Hims&Hers Q1-25 | Earning & Call

The bear case is melting

If you do not know about Hims & Hers, everything you need is here.

The bull case is rapid: Attract customers & convert them to personalized plans through different treatment verticals while delivering the best care possible by leveraging data, focusing on long term life quality improvements.

“Over time, we aim to create a curated healthcare ecosystem bringing together best-in-class solutions anchored by better data, personalized experiences, and trusted clinical support.”

“Netflix transformed the way we consume media through an initial focus on building a broad subscriber base by leveraging convenience and then utilize data and insights to elevate the experience for their subscribers.”

Overview.

Strong.

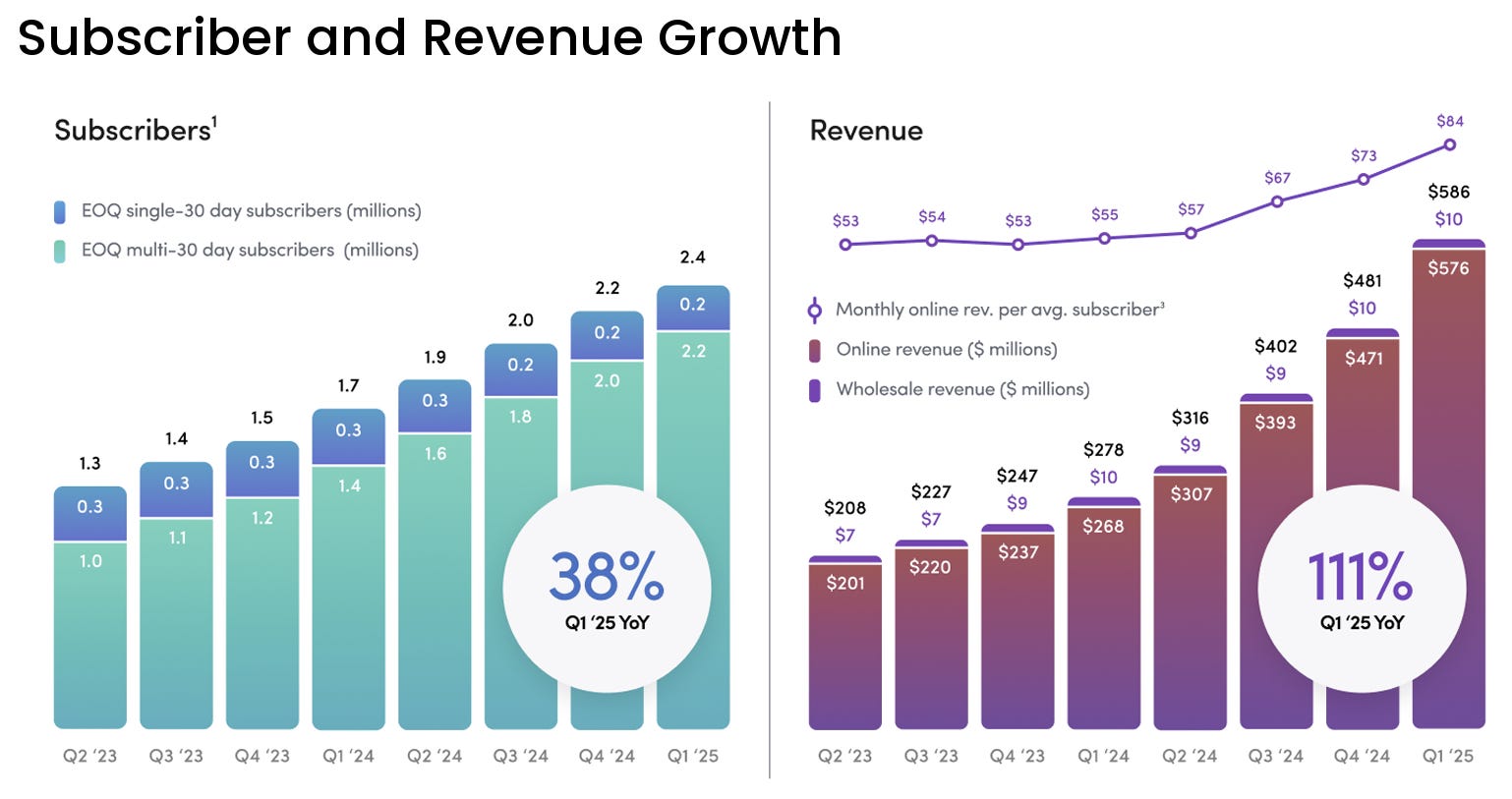

Revenue. $538.87M | $586.01M | +8.75%

EPS. $0.12 | $0.20 | +66.67%

No buybacks | $65M remaining.

Business.

Subscribers.

The subscriber base continues to grow pretty rapidly with a 38% YoY growth to 2.4M patients with massive retention - multi 30-day subs.

