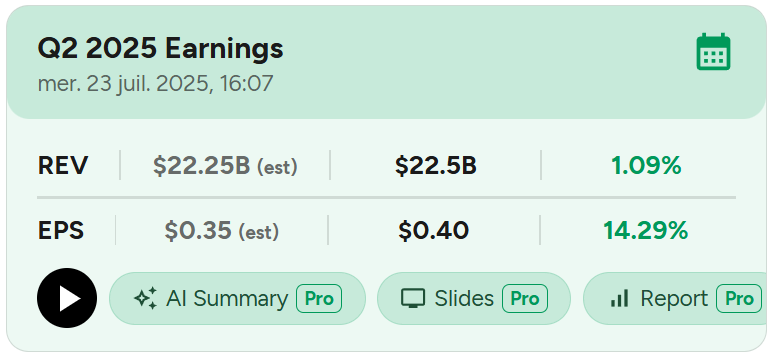

Tesla Q2-25 | Earning & Call

It's a very long & dark tunnel.

Everything you need to understand Tesla’s bull thesis is here.

Business.

The company has clear problems. More than just one at the moment…

EV Demand.

Let’s start here as both revenues & deliveries are simply bad. The question remains on why; is it a brand demand issue or a purchasing power issue?

If you listen to Elon, it is the second.

[…] the desire to buy the car is very high. Just people don't have enough money in their bank account to buy it, literally, that is the issue, not a lack of desire, but a lack of ability.

It is true that the West is still struggling with high rates in some regions - notably the U.S., but Europe has been decreasing them regularly, Canada as well, & demand has not picked up in those regions.

We can see a comparable trend in China where financial conditions are much looser.

Revenues from China include more than just EVs, but those are the biggest proportion of revenues, so it is representative enough of Tesla’s demand in the region - and it is not really bullish.

Tesla EVs are now available in India since a few weeks, which is not a small market, and could generate lots of demand. Let’s see how the region grows.

Every car manufacturer is struggling lately, so there is certainly a lack of demand due to the actual financial conditions. But we can’t blame it all on macro anymore as we start to see signs of lower demand for the brand itself, even in China.

That being said, the Model Y refresh is still new & generated a sequential growth in demand with better economics, rising revenues & operating margins sequentially.

