Alibaba Q2-25 | Earning & Call

The thesis slowly unfolds... Slowly.

If you guys are interested, you’ll have 15% discount on FiscalAI subscriptions through my referral link. FiscalAI is the tool used for KPIs on all my write-ups, really powerful, valuable data & great UX.

https://fiscal.ai/?via=wealthyreadings

Everything you need to understand Alibaba’s investment thesis is here.

The quarter is better than the data makes it look, and we’ll detail everything below.

Business.

The investment thesis continues to play out, a bit boringly but patience is a virtue in investing. The thesis reamins that Alibaba will be the #1 or #2 cloud and AI service provider in China as the country will not rely on American services, while the e-com branch continues to grow healthily, with a potential acceleration depending on Chinese consumption.

Local E-com.

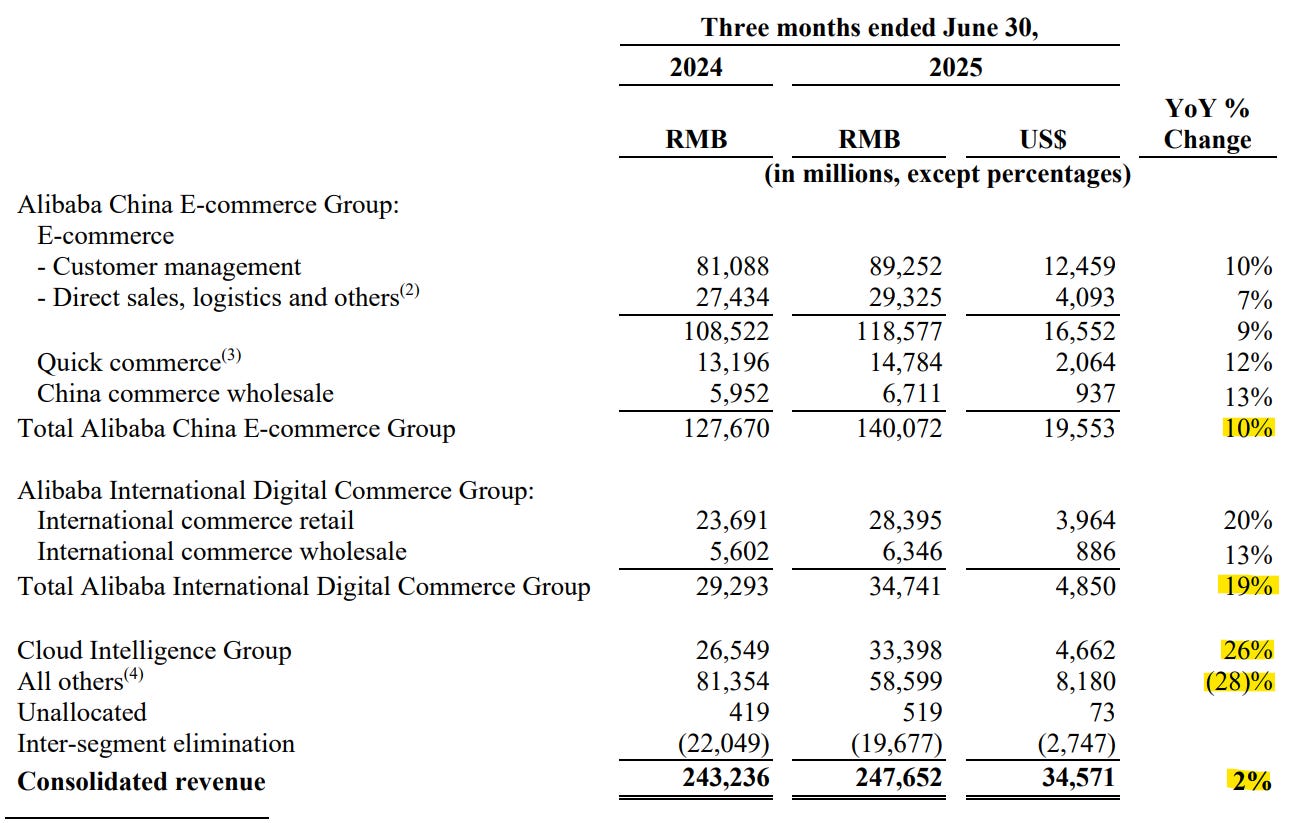

Overall, the branch is growing well with a 10% revenues increase YoY, but the details aren’t exactly what we’d like to see, although they could point to exactly what we want, but we’ll need more confirmations.

Alibaba’s local e-com revenues are divided in two sources, customer management & direct sales. The first one includes merchants advertising and promotions, the second direct sales, platform fees and logistics - Cainiao.

What we want is a growth from consumption, not services, but I’ll add management’s comments before sharing my interpretation.

Customer management revenue increased 10% year-over-year, primarily driven by the improvement of take rate.

Direct sales, logistics and others revenue under E-commerce business increased 7% YoY, primarily driven by the increase in revenue from logistics services, partly offset by the decrease in direct sales revenue as a result of our planned reduction of certain direct sales businesses.

Advertising spending is growing, take rate is improving, which means customers are reacting to those ads. And yet, consumption in declining - in volume at least. And merchants’ still spend more in logistics.

I could be worried as it seems like merchants pay more for less sales, but advertising spending is a choice. The bear argument could be that Alibaba has too many and too high fees, stealing merchants. But that would go against the increase of advertising which is a merchant choice.

So my personal conclusion would not be bearish. On the contrary, as I would see this as merchants’ optimism on Chinese consumption. They grew advertising on Alibaba’s platforms because they expect to get returns. Those returns haven’t manifested yet, which leaves one question.

