Alibaba Group - Investment Thesis

The unloved one.

Let's travel outside of the U.S for the first time, outside of the E.U and far away from the western stock market, to the complete opposite side of the globe and to a misunderstood country. Let's talk about China and its e-commerce companies.

More precisely about Alibaba but there are other opportunities in the Chinese market. I’ll try my best to explain why it isn’t a crazy idea to buy their stocks. And why the potential outweight the risks to my opinion.

[Company]

I'll start by talking about this giant octopus founded by Jack Ma in the late nineties, an animal very hard to categorize as they're now present in many different markets and are apparently not planning to stop their expansion - behaving like a very famous western company we will talk about later...

Let's detail a bit their businesses.

TaoBao, TMall & Chinese e-commerce. The heart and cash flow of the company, the original business created in 1999, not very long after Jeff Bezos' Amazon saw its first lights. It was of course different than what it is today as it started as a B2B e-commerce, meant to export Chinese resources to anyone who wanted them.

Things evolved and expanded from here as Alibaba added retail to its business and developed different apps which became the must use in China & Asia - apps like TaoBao, the most used app in China, or TMall in the top 10 are owned by Alibaba Group.

Those apps are very different from the one we're used to as they're based on the Chinese culture, very gamified. But the core principle and functions are equal to our Amazon. Find everything you want, buy it at the cheapest price, be delivered as soon as possible, and have some perks if you subscribe or if you use the application often enough.

Everything is meant to allow the end user to find what they don't want nor need and to make them buy it, and it works. So well that the company decided to expand even further.

AliExpress & Internationnal e-comerce. And what's better than to target western societies with cheaper Chinese products? Probably nothing so that's what Alibaba did next and it is working perfectly as AliExpress became the number #1 e-commerce platform in terms of volume in Europe last quarter - according to the Cross-Border Commerce Europe.

This is a pretty big achievement when you compete against Amazon.

Cainiao. We enter into the less known businesses of Alibaba now with their logistic branch, which is a pretty important one when your main business is to deliver things to retail, and surely better to own internally than to rely on third parties. I assume this was the logic.

This is a separate branch but its goal is to deliver what is bought from their apps, everywhere. It allows Alibaba to set its own rules like proposing the 5-day deliveries to Europe for example, which is surely something very hard to propose - or very expensive - if they were to use an external company. It still is with an internal one but at least they manage it as they want.

Cloud & AI. This is completely outside of their main competencies but also completely adequate to China's growth and innovations need. I have talked extensively about how China wasn't a dying country but a transitioning country, passing from attracting external investment with cheap labor to growing internally through innovation.

https://x.com/WealthyReadings/status/1707408948876226903

And innovation nowadays means computers, data, AI… And to do that, you need infrastructures. A very intelligent investment from Alibaba as we also have to understand that because of their politics, young tech companies surely won't have the rights to build services through Amazon or Google clouds. No, they'll need Chinese infrastructure so that the data can be overlooked and controlled.

And Alibaba's cloud branch was built.

Ele.me & Digital services. This part of Alibaba contains other smaller bets like Ele.me which can be compared to Uber Eats and more. I won't dive into those as this doesn't really impact the investment thesis but it goes with Alibaba's long-term plans: to develop & own different businesses.

There are more than Ele.me, with cartography apps or a Booking-like application. We could call this branch "side bets" and they definitely hold tons of potential but I consider them like what they are: bets. Great if they work while not hurting the group if they don't: only potential upside.

Digital Entertainment. I won't go further here, it's nice to know it exists but it is irrelevant to my investment thesis so know it: One of their branches do movies & more.

[How do they make money]

We've seen what composes the Alibaba Group but before seeing where the cash comes from, let's start by digging a bit into what the group exactly is: A start-up incubator fueled by one cash sh*tting business.

The goal of Alibaba was to grow its Chinese retail business - which it has - and to fuel other promising businesses with the cash generated by it. And things are going well for now.

Hard to deny that the strategy is working although yes, the cloud business isn't growing as fast as we'd like for such investments. But it is growing, and the rest is showing very strong results.

