Meta Q2-25 | Earning & Call

Perfection is boring, but this might change.

Everything you need to understand Meta’s bull thesis is here.

Over the last few months, we've begun to see glimpses of our AI systems improving themselves. And the improvement is slow for now, but undeniable

There were a lot of doubts around AI. This quarter and the earnings season at large should put those doubts to rest as companies which invested massively start to show results in the form of revenues & growing efficiency.

Business.

Once again, Meta delivers an amazing quarter, above expectations. Mark continues to look like a kid playing with his billion-dollar toys and Susan is the adult in the room - and doesn’t receive enough praise for her work.

Fundamentals are stronger than ever with a constantly growing user base & time spent on Meta’s apps as the company upgrades its algorithms, which apparently pleases its users.

Advancements in our recommendation systems have improved quality so much that it has led to a 5% increase in time spent on Facebook and 6% on Instagram, just this quarter.

This is part - a big part, of Meta’s success as growing user base & time spent on their apps grows demand for advertising, which is also improving… A pretty virtuous cycle - at least from a corporate point of view.

And those latest improvements are entirely due to AI models.

On advertising, the strong performance this quarter is largely thanks to AI unlocking greater efficiency and gains across our ad system. This quarter, we expanded our new AI-powered recommendation model for ads to new surfaces and improved its performance by using more signals and longer context. It's driven roughly 5% more ad conversions on Instagram and 3% on Facebook.

This is the second part of Meta’s virtuous cycle. A growing user base grows demand from advertisers as they’ll reach a large audience, but Meta’s ads are also getting better thanks to AI, with a constantly growing reach & conversion.

In Q2, the total number of ad impressions served across our services increased 11%, with growth mainly driven by Asia Pacific. Impression growth accelerated across all regions due primarily to engagement tailwinds on both Facebook and Instagram and to a lesser extent, ad load optimizations on Facebook

Which increases both demand from advertisers for Meta’s most perfected advertising tools, and their pricing.

We're also seeing good progress with AI for ad creative with a meaningful percent of our ad revenue now coming from campaigns using one of our generative AI features.

The average price per ad increased 9%, benefiting from increased advertiser demand

The growth rate is slowing down but only because comps become harder as Meta is constantly improving its models for years now - although the uptick in impressions is really impressive at this point.

I have talked about this virtuous cycle regularly now, but it seems like Meta can still make it work even after years of improvements. Curious to know where is the limit. But for now, it’s all about a constantly growing user base, time spent on apps, demand for advertising & efficiency…

Mark’s Avengers.

We already commented on Mark poaching the best engineers from… All around the world, attracting them with massive compute at their disposal and equally massive packages.

I personally like to see this and while people would comment “throwing money is not the right way of doing” I’ll tell them they could be right in many situations. But when Meta’s management throws money, it usually yields results.

To build this future, we've established Meta Superintelligence Labs, which includes our foundations, product and FAIR teams as well as a new lab that is focused on developing the next generation of our models. We are building an elite, talent-dense team Alexandr Wang is leading the overall team, Nat Friedman is leading our AI Products and Applied Research, and Shengjia Zhao is Chief Scientist for the new effort.

The people who are joining us are going to have access to unparalleled compute as we build out several multi-gigawatt clusters.

Time will tell, in the meantime, Mark now has his brainy army meant to build & share superintelligence with Meta’s users.

Hardware.

Some comments on Meta smart glasses & their new partnership with Oakley.

We continue to see strong momentum with our Ray-Ban Meta glasses with sales accelerating. We are also launching new performance AI glasses with the Oakley Meta HSTN, they have longer battery life, higher resolution camera and are designed for sports.

The percent of people using Meta AI is growing, and we are seeing new users AI retention increase too, which is a good sign for that continued use.

The growth of Ray-Ban Meta sales accelerated in Q2, with demand still outstripping supply for the most popular SKUs despite increases to our production earlier this year

Europe Regulatory Headwinds.

The continent continues to be against innovation and has been fighting against Meta for long now, and this battle is apparently not over even after many modifications to their algorithm in the region.

For example, we continue to engage with the European Commission on our Less Personalized Ads offering or LPA, which we introduced in November 2024 and based on feedback from the European Commission in connection with the DMA. As the commission provides further feedback on LPA, we cannot rule out that it may seek to impose further modifications to it that would result in a materially worse user and advertiser experience. This could have a significant negative impact on our European revenue as early as later this quarter.

This could turn to be a big headwind as Europe was the fastest growing region this quarter, and remains Meta’s second biggest quarter.

Financials.

Nothing much to comment here.

Everything is as good as one could expect, revenues are up 21.6% YoY, income 31.1% YoY. Expenses are under control and margins are expanding thanks to AI efficiency & models delivering better results, hence demand.

In terms of cash, Meta generated $8.5B of FCF, has $18.2B of net debt and returned $9.8B & $1.3B to shareholders through buybacks & dividends respectively.

As impressive as usual.

Capex, ROI & Compensations.

I’d like to take a section to talk about CapEx & compensations as both will affect Meta from now on, as CapEx expansion started a bit more than a year ago and continued, accelerated even with a target up to $66B this year & even higher next year.

