Google Q2-25 | Earning & Call

Another room, still no disruption in sight...

Everything you need to understand Google’s bull thesis is here.

Business.

Search & The Invisible Disruption.

I’