This only shows the good side of their strategy and we didn't properly answer the question of where the money comes from because there's only one answer for this: The Chinese e-commerce branch. This is the cash sh*tting business and everything else is simply burning this hard earned cash to grow and one day, be profitable too. Probably to fuel later branches’ growth.

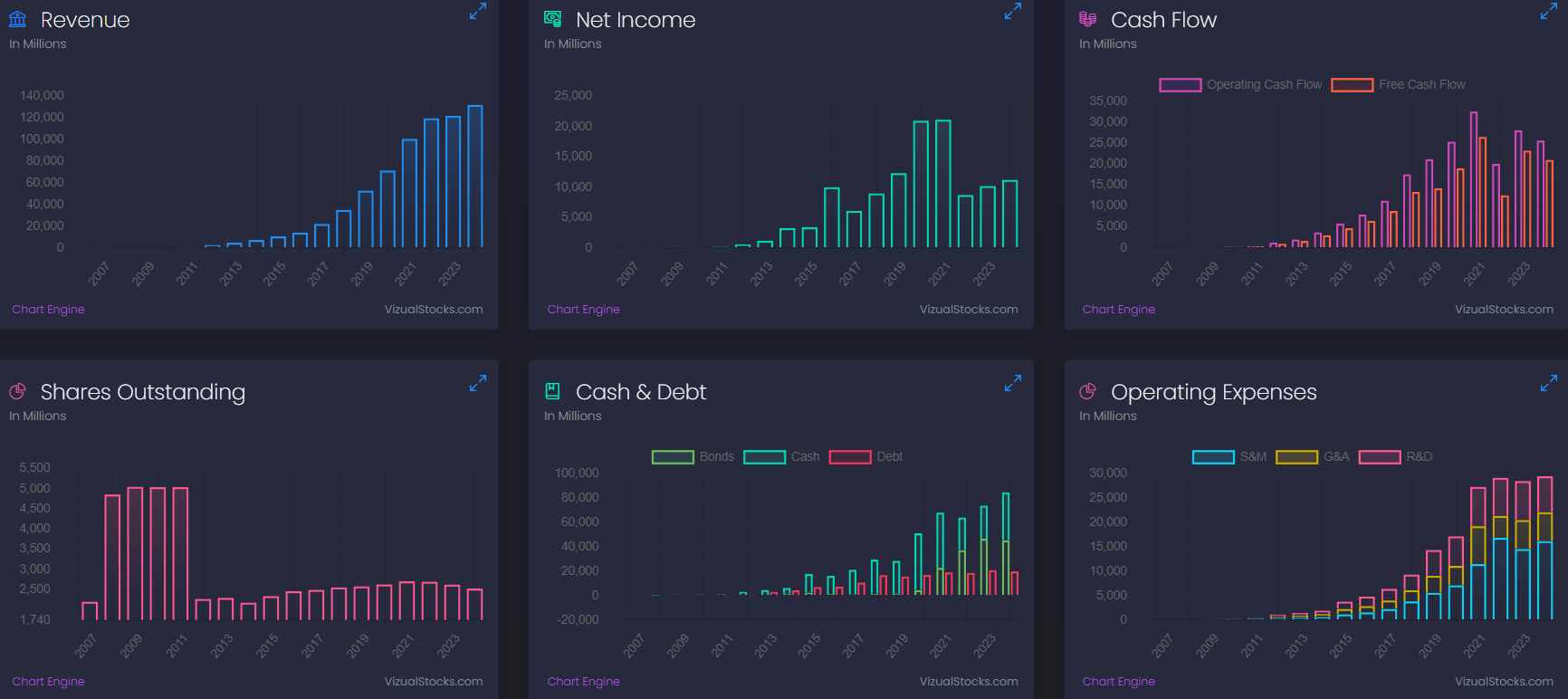

This is from Alibaba's Q1-24.

The cloud branch was profitable tis quarter and last year, but all the rest is red - yet the final income is green. This is Alibaba's strategy and it comes directly from the playbook of one of the most influential and important companies of the world.

Amazon.

