Grab Q2-25 | Earning & Call

Following Uber's playbook.

If you guys are interested, you’ll have 15% discount on FiscalAI subscriptions through my referral link. FiscalAI is the tool used for KPIs on all my write-ups, really powerful, valuable data & great UX.

https://fiscal.ai/?via=wealthyreadings

Everything you need to understand Grab’s bull thesis is here.

Business.

Grab is a complex business to detail as it is based on a flywheel, converting users and merchants across different verticals - deliveries, financials, mobility, advertising…

One merchant can be here to sell its products, contract a loan, and advertise on the apps. And a customer can consume with both mobility and delivery, scroll ads, but also contract loans or use Grab fintech apps as its payment system.

So, it goes without saying that user and merchant acquisition are immensely valuable to Grab, probably more than other companies as each acquisition can be leveraged two, three, or four times.

And of course, in our case, because we are multi-vertical as an ecosystem, the benefits of having new users come in extends to the broader Grab ecosystem as then we can cross-sell into Deliveries and Financial Services.

FiscalAI was not updated yet as they need the 10Q which isn’t available yet, but Grab now has 46.2M monthly transacting users, a really healthy acquisition & retention.

Grab also achieved double-digit growth in GMV, keeping their crown as the biggest player in their field in SEA.

But I think, overall, we are about 3x -- 3.5x larger than our next largest competitor in the region. And that means that our scale economies are quite considerable. And that's why we've been reinvesting in AI and other capabilities, which mean that our efficiencies and the savings we can pass on to consumers are much higher than those of smaller competitors.

This is the Uber playbook - which is not surprising as they have a seat on Grab’s board and own around 13% of the company: strangle competition. Expand faster, cheaper & never slow down on aggressiveness until you own enough market share to finally optimize your operations and turn the cash machine on.

Nothing says that it’ll work as well for Grab as it did for Uber. But they are following the same playbook and have positive data so far, while also having this flywheel opportunity which Uber didn’t have.

Mobility & Delivery.

Both are growing healthily, especially mobility with MTUs growing 16% while number of transactions grew 23%, indicating a growing usage of the service from active users plus a strong acquisition. Double wins.

Once again, FiscalAI was not updated, but it shows the dynamic. Q2-25 delivery and mobility GMV were respectively $3.47B and $1.88B, up 22% and 19% YoY for a total GMV of $5.35B, up 21% YoY.

Healthy and encouraging, especially as management expects this growth to continue.

We expect to sustain this growth momentum to accelerate on-demand GMV growth rates relative to 2024.

With growth also coming from its subscription plans, confirming a strong demand & customer satisfaction for their services.

In addition, as you well know, we've got GrabUnlimited, which is now the largest paid loyalty program in Southeast Asia, driving almost 5x higher spend and 3x higher order frequency for its members. And we've reached new record highs in paid subscriber count there.

Grab is investing in AI for different verticals of its business, including physical AI with autonomous vehicles to optimize and scale both deliveries & mobility.

At the moment -- earlier this month, we announced A2Z, partnership with a Korean full- stack AV manufacturer. Now that culminated in the announcement of the first autonomous electric shuttle bus in Singapore. Now in Philippines, we are working with regulators closely and property developer Megaworld to launch a pilot study on drone-powered commercial delivery. you can expect to hear new partnerships with more global AI and driverless AV partners.

Asia is moving pretty fast on this kind of subject - see China, for example, on par with the U.S. for AV services, so I wouldn’t be surprised to see it in Grab’s geographies soon - except countries like Vietnam where the traffic is simply impossible for AVs.

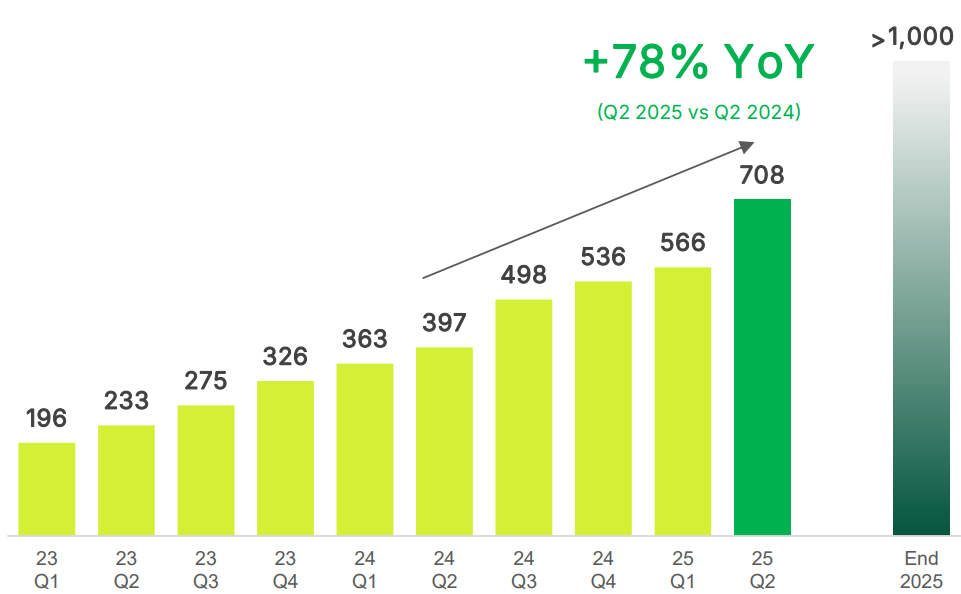

AI will also be leveraged in advertising, a rapidly growing vertical for Grab with large potential, part of the company’s flywheel with a run rate of $236M today, growing 45% YoY with pretty low penetration.