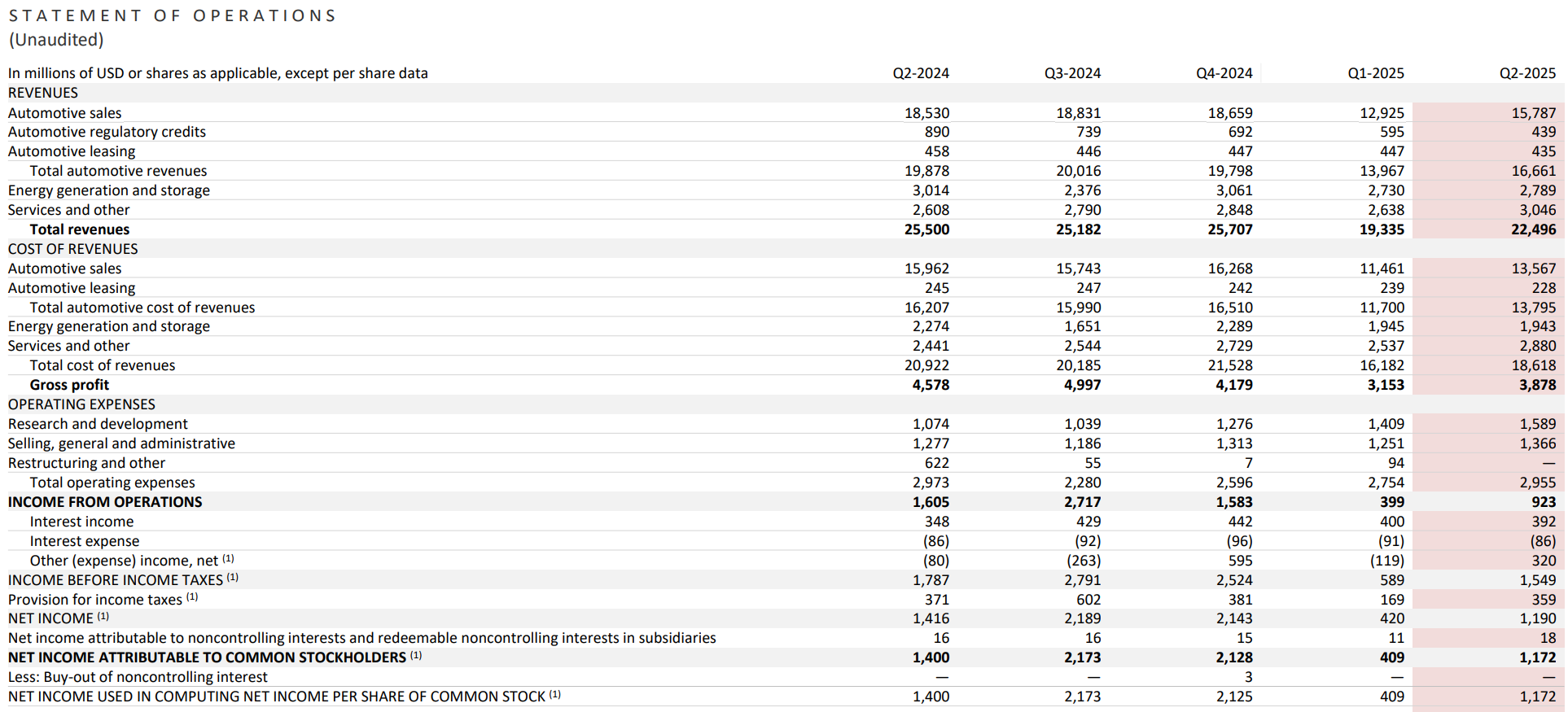

We've started seeing on the automotive revenue front, despite reduction in regulatory credit revenue, the total automotive revenue increased by 19% sequentially, even though total deliveries only improved 14%. This was primarily due to improved ASPs because of the new Model Y.

Probably the only good piece of data I could find on this report.

Energy Branch.

To make it even worse, even the energy branch is struggling while being the biggest bull argument for the company short term.

Growth is flat sequentially in both GWh deployed and revenues and is declining YoY. Management always said that deployments will vary depending on lots of factors as Megapacks require lots of organization, so maybe we should not sound the alarm already, but we’ve been flat-ish for a year now.

Overall, we are forecasting a very strong second half of the year as we increase deployments […] Note that the overall deployments will continue to vary QoQ.

Management remains bullish, but we’d need data to feel the same.

Big Beautiful Bill & Macro.

It’s no secret that Trump’s latest policies won’t go in favor of renewable solutions as they will remove some subsidies, reduce others while Tesla’s entire business revolves around clean energy sources, hence hurting all of their branches - as their products are going to be more expensive for end users.

The One Big Bill has a lot of changes that would affect our business in the near term. The first among those changes is the repeal of the IRA EV credit of $7,500 by the end of this quarte […] This, in turn, will have an impact on the new sales of regulatory credits to other OEMs and, in turn, will lead to lower revenue.

And this comes during a trade war which impacts the entire world.

Sequentially, the cost of tariffs increased around $300 million with approximately 2/3 of that impact in automotive and rest in energy. However, given the latency in manufacturing and sales, the full impact will come through in the following quarters, and so costs will increase in the near term. While we are doing our best to manage these impacts, we are in an unpredictable environment on the tariff front. The margins for the energy generation and storage businesses improved sequentially, while deployment reduced primarily due to the ramp of power deployments at higher margins. We were able to achieve our highest gross profit for the business yet.

Tariffs did not yet trigger inflation, not because “tariffs are not inflationary” as you can read or hear from the U.S. administration, but because all American companies did front-run most of them & built massive inventories in Q1-25.

Those inventories were bought at a normal price & are still used to manufacture, and managements are probably praying for the trade war to be resolved before they run out and have to buy more. If - when, this happens, prices will have to go up because companies cannot keep prices low with higher-priced material.

For now, inventories are enough to sustain normal prices, but they start to deplete big time. This won’t be true for the entire year if nothing changes in terms of policies, and prices will have to rise.

This will impact Tesla as much as others will the reduction of subsidies will had a bit of strength to the hammer hitting the brand.

Full Self Driving.

I do not think the news shared during this earnings call were really good for FSD, at least from a commercial point of view. From a fundamental one, things have never been better as Tesla released its latest safety report, proving once more FSD’s efficiency.

Keeping in mind that the goal is not to be perfect, but better than humans.