[Market]

China is pretty good at stealing and if you did study their culture, you'd know it's not a big deal at all for them to do so. Industrial espionage is normal for them, I wouldn't go as far as to say encouraged but well... It is. So there's absolutely no surprises to see that Alibaba is simply trying to replicate what Amazon did in the U.S. The only difference is where they're doing it, although in 2024, where you're selling doesn't really matter anymore...

I will focus on e-commerce here and forget a bit about the cloud business because the first still is the heart of Alibaba & my investment thesis.

The market is... Huge.

There also are a lot of players but not many succeed... When consumers are used to one app they tend to stay with it except if something really important changes or if competition brings something much better. And that's what Alibaba and China, in general, did by pressing their advantage over the west: cheap products.

We use Amazon in Europe for almost everything because it was without any doubts the best service anyone could have. But over the last years, Chinese platforms rose and proposed equivalent services with cheaper products - hence AliExpress being the first e-commerce platform in Europe last quarter.

They won the heart of lots of users.

[Finances]

And they've done so as I said, following the Amazon playbook with one small but important tweak: profitability & stability. They waited for their Chinese e-commerce to grow and generate cash before burning it into other businesses, unlike Amazon.

It allowed the company to do things a bit differently while still growing with an astonishing 33% CAGR over the last 10 years. Being profitable helped them grow a very strong balance sheet with a $56B net debt and to bring back value to shareholders through both dividends & shares buybacks.

The company's net debt is worth 30% of their valuation as of today. And that's a big part of the investment thesis I will detail in a few minutes. First, the risky part.

[Risks]

I've seen lots of comments on X talking about "investing in the enemy" or "investing in a dying country" or, the last one, "you gotta be stupid to invest in China". Sure things, there are risks, like in everything you do in life - getting out of your house is risky but staying in also is!

Everything is about balance.

China/CCP. This is the risk many talk about. China is a communist country and you cannot trust a communist country for lots of reasons. They could force Alibaba to behave in ways that would hurt the business in the interest of the CCP. They could simply make the CEO disappear (he's back now). They could go as far as confiscating foreign shares as you do not really own them either way in China.

Those things could happen, but behind every risk there's a probability. As I said, you could be hit by a meteor or simply a bus when you walk down any street. Yet will you never go outside anymore? No. Because the risk of it happening is very low, and the reward of playing football with your friends is higher.

Investing is the same. Ask yourself in which kind of world would we need to be for China to confiscate your Alibaba’s shares? China’s ruler are very pragmatic. But there's risks investing there. But when the potential rewards are higher than the risks, it's worth considering - which it is in Alibaba's case.

Competition PDD & JD. As I said earlier, there are lots of companies in the retail e-commerce and a few have the same pricing advantage than Alibaba.

We saw that the e-commerce market was a very huge cake and Alibaba gets most of it at least in Asia but they'll never get it all and will be targeted by tons of competitive companies. This is true for every business and also is a reason why Alibaba is so aggressively investing in its other business.

Books & accounting. There's a saying in China that companies have three books. One for the government, one for the public and the real one. Don't think this is a myth, it isn't. This is to illustrate the difference between cultures because what we would consider fraud and send people to jail for, the Chinese consider it normal.

We cannot apply western behaviors and logic to a thousand years old culture on the other side of the world. We play different games and if we want to play theirs, we need to learn their rules and not force ours on them.

Some don't want to play another game and that's entirely fine. That might be the only rationnal reason not to invest in China, at least the only properly argumented one I heard, and I entirely respect it.

[Thesis]

We have seen almost everything there is to see about Alibaba. You know the company, its business, finances and risks. Time to turn ourselves to my investment thesis which is pretty simple.

Undervalued stock. The company has a FCF margin above 15% and generated more than $3B last quarter. It bought back $12B of its own shares during FY-23 - reduced the count by 5% - and still has a $25B program until March 2027. It is three years later but this amount at today's price would buy back 13% of the company's capitalization - it's huge.

As if it wasn't enough, Alibaba's tradding at its lowest multiples since years.

Amazon (a perfect comparison point) is trading at a P/S, PER & P/FCF of respectively x2.8, x50 & x41.2. Use any of those multiples on Alibaba and you'd have a share price high above $150 - although Amazon's growth is a bit stronger (really not much) so we'd need to take that into account. Alibaba is still growing high single digits and growth is accelerating over the last quarters as the company's investments are finally paying off.

