MercadoLibre Q2-25 | Earning & Call

Currency mix is a b*tch.

15% discount on FiscalAI subscriptions through my link. FiscalAI is the tool used for KPIs on all my write-ups; powerful, valuable data & great UX.

https://fiscal.ai/?via=wealthyreadings

Everything you need to understand MercadoLibre’s bull thesis is here.

As I shared extensively on my investment thesis, the macro conditions locally are very important for Meli’s bull thesis & the data is pretty good at the moment thanks to a falling dollar & lowered inflation in Argentina, in between other components.

Argentina is growing particularly well, I would say, as a result of both macro conditions and team execution.

Although ironically, the dollar is partially the cause of weaker results than expectations.

Business.

I would like to start by highlighting the professionalism & quality of this earning call. I read a lot of them each quarters & years, but Meli’s management is really something else with clear & honest answers. No bullshit. Important to start here as it’s not the case in every company.

Brief overview of Meli’s quarter, which is really healthy in all its segments.

We might start by talking about currency headwinds, which I talked about many times already but are important for companies which declare earnings in dollars but sell in other currencies, which gives strong headwinds when the currencies it sells in lose buying power against the dollar.

A normal dynamic for companies involved in different geographies & currencies, there is nothing to be done about it, some quarters will yield positive FX, others negative, although when business is done in LATAM there are more negatives than positives due to how currencies are managed - also covered in the investment thesis.

E-commerce.

The take away from this quarter is really easy: more users, more spending, more units shipped & rising consumption.

A constant 25% YoY growth in unique active buyers, a 5% YoY growth in amount of items per unique buyer and a 23% growth in GMV, once again constant over the last quarters.

And this strength is true in all geographies with a constant growth in Mexico & Brazil and an accelerating one in other regions, while Argentina’s growth is still massive but the smallest of the three region - on par with Mexico.

The big subject of this quarter was the reduction on shipment fees in Brazil, which has always been Meli’s strategy to onboard & retain users on its platform - a proven strategy all around the world.

We would not be a $50-plus billion GMV company today per year if it were not because of building our logistics infrastructure and launching our free shipping program back in 2017.

To all the questions asking for short term results, the answer was that they will be coming, as they always have under such circumstances.

So it's a bit early, but we definitely expect the trend that we see in traffic increases, conversion rate increasing, more engagement, more frequency to continue in the future. And with that, we expect to see orders going up, order sizes going up and so on, right?

On Argentina, as shared above, as the conditions in the region improve economically and spending is growing - massively.

Argentina had another exceptional quarter in Q2'25. Unique buyer growth exceeded 30% YoY for the second consecutive quarter – underscoring the attractiveness of our value proposition versus physical retail in Argentina as the economy stabilizes, confidence returns and consumption strengthens.

In Mexico, steady developments of logistics continue to yield good results.

Some comments on advertising.

In Q2, we launched our integration with Google Manager, an important milestone in positioning Mercado Ads as a key strategic partner for brand-focused advertisers.

Argentina is growing particularly well, I would say, as a result of both macro conditions and team execution. So lower inflation, more stocks on the hands of sellers and so on is kind of giving them the space and the oxygen to be able to invest as to promote sales.

FinTech.

Once again, really healthy with the same kind of trend highlighting a growing user base - a constant 30% YoY growth, and consumption of the services.

Monthly active users of Mercado Pago reached 68 million, reflecting rapid user growth and increasing engagement across our ecosystem. Assets under management more than doubled year-on-year once again. Our credit portfolio surpassed $9.3 billion, growing by 91% year-on-year.

In other words: engagement is strengthening. This is the context in which we launched bold marketing campaigns with the objective of significantly expanding Mercado Pago's reach beyond its current 68mn MAUs.

I wish I could comment more but… Sometimes great data allows me to rest my fingers a little bit.

Financials.

As one could guess, pretty strong overall although we have to touch to some key data.

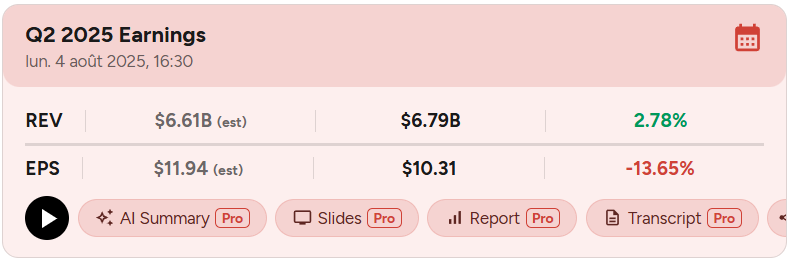

Revenues grew 32% H1-25 which is excellent, on expectations, and gross margins are stable around 46%. The bigger problems, at least what did not please the market at open - before it corrected its mistake as we’ll see below, were the net margins which came below 8% compared to 10% a year ago, resulting in an EPS miss.

There are reasons for this, the first one due to normal financial business with a bigger provision for doubtful accounts than expected, the second from higher FX headwinds as shared above, and lastly due to marketing campaigns.

So I would think it's a combination of both ongoing investments in acquiring users and downloads, but also a couple of one-off campaigns, in particular in Mercado Pago and the lower free shipping threshold that we did in Brazil this quarter.

The EPS miss is more due to an accumulation of timing issues than a structural issue, so we should not worry about it.

Investment Execution.

The conclusion will be as short as this report. Every branch is growing well & healthily. The only possible bad data of this report comes from this accumulation of bad timings.

In term of valuation, we are around my buying target.

This model assumes a 25% and 20% CAGR growth until FY26 and FY29, respectively, 9% net margins, no dilution, and P/S & P/E at respectively 5.5x & 40x.

Those assumptions are fair, but not too conservative, with a 5% margin of safety - like all my assumptions. So we clearly are around a buying price for a long term position, it only depends on how conservative you’d like to be.

In term of price action, the stock was supposed to gap down at open but the market quickly realized its mistake - sadly as I clearly would have bought in. The stock still has a tendency to bounce on its 50EMA a few times per year, so I’ll remain patient, hoping this happens soon enough.

We’re still bouncing on a massive support so it might take some time, except if we finally have that market breather I’ve been waiting for…

Shareholders are certainly holding happily.