And yet, it seems that many - or not enough, are unaware of the system’s quality or want it, which is surprising to me as it seems valuable not to drive - management compares it to a personal chauffeur for $3.33 per day.

The vast majority of people don't know it exists. And it's still like half of Tesla owners who could use it haven't tried it even once. They don't actually. And obviously, this is something we want to educate them on. […] They don't think a car is capable of this.

And so what we are going to do, to Elon's point, like we've been giving people free time to try FSD, but we'll start giving more prompts to say, okay, this particular drive, try FSD.

The latest measures taken by the company improved the demand for FSD.

We've started seeing an uptick in FSD adoption in North America in recent months, which is a very promising trend.

I mentioned it in my opening remarks, since we have launched version 12 of FSD in North America, we've definitely seen a marked improvement in the FSD adoption. And the other thing which we had also done last year is we did bring down the pricing and we've made subscription much more affordable. So we have seen a 25% increase since that time, which is an encouraging trend. But honestly, we've just started the story around explaining the benefits of FSD.

But hearing that half of Tesla owners did not even try it while having a free month is… Really concerning. This software remains Tesla’s bull case & if even EV owners do not try it, trust it, or are not aware of its safety and capacities… There is clearly an issue with the brand’s communication.

Robotaxi & CyberCabs.

The pilot launched in Austin is going pretty well with 7,000 miles drven (11,265km for my fellow non-Americans), which seems a bit weak but once again, it is a pilot without many cars nor many users. Feedbacks are apparently positive without any accidents, despite some imperfections but this isn’t a secret for anyone, not even the bulls.

Deployment will continue with Model Y and others until the CyberCab is ready to take the lead with proper regulations & tests, for a wider service.

A couple of weeks or so. And we're getting the regulatory permission to launch in the Bay Area, Nevada, Arizona, Florida, and a number of other places. So as we get the approvals and we prove out safety, then we will be launching autonomous ride-hailing in most of the country. And I think we'll probably have autonomous ride-hailing in probably half the population of the U.S. by the end of the year. That's at least our goal, subject to regulatory approvals.

I kept the quote, but half of the U.S. population by EOY is clearly a Musk’s prevision. If the service is accessible to the public in some locations by then, many bulls would be happy while management estimates it to be impactful in revenues by EOY26, which seems more reasonable - and even a bit rapid.

Financials.

Without any surprises, everything here is also pretty rough.

Automotive revenues are down 16.2% YoY, because of lower credits revenues but also because of a lower demand despite the refreshed Model Y being available the entire quarter. There is an uptick sequentially, but I wouldn’t see too much into this. We’ve already talked about the energy branch’s YoY decline and flat QoQ while services are slowly growing but far from making any impact in the total.

