balanced with 65% tech/risk and 35% energy/materials. This is what diversification should look like, I’ve written about this, you guys should go read this article if you haven’t.

Many investors believe diversification means owning different stocks. That is plain wrong. Diversification means owning assets that are not driven by the same narratives.

If you own both IREN and Nebius, or ASML and TSMC, you aren’t diversified; you are diluted. This is poor capital allocation because these pairs are highly correlated. You’d be better off putting your capital on the highest potential, and then seek for true diversification elsewhere.

I am now in a situation where I’d rather lock in gains and reduce margin to none, even maybe raise some cash. When you hit triple digit returns in five months, you don’t want to take too much risk if conditions aren’t perfect, even with a diversified portfolio. I’d rather chill a bit until the market gives clear directions.

We could have a healthy consolidation now. If so, I’ll have time to buy on breakouts. If we were to continue higher, I’d still be part of it without margin, with the certitude that a breather is coming and that slowing down isn’t a mistake. And if we were to have that breather, then I’ll be ready to go back all-in on key assets at great prices.

So for me, now is about reducing risk and getting ready for the next leg up, whether it happens after a rapid consolidation, or a deeper breather.

Now let’s dig into the specifics; my plan for each of my positions and the ones I want to buy/accumulate, at what price and priority.