Alibaba Q4-25

Everything. All at once.

The thesis is not broken, but it isn’t perfectly healthy neither. Alibaba remains a great company, in transition from an e-commerce platform to a vertically integrated AI services provider. It still has a lot of potential, even if the overall picture isn’t the best today...

As for investing, Alibaba is officially no longer a stock I can hold, as it has been trading below its W50 for several weeks and this quarter didn’t show what I wanted and was not received positively by the market.

I have a system, and I follow it: I do not hold weakness.

We rode this name from $80 in December 2024 following a clean W50 retest after a high-volume breakout, delivering 53.01% returns vs. 7.26% for the S&P 500, an alpha of 45.75% over a year and three months.

Vertically AI Integrated

This is a major part of the bull case as Alibaba owns the entire AI stack, from infrastructure to software, including models and end users. This is what could drive above-average growth in the coming years and what the company has to leverage - and they are doing so.

Looking ahead, we are well-positioned to drive growth on both enterprise AI and consumer AI fronts, powered by our fullstack AI capabilities spanning foundation models, cloud infrastructure, and proprietary chips, alongside deep integration with our broader ecosystem

It showed this quarter with continuous acceleration - slower but still here.

Management confirmed that their AI services continue to capture a large share of the Chinese tech market. This is key to the bull case, as the country is accelerating its AI transformation and demand is - and will remain, massive.

Alibaba Cloud continues to lead the market, attracting more customers to onboard our comprehensive AI+cloud products and services, including high-performance networking, distributed storage, cloud operating system, and services for model training and inference.

They also confirmed growing adoption of their AI services by end users, beyond internal optimization and compute usage, which is another important signal as this is how they leverage the final consumers into revenues.

Since launching its Chinese New Year campaign on February 6, Qwen app has seen tremendous user engagement. By the end of February, approximately 140 million users have had their first AI-driven shopping experience through Qwen app’s agentic features from ordering food and groceries to ticketing and travel bookings. In February, consumer-facing Qwen has surpassed 300 million monthly active users across all platforms.

There isn’t much to criticize on their AI/cloud execution. This is what I want to see and the company is moving forward really well, even if growth acceleration slowed a bit this quarter; the market may be frustrated but this could simply be a temporary pause before a second ramp-up.

Local Consumption

The first issue is exactly where expected: Chinese consumption. I remain bullish long term but the Chinese government only deploys targeted and gradual stimulus, unlike the liquidity expansions in the U.S. where it is accepted to just throw money into people’s pockets. Not even talking about the cultural trend of saving...

And so what looked like a promising acceleration was hurt this quarter with a big sequential growth decline.

No magic here, deceleration comes from lower consumption and a normalization of their fee programs which was modified a year ago. Not what one wants to see for an e-commerce platform but this isn’t the source of growth nor the bull case either way, it was only meant to be the source of cash generation to fund their AI expansion.

And this is where the real problem lies this quarter.