So we expect to ramp our investments significantly in 2026 to support that work.

Our Prometheus cluster is coming online next year, and we think it's going to be the world's first gigawatt-plus cluster. We're also building out Hyperion, which will be able to scale up to 5 gigawatts over several years, and we have multiple more titan clusters in development as well. We are making all these investments because we have conviction that superintelligence is going to improve every aspect of what we do.

Gentle reminder that the market was selling the stock below $450 a year ago due to this kind of comment. Things changed - my view on it didn’t though.

On CapEx first, the “problem” with investing in infrastructure is that it reflects on the company’s statements as they need to take depreciation in consideration, and as Meta invested massively in it… Depreciation will accelerate & impact margins.

This is also true with the massive comps they plan to pay Mark’s Avengers, which will be included in the company’s G&A and also impact margins. Susan says it herself.

On the second part of your question, we've said in the past that our primary focus from a profitability perspective is driving consolidated operating profit growth over time. And it won't be linear. In some years, we'll deliver above-average profit growth. And in years where we're making big investments, I think we will see that impact the amount of operating profit growth that we can deliver. And at the moment, we see a lot of attractive investment opportunities that we believe are going to set us up to deliver compelling profit growth in the coming years for all of our investors.

Both will be added back into the cash flow statement but depending on how we look at a company’s results, we could see declining margins & imagine that it is a bad sign, change the market’s perception of a quarter & of Meta.

I am part of those who have always been in favor of those investments as I believe Meta has one of the best - if not the best, management in the world & has proven itself capable of returning value from its investments, but some disagree - not with the fact as data speaks for itself, but with the decision.

Let’s see what they do during the next years, but those factors could lead to a down trend, not due to Meta’s fundamentals, but to the market’s perception of the data.

Investment Execution.

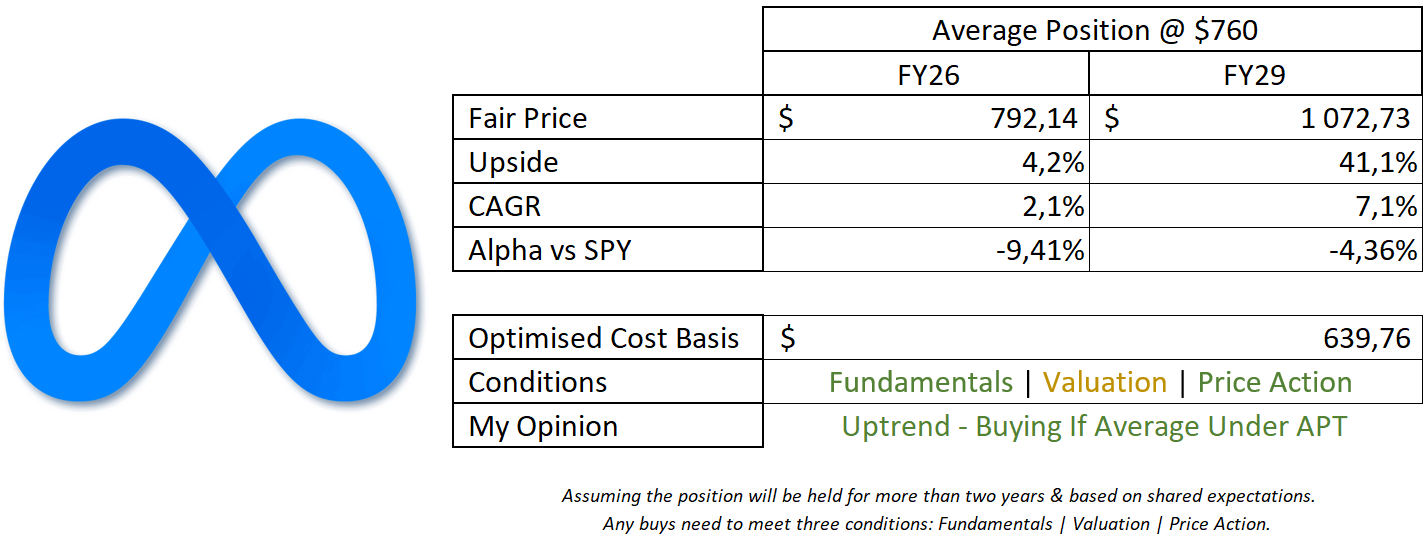

Another elite quarter from Meta, without much more to comment on. I would remain cautious on the market’s perception & actual valuation, but I can see no reasons to worry fundamentally for the future of the company.

This model assumes an 18% & 13% CAGR growth until FY26 & FY29 respectively, 40% net margins, 1.5% returned to shareholders & P/S & P/E at 26x & 7.5x respectively.

The stock is surely a bit expensive right now, reaching the top line of its P/S five-year average & starts to show some bearish divergence with its price action after breaking its ATH on this report.

I personally believe this is a better region to trim than anything else but this is only my personal bias. In terms of accumulation, the breakout would give a perfect region if that’s what you are looking for.

Meta is an elite company.

If you want a bit more insight on how I trim my stocks, you’ll find a detailed explanation here.