Hims is onboarding 200,000 users per quarter & its rentention over the last three quarter has been… Close to 100%. Less before that but still really high.

Don’t get caught on the average revenue per subscriber as portion of it came from the rapid growth of compounded semaglutide - which had a higher pricing than the rest of their products. It’s hard to say how this will evolve now that this product isn’t wildly available anymore, it might stabilize, maybe decline… Again, it isn’t the most important metric. but Hims will scale on volume & not on pricing per client.

On personalization, the bull case, conversion remains strong & is accelerating with 63% of their patients now following a personalized plan.

This is the most important metric to look at & the demand for it is growing through all verticals, not only GLP-1, and the potential remains huge.

“80% of [dermathology] businesses are now with personalized proprietary skews, having driven a 20-point retention gain in just the last couple of years. You see the same kind of things happening across the sexual health business as we really transform that business to 1 with dual action treatments, hyper personalization, daily benefits. The penetration rates of the core categories we're in are still very, very low. I mean, you're talking low single digits given the TAM”

Weight-Loss Branch.

Many comments, starting with the bear case slowly melting.

“year-over-year subscriber and revenue growth outside of GLP-1s were both nearly 30% in the first quarter.”

This is the first time that the market has real confirmation that growth happens, even without compounded semaglutide. We had pointers, but bears remained convinced Hims wouldn’t grow without semaglutide. Not only does their weight loss drugs branch continues to grow, but the rest is growing as fast.

“You've got the Hims & Hers dermatology businesses growing 50% plus year-over-year. Those businesses have really been transformed with personalization where north of 80%.”

On Novo Nordisk’s relations & their new partnership which could give opportunities for Hims to leverage their massive portfolio.

”This collaboration also signals something important, trust from a major pharmaceutical leader, and it sets the blueprint for future partnerships that can expand both our reach and our relevance.”

We talked about it already, with branded GLP-1 now available on the platform. It goes further than just reselling the drug though as Hims’ $599 package includes a complete follow-up for their patients to reach their objectives. There is value added compared to simply purchasing the drug itself.

Hims isn’t just selling things online, they sell an entire personalized service. This is what makes the difference.

Questions were asked on their relations with Novo while continuing to compound semaglutide. I raised the question last week so I am glad to have answers. Hims did have conversations with them on how this would cohabit - and confirmed again that they are strictly following the FDA rules.

“On the personalized semiglutide standpoint, you know, one of the things that we did talk about with NOVO early is just what we believe is appropriate use of personalization and align philosophically with what our providers believe is that clinical necessity. So there is an alignment for what we believe to be blue chip use of that compounding exemption.”

There is an understanding, and probably some rules.

“these are patients that frankly just cannot use commercial doses or a lot of them have actually tried the commercial dose and then have turned off due to the high side effect rate.”

Only proposing personalised solutions to patients who already tried branded dosages & couldn’t keep up with it. This would not eat Novo’s revenues as those would be lost customers either way. Hims confirmed that they were on the same page.

The details are speculation from me. What matters is that there is an understanding between both companies.

I also want to point that the 300% growth on their oral solution is a great number, but it was also launched in Q1-24 so it is compared to no volume at all. We’ll need longer to have a real comparison & idea of the potential of this vertical.

Expansion.

Lots of things coming this year.

Starting with their at-home lab which was announced some months ago and will start to propose its services this year. If you missed the investment case, here’s a diagram on how it will work to provide better data to their clients, more personalization on their treatments hence a better outcome & usage of Hims’ services.

And more coming with low testosterone & menopausal treatments, more later with a potential focus on peptides.

“Building on our success in weight loss, we are launching new offerings in low testosterone and menopause support this year, with longer term opportunities emerging in longevity, sleep, and preventative care as we expand lab testing and peptide capabilities.”

I am not an expert in the subject so I will document myself before commenting.

Management.

Rapid comment on the change of COO - Chief Operating Officer, as Nader Kabbani, who worked 18 years for Amazon, is set to replace Melissa Baird. Bringing more experience on key subjects for Hims’ next steps.

Financials.

Strong, again.

As we’ve seen, revenue grew 111% which is massive. Costs grew faster which reduced the gross margins which is normal - GLP-1 business has lower margin. Now that this portion is restricted, gross margins should expand again. Expenses didn’t grow as fast as revenues - up 70% YoY. With a much higher revenue base, cash generation was much stronger with net income growing 345% YoY.

Quarter ending with $109M of OpCF, $50M of FCF - up 321% YoY, with $25M of SBDs - as usual for growth companies: strong but growth is here so why complain, and a very healthy balance sheet with $232M of net debt. Can’t ask for more.

Surprisingly, Hims did not buy back any shares this quarter while the stock price was clearly depreciated. Buyback is their last priority & they spent a lot lately so this is a potential focus on keeping their balance sheet. Curious still.