Growth Without Cash Flow

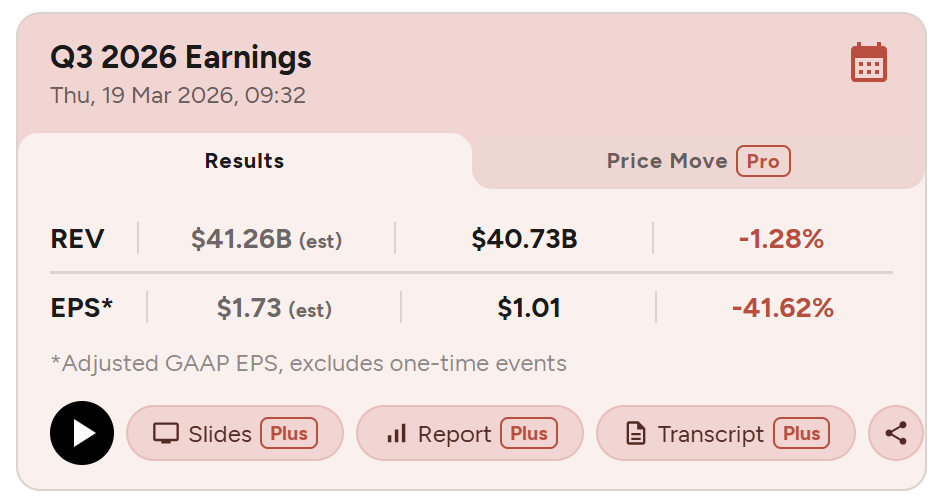

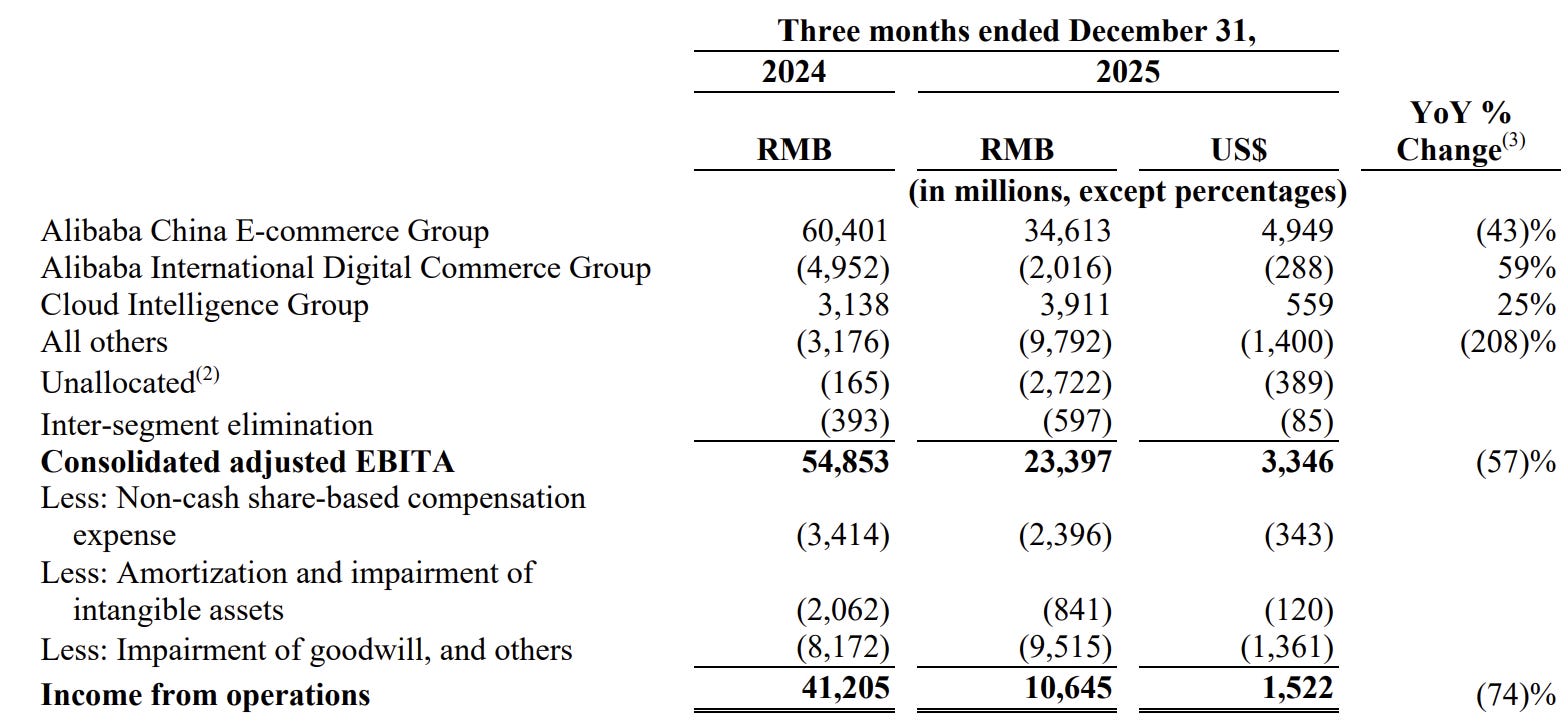

To expand AI infrastructure, you need cash. And this quarter, Alibaba saw a 2% revenue growth - which should have been a 9% without the negative drag of Intime and SunArt, for a -74% decline in operating income… What happened?