We're still at less than 50% penetration of our merchant base in terms of those that have tried us. So there's still upside there in terms of expanding the penetration of our merchant base. And because their return on advertising sales is averaging 8x, we know that it's a great product for them, and it can help them grow

This is the same story as Meta and another reason why user base is so important for Grab: the more users, the more demand for advertising, and as Grab leverages AI to improve its ads, the more expensive they get & higher margins, yielding better returns, attracting more advertisers, more users, etc...

We start to see this virtuous cycle with Grab.

Fintech & Loans.

Not much to comment here except to say that the vertical is growing very fast thanks to very different products targeting all kinds of users and merchants -BNPL, personal lending, SME supply chain financing, etc.

So we've said that by the end of the year, we'll hit $1 billion. We're at about $700 million in the end of quarter

I have no data to support this, but my assumption remains that the flywheel is really working as growth follows user acquisition & manamgent confirmed its focuse on its own user base - which makes it even more interesting for merchants to be part of Grab ecosystem entirely, accelerating the platform’s network effect.

We continued to focus on lending to our ecosystem partners through GrabFi and our Digibanks.

Financials.

Financials are pretty stable for a growth company.

A 23% YoY revenue growth, completely organic, with its fourth quarter of profitability in a row and stable margins, without focusing on profitability as the main objective remains user acquisition & to strangle competition - the Uber playbook.

In terms of cash, a small reminder that the company raised $1.5B at zero coupons a few weeks ago - which once again shows pretty strong confidence from the market. They do not have any plans yet for their $5.4B of net debt, but we can be sure those will be invested to generate organic growth through acquisition or improvements.

Guidance.

Management left its outlook unchanged.

Investment Execution.

This is a good quarter in terms of continuation for Grab; it shows that the thesis holds and that the company is capable of attracting and retaining users while leveraging its flywheel, converting both merchants & consumers to their financial services.

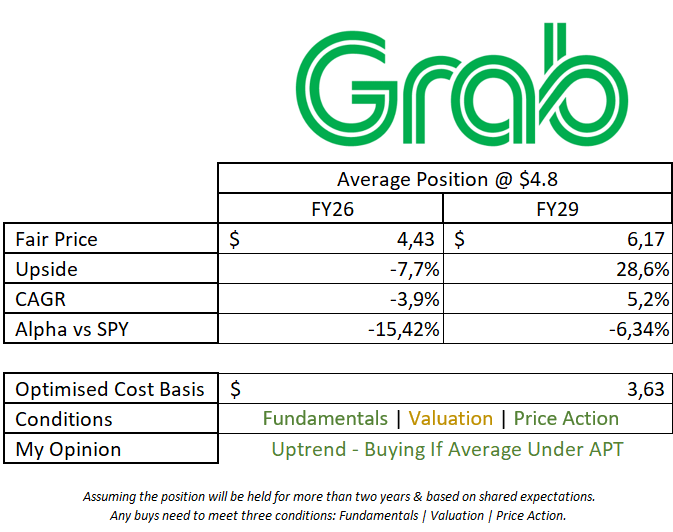

In terms of valuation, we are still above target for a perfect position, but let’s keep in mind that these growth stocks always have a premium due to potential; they’ll rarely reach my targets as I tend to be conservative & they don’t include emotional premiums.

This model assumes a 20% and 17% CAGR growth until FY26 and FY29, respectively, 3.5% net margins, 3% of dilution, and P/S at 5x.

To illustrate my point, Grab fell to $3.4 on the April “crash” while most stocks I follow went largely below my buying prices. It will be very hard to buy at $3.6 as long as we stay in a bull run, except seizing the perfect opportunity during a volatility spike.

For now, the stock did break out, and I took a speculative position on the retest, but it ended up reintegrating the downtrend following earnings & the macro new at the end of the week.

This isn’t the best, and we won’t have the explosive trend we could have expected, but we are now reaching the 50EMA, which, once again, is an important bull region to hold on bullish trends. If it holds, I won’t close the position.

As for a long-term position, it is up to each of you to add the emotional premium you feel is fair to the fundamentals and make your plan according to it; be sure that you can hold the position with averages at those prices.

For now, I personally have better names to buy on my watchlist, but I could consider it if we continue to stabilize around 44.5 or so. The trendline is healthy, fundamentals are improving and potential is massive, especially in one of the fastest-growing regions in terms of buying power.

Grab is a great company to diversify ourselves from the U.S. consumer, which I believe is important to do for the medium term.