So why is there such a big difference in the multiples? Simple: China.

Western investors are scared to put their money in a Chinese stock or globally in the Chinese market for very different reasons but the most obvious being the fear of the political regime, the actual geopolitical tensions, and the economic conditions which make many hold their assets closer to home.

All very good reasons but once again, behind every risk there is a probability & an opportunity. Thinking about the risks alone would make you stay in bed all day long.

Reach & Asia growth. But this isn't only an undervalued play, there's more to it. Alibaba is focused on retail. What matters is where the company is & where the products are and the answer is: China.

A retail company close to the most populated countries of the world. But having people around you isn't enough, you need those people to buy things and to do so, they need to be able to, they need a strong purchasing power.

It is obvious that Chinese purchasing power has skyrocketed over the last few years but this is also true for countries like Singapore (or Malaysia as you see fit), Korea, India, Vietnam, Dubai, etc... There's still lots of work to do but those countries are the future, they are the ones where purchasing power is growing the fastest and they are the ones who will, in the next years, buy everything online.

[Opportunity]

I will change my way of doing for Alibaba because the investment thesis is different, it's not at all based on its market share and growth. It's based on trust in China which leads to multiples & the company's ability to grow and turn its branches profitable.

It's impossible to model anything for the first case as trust will come back with time. And we could do some projections on the second as most of their branches should turn profitable in the next few years, very probably before 2026/2027 and when this happens, EPS will rocket.

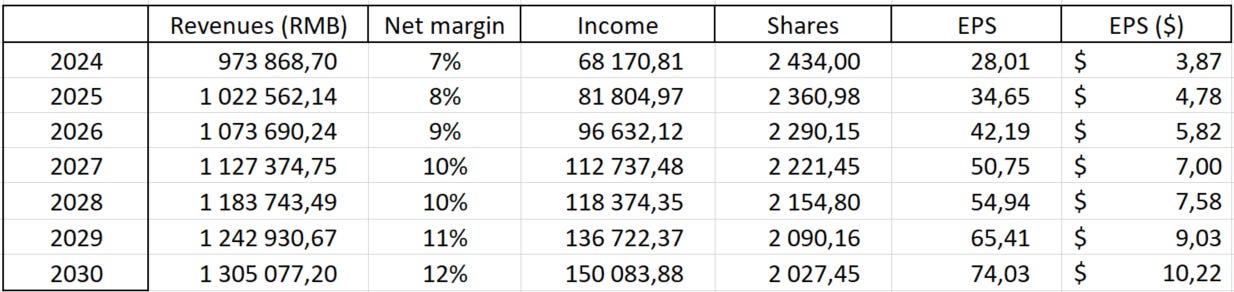

This is a pretty simple view on what Alibaba would become with a 5% CAGR, increasing net margins while shares outstanding decrease 3% per year - not hard to do with such massive buyback programs. Besides the net margins growth, assumptions are bearish.

Now it's all a matter of multiples and trust from investors in China - or greed. It's all about how long they will stand on their hands and not press the buy button while such business are growing.

As a reminder, Amazon is actually trading with P/S & PER respectively at x2.8 & x50. The table reviews different cases.

Keep in mind that those numbers only come with a 5% CAGR, which is pretty bearish considering their branches' actual quaterly growth, and only a 3% reduction on their shares - again, conservative.

This is the only thing to understand with Alibaba: It's all about multiples, and multiples come with trust. And there are no doubts that the company is highly undervalued.

[Conclusion]

This is my investment case of Alibaba. Investing in Chinese stocks has risks but every risk should have its probability attached and to my opinion, the risk of anything serious happening is pretty low after all, and the potential rewards are really, really strong as you saw with my very simplistic assumptions.

I'd still understand that many don't want to invest in China heavily. But I hardly see how anyone could consider it dumb to have a small portion of its portfolio dedicated to it with such a potential - as I really believe the thesis makes sense between Alibaba’s business the families’ purchase power growth in those regions.

It's all about balance.

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!