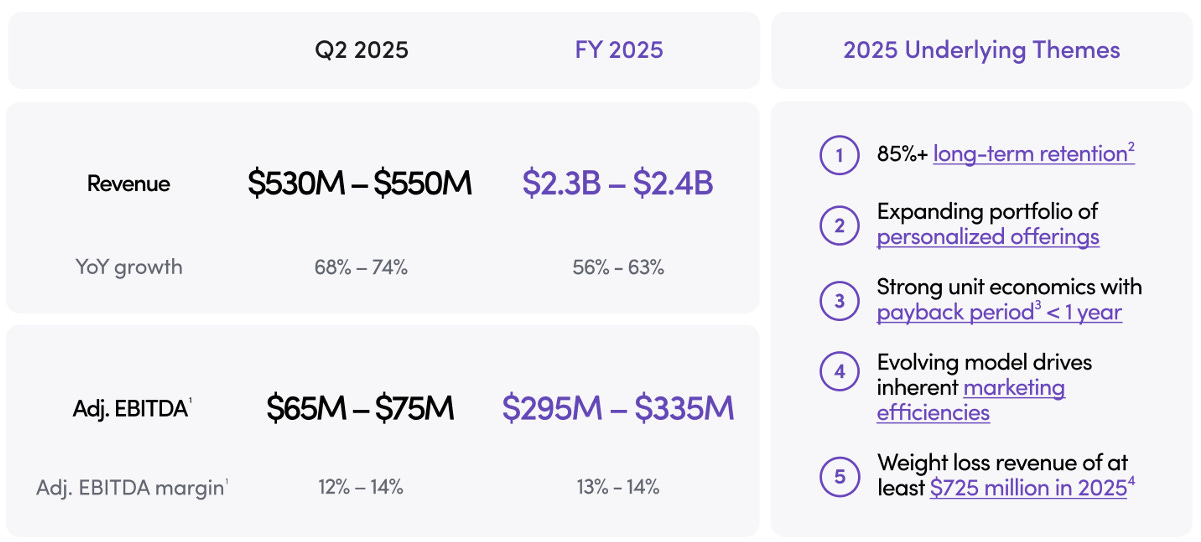

Guidance.

This isn’t helping the bear case.

With compounding GLP-1 ending in April, many expected Hims’ growth to plummet. It should slow down - about 74% YoY hence no more growth acceleration at least for a quarter, but remains massive & proves that semaglutide was not the only source of growth, far from it - as seen above. Yearly guidance is unchanged and many start to believe it now - they doubted they’d do it without GLP-1.

Hims gave a second guidance which I wouldn’t take for granted nor look at too closely as things are really hard to predict so far in time but they seem comfortable planning for $6.5B+ revenues by 2030.

My Take & Valuation.

Quarter was nothing but excellent in my opinion & confirmed the bull case while also decreasing the probabilities of the bear cases - no to small growth without GLP-1 and potential patent infringement from Novo Nordisk. Both of those now have a very low probability of happening which means the narratives will change & might turn bullish, with a lower focus on their GLP-1 business anymore - finally.

We’ll need a bit more time to see exactly how the weight-loss branch will behave but trajectory seems good while other branches are growing rapidly - confirmed by strong attraction & conversion despite not selling personalized GLP-1 anymore. Plus lots of new verticals to be added in the next year(s)…

What’s not to like?

Valuation became much more interesting as Hims reduced uncertainties. What is cool with great companies is that they often get cheaper - or at least not more expensive, while stock continues to climb.

This model assumes a 40% & 25% CAGR growth until FY26 & FY29 respectively, 9% of net margins, no returns to shareholders & multiples equal to its 3Y P/S average at x5.

I would personally consider those assumptions conservative, both in terms of growth & multiples but being conservative is not bad when investing, especially in growth stocks.

To go a bit further with Hims’ long-term guidance - which I would not use as a base case. A P/S of 5x on $6.5B means $32.5B of capitalization, or $145 per share by 2030 assuming no dilution. Just sharing the numbers.

Rapid words on price action, which I usually do not comment here. Hims was one of the most shorted stocks these last months and yes, this quarter is excellent but price action could be due to short covering - shorts buying back their shares which applies a buying pressure on the market, as the thesis of lower growth due to GLP-1 shortage or lawsuits from Novo decrease in probabilities.

In conclusion, the quarter is excellent, the bull case continues to play out while the bear cases probabilities are reduced one by one. If you follow me for some time you know I have a position sub $20 since long now, and I sure intend to increase it but I will remain patient. This pump was strong & maybe not very healthy as detailed above. Don’t chase green days, wait for the red ones to buy.

I have no reasons to sell any shares though, the only question is when to buy more.

Thanks for the coverage!

Pleasure!