Soitec Detailed Earning Review

Why would a 30% YoY revenue decline deserve 700% YTD performance

This is where fundamental investors and Excel moguls go crazy, this also is why they underperform and why the market is a special, extremely misunderstood place.

Soitec’s revenues are down 34% YoY. Most would say this is a dying business and its stock is not worth looking at, and yet… Well, they’re wrong. Earnings and financials look behind, they do not matter anymore as the markets price the future, not the past - which is why only guidance matters during earnings.

Soitec is up ~290% since I shared my thesis and made it my biggest position a few months ago, it is up ~20% more today while dropping a -34% YoY decline. And this quarter confirmed my thesis, that the future is bright and that the market should continue to push its stock.

Are Fundamentals Weak?

No. Soitec is at the heart of photonics. Optical semiconductors need SOI wafers and Soitec owns the most efficient technology to manufacture them cheaply and at scale. And while we think about data centers today, the truth is that SOI wafers will also be present in every hardware leveraging AI with a need for low latency in the future, which means robotics, EVs, 5G hardware and smartphone, and many more…

Many of the five billion AI device by 2030 will be always on and extremely sensitive to active and passive power consumption. We also expect AGI to drive new needs for connectivity with more data volume to be exchanged, lower latency, higher band, lower power consumption and higher integration.

So in conclusion, for both infrastructure and edge applications, we are targeting every layer of the AI stack with our expanding portfolio of engineer substrate.

This is a pretty large market until the end of this decade.

But yes, if you look at past revenues only, you will not consider Soitec. Rapid growth slowdown, negative margins, unprofitable - EBITDA profitable though with positive FCF. What’s to like here?…

Well, the narrative.

We have had all the confirmations we needed through this earnings season to have the quasi-certainty that photonics are the future and are about to become the most demanded piece of hardware in data centers whether within Nvidia’s GPUs or Arista’s XPOs. Any pluggable today and CPO tomorrow will include SOI wafers.

Customers come to us for prototypes and move from prototype to qualification faster and faster.

We expected around 30% CAGR but we are now expecting more, but we have to be humble in this industry, I will not give you a firm number.

[For photonics] we have new customers, in Singapore, starting prototypes from scratch. And we have more and more in the last months

This should add enough context to dig a bit deeper and you will find out some interesting things.

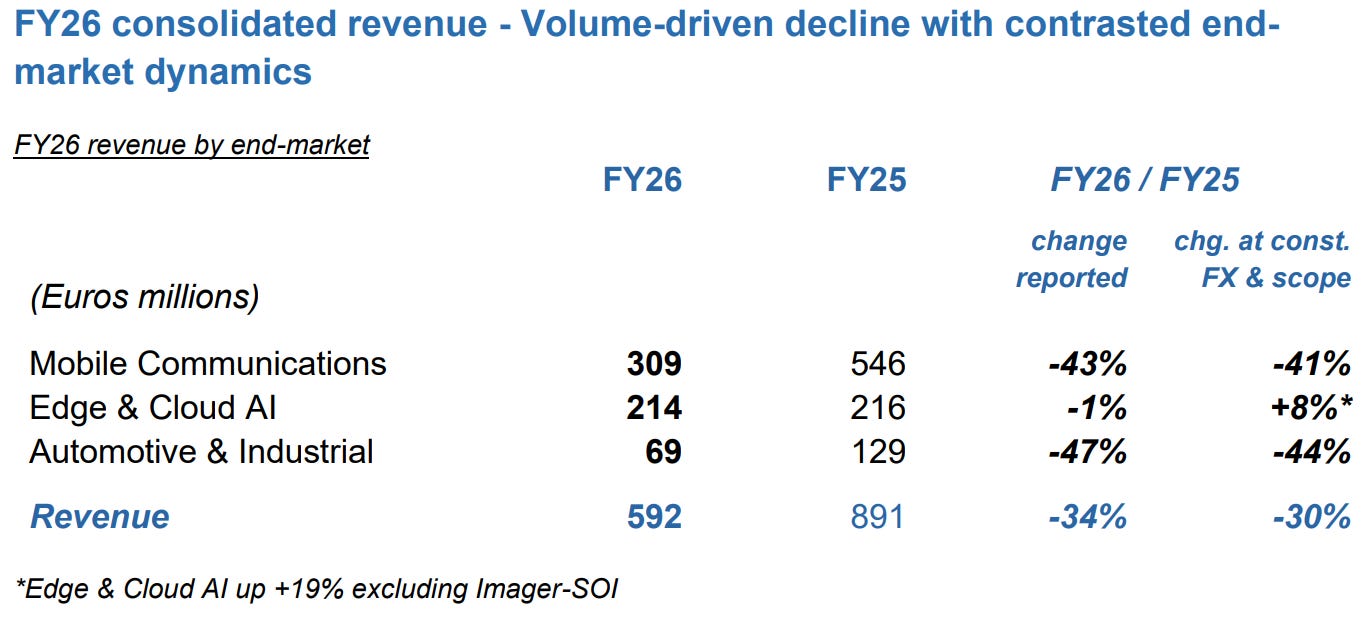

First, Soitec grew revenues 24% QoQ, exceeding their guidance of 20%. This is a lot, and doesn’t happen without tailwinds. Their photonics vertical was responsible for $100M of revenues FY26, which based on previous quarters indicates a healthy sequential acceleration - hence demand as the previous quote confirmed.

Photonics are still a new technology, at least applied to those use cases and are only starting to be tested now over the last few months, haven’t yet started to ramp up as confirmed by all hardware manufacturers those last weeks. Yes demand is rapidly growing but scaling such hardware requires time, and even more time for it to be represented in earnings deck.

This partly explains the “low Edge & Cloud AI YoY growth” as the technology needs to scale but there is more to it. Soitec stopped the production of its Imager products so the YoY comparison is unfair as including previous volume, discontinued today. Growth stands at a healthy 19% excluding this vertical.

This is the real signal about AI demand for SOI wafers.

This evolution reflects positive volume and product mix dynamics, notably in photonics-related activities, as well as the contribution of FD-SOI in Edge AI applications. Strong Photonics-SOI growth momentum continues, with revenue rising above $100 million in FY26, earlier than initially anticipated, marking an important step in Soitec’s expansion into high growth AI data center architectures.

Just like Global Foundries and just like we anticipated when I bought in Soitec months ago, the legacy verticals hurt its profile and will make the company looks like a dying one instead of what it is really, a transitioning one. Smart money might stop at this or not be able to invest yet as the profile doesn’t meet their requirement, but it doesn’t mean the narrative isn’t here.

Those are temporary setbacks until photonics become large enough to generate enough growth , or other verticals stabilize - which doesn’t seem to be the case. Management is dealing with this period as they should, with sane financial decisions to reduce spending, focus on its balance sheet and its production towards future core products: AI & Cloud photonics.

They confirmed that manufacturing capacity from those legacy verticals could be re-allocated towards other hardware, under more demand - understand photonics here, at low cost and short timeframes. In plain English: slow demand for other verticals means they are ready to use it to scale photonics more rapidly.

We can scale by reallocating fungible SOI capacity already installed without years of capacity ramp and qualification.

This decline is legacy demand might end up being a blessing.

So if you focused on financials without looking at the context, sure, this quarter looked shit. But when you add context, fundamentals and market trends, well… A shitty quarter becomes the confirmation of a bull case. It will take time to materialize, but the market will continue to anticipate it.

Because that’s what markets do, they anticipate.

Unfortunately I missed the boat waiting for a pull back. Still running wild.