Management decided to scale meaningfully its investments, but not only in AI and clouds, also in their e-commerce business and quick commerce infrastructures, yielding a 43% decline YoY in cash generation from the stable source, from the vertical which was supposed to generate cash to expand AI.

Can’t help but see Obiwan Kenobi screaming “You were the chosen one! It was said you were to destroy the Sith. Not join them!” Well apparently management thought it would be great to spread spending between two verticals instead of focusing only on one and do it well.

On another hand, the small foot print taught us that some of the AI CapEx spending was reattributed to “All Others”, so even if the cloud vertical seems healthy the real EBITDA and margins of this vertical alone is probably not as shinny as displayed.

I believe the market is fine with their cloud situation and even this accountability trick. We’ve seen it in the west: you need to spend to grow and Alibaba has a large opportunity ahead plus very stable finances which allow spending. The issue is about spending on an e-commerce platform without much ROI as their quick commerce, which “only” is growing 20%+ is not generating much cash…

Management is going all in on two capital-intensive verticals at the same time without comparable returns. Why? The funds required for tech are already so large, why split them? Why now?

I know my bull case relies not only on AI but on AI application and Chinese consumers, so this is a step management has to go through, they have to invest in their e-commerce platform, but there is a time for everything and trying to go through two capital intensive transformations at the same time while cutting massively your cash generation doesn’t seem to be the right approach…

It can work. But the risks are huge and vision/execution must be flawless.

Investment Strategy

So as I shared earlier, Alibaba does not meet my criteria anymore.

The thesis isn’t broken per se but it isn’t true anymore, not in the form I was expected and as management decided to play the game in hard mode, the market is not going to reward them... It already struggle to accept the risks to fund AI datacenters in the west so it certainly won’t reward a Chinese company with comparable challenges plus spendings on another vertical with lower ROI.

What if they run out of funds? What if they execute wrongly and have to come back on some of their decisions? What if they misunderstand the market or the technology’s potential? What if one vertical slows down the other? SO many more what ifs.

They have/had the chance of being the #1 AI service in China with a complete dominance while keeping their status of #1 e-commerce platform but decided to gamble both with massive spending instead of having a clear focus.

It doesn’t meant they won’t succeed. It means they are making it harder than it should and the market doesn’t like harder than it should. One mistake could set them years back and slow everything down.

The market obviously doesn’t like it. The stock lost its W50, lost its higher low and fell harshly post earnings with high volume, meaning lots of investors unloaded their shares accepting a lower price for it.

I am very bullish on China and on Alibaba, but the gamble they are taking isn’t worth it right now, the market doesn’t want it: so I wouldn’t want either. I did not have a position personally and was waiting for the earnings to take a decision, which is that I’ll stay out. And as the stock doesn’t meet the criteria anymore, I also closed the position on my stock picking follow up website.

This is the end of Alibaba for me, at least in term of positions. I will continue to follow the company as a massive potential and the #1 Chinese cloud, but investment wise, I will need more to start another position.

As shared at the beginning, I am closing a position with great returns and am very happy with the trade. Hopefully, Alibaba will give us more. Until then…

Farewell.

Disclaimer: I am not a licensed financial advisor, analyst, or broker. This content reflects my personal opinions and investment decisions for informational and educational purposes only. I hold positions in securities discussed and may buy or sell without notice. Nothing here constitutes a recommendation to buy, sell, or hold any security. Past performance does not guarantee future results.

Always conduct your own research and consult a qualified professional before making investment decisions. I accept no responsibility for any financial losses.