Is it a last attempt to boost consumption? Or is it the first sign of consumer spending growth? We cannot reach a finite conclusion but again, I continue to lean bullish, and there are more hints that make me do so.

The number of 88VIP members, our highest spending consumer group, continued to increase by double digits year-over-year, surpassing 53 million.

Our significant investment in quick commerce focused on building consumer mindshare and business scale, which contributed to the 25% year-over-year increase in monthly active consumers on the Taobao app in the first three weeks of August.

Plus some comments from the call.

From July onwards, in particular, the growth of order volume, user scale, merchant supplies and delivery capacity have all exceeded expectations. In fact, if you just look at the food delivery to home category, we are now already the market leader. In terms of orders.

The only valid conclusion to reach is that merchants are growing their ads spending and working at reaching more consumers, with better results thanks to Alibaba’s efforts in AI. Management’s comments points to this being the start of a growing consumption, but data is not there yet.

Which leads us to our second subject.

Cloud Business.

Less speculation on this one as the result is clearly positive with a continuous growth acceleration as demand for AI & cloud services grows.

AI-related product revenue maintained triple-digit year-over-year growth for the eighth consecutive quarter. As AI demand continues to grow rapidly, we are also seeing increased demand of compute, storage and other public cloud services to support AI adoption.

The AI revolution doesn’t just happen in the U.S. and as said earlier, China will need to have local providers and Alibaba is the best horse to make it happen. They don’t only focus in AI services as their business also includes cloud services, which will grow in parallel.

This remains the differentiating factor for Alibaba, and the reason why I own the stock instead of any other Chinese e-commerce. Alibaba has it all, and all its branches work together, improving themselves and therefore the entire group results.

International E-com.

On their international e-commerce, growth continues to slow down but we are finally seeing the end of the tunnel on profitability with a flat EBITDA - almost with $8M of loss, for the quarter.

This doesn’t mean we will have constant profitability but Alibaba now focuses on it. As a shareholder, I’d rather see investments slowdown in its international e-com & grow in AI and Cloud services, which is now a bigger source of revenue, cash, growth, and a much more important asset.

Semiconductors.

There are rumors about Alibaba entering the semiconductor game, engineering their own to supply the Chinese market as the tension with the U.S. and export controls on Nvidia chips is still in effect.

Those are only rumors until today, nothing was shared by management. There are no smoke without fire usually but nothing official yet, and I am not sure how this could be done and how this would fit within their business.

Competting with Nvidia is not easy, as the U.S. market learned, and Huawey is already on the market with much more knowledge than Alibaba… I’d rather see management focus on AI services, but let’s see where this goes before commenting on it.

Financials.

Some more comments on the group’s revenues as we could question what happened as a 10% Chinese e-com, 19% international e-com and 26% clouds growth resulted in a 2% YoY revenue growth for the group.

The answer is simple, Alibaba sold two of its retail store branches early 2025, Sun Art and Intime, which revenues were included within their “other” branch. The revenue comparison is hurt as those aren’t part of Alibaba anymore. Excluding their impact, the group would have grown above 10% YoY.

The data is rendered a bit bearish but the fundamentals are really bullish. No Alibaba investor really cared about those two retail chains & it’ll allow the company to focus on more important branches, and use the cash from those sales to invest in more valuable assets - notably its cloud business.

As usual, data without interpretation is useless, so this is clearly not a problem for our investment thesis, on the contrary. In brief, pretty satisfied so far.

In the less satisfying, there have been lots of pressure on Alibaba’s EBITDA margins, due to investments.

Investments in Taobao Instant Commerce, user experiences & acquisition, technology for the Chinese e-com branch, investments in infrastructure for the Cloud branch and improvements on the international branch with better operating efficiency.

Those investments are normal and necessary, as long as they bring growth, especially as they do not bring the group’s margins down significantly. They led to a negative FCF and less shares buyback with only $815M spent. I wouldn’t complain as this is how organic growth happens in tech: with large investments. Alibaba is still very confortable with slightly more than $40B in net cash.

We’ll need to monitor growth but this quarter should be the start of confirmations for Alibaba. We need acceleration, to justify the investments & the return of consumption locally.

Investment Execution.

There is nothing really bearish here and even if there are some unanswered questions, I personally consider that the data is pointing towards bullish outcomes, as I do not believe that merchants would spend with higher take rates in despair, especially with the comments made by management and the latest economic data from China.

And while local e-com is healthy at worst, the trend for Alibaba’s tech is crystal clear: an accelerating demand growth for AI services and therefore other tech services. The AI revolution was massive in the U.S. and China is getting, with less focus on it from enterprises hence less demand - although their physical AI is close to be on maybe on par with the U.S. But the country is bound to follow America’s path, and if Alibaba succeeds at being the number #1 provider… The opportunity is massive.

I won’t redo my valuation, I still consider $140 or so to be a fair average price for the stock, so I remain bullish and will continue to buy in both Alibaba and the China tech ETF as it is a global revolution and not just an Alibaba revolution.

In term of price action, nothing really new despite today’s beautiful green candle. Still within an accumulation range, which can be bought at any moment or on lower timeframes retests.

The China trade will span over years. We still have time but this quarter is potentially Alibaba’s inflection point. If merchants’ advertising spending growth is indeed the precursor of a growing local consumption… The train will leave fast.

Hard to see when Chinese consumers would start to spend more and at what pace; but AI is a state driven effort to be used in “every aspect of life and production” - BABA is definitely a big part of it.