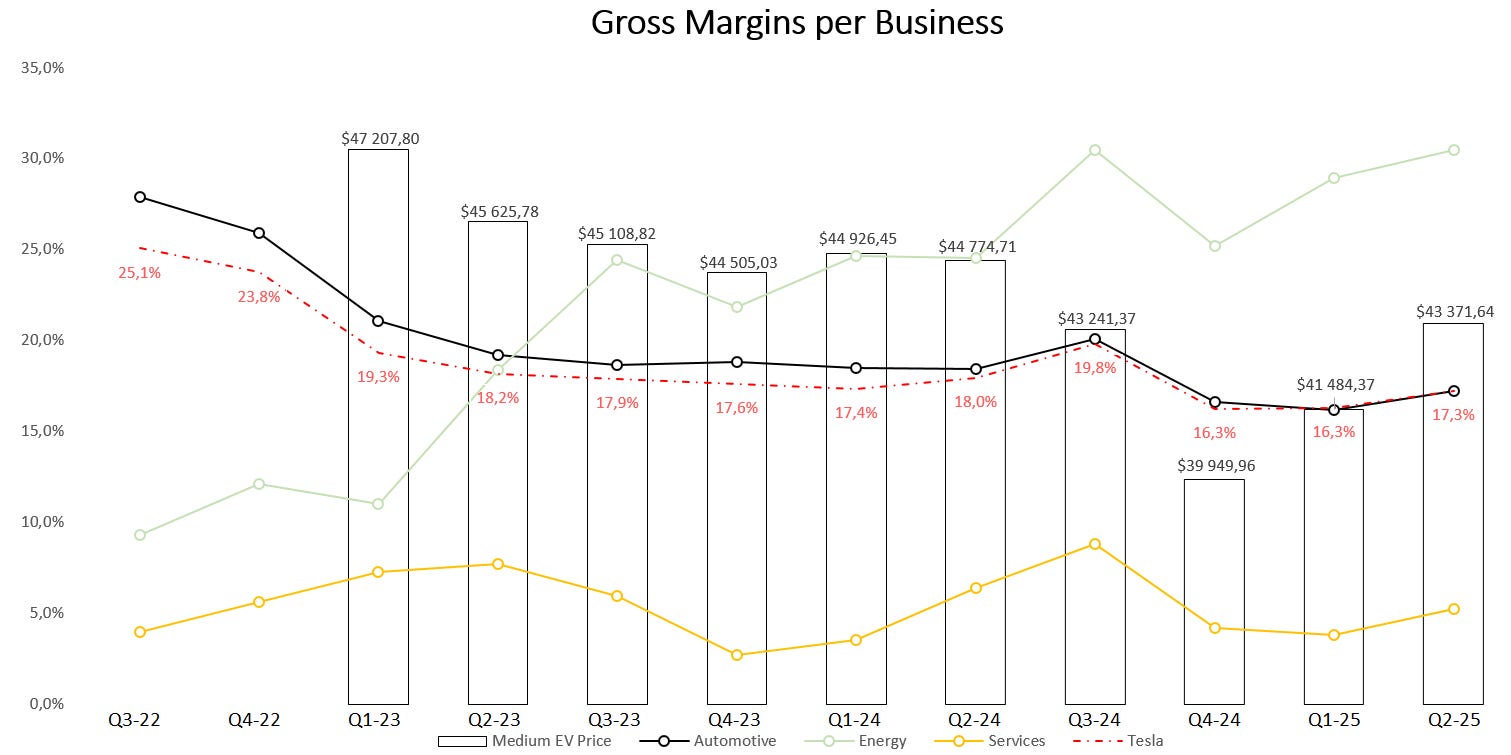

Another potentially good point is that gross margins are growing, which is not too surprising when it comes from the energy or service branch, but is for the EV branch despite lower credits revenues - due to the Model Y pricing as shared above. This brings a small uptick in global margins.

The data remains bad when it comes to cash generation as we’re talking about a 5.2% net margin boosted by Bitcoin unrealized gains - 3.9% otherwise. I personally include treasuries yields as those are cash income, but unrealized P&L on volatile assets should not be included on statements.

Other income grew sequentially, primarily from the mark-to-market adjustment on Bitcoin holdings, which was a $284 million gain in Q2, while being $125 million loss in Q1.

We end the quarter with only $146M of FCF helped by growing SBCs, although Tesla also had massive capital expenditures.

Balance sheet remains very healthy with $29B of net debt as it remains a rule for Tesla and will be used to fuel growth for robotaxi over the next years if necessary.

Investment Execution.

Nothing really bullish on this report. A clear slowdown in demand for the brand’s EVs around the world, a sluggish energy branch, no uptick in FSD adoption - supposed to be the bull case for the company, despite clear safety reports which can make some believe that households have no need for this software - or do not realize its value, are afraid of using it.

The bull case for the company remains the same & Musk knows it better than anyone.

But once you get to autonomy at scale in the second half of next year, certainly by the end of next year, I think I would be surprised if Tesla's economics are not very compelling.

You guys know I am a bull & own the stock. I will accumulate at proper prices because the brand remains the only one with an FSD-like software for households, and if they end up succeeding in household subscriptions and robotaxi, cash will follow big time, with Optimus coming later.

Bears might laugh at me & say that I believe in Santa, that this will never happen. They might be right but I’d rather take my chance than not.

In terms of technicals, we remain in a large range.

The stock can go higher, lower, back on its trendline below $200… I teach you nothing here, everything is possible, I personally intend to accumulate below $300, but won’t make this position massive as it remains based on a narrative with bad data. If data were to get better, I’d increase my accumulation, even at a higher price.

It’s an everything or nothing position based on the potential of what could become a massive ecosystem.

You believe in it. Or you don’t.

Thanks foe the honest feedback on the lackluster quarter, it's disappointing that even the energy brach failed to impress. It's very true that Tesla is a change agent for the future - we only need to convince people to go with it.

The products are great but there is a clear brand issue by now which cannot be ignored anymore... It's not the only thing but it's part of an overall tough situation.

Let's see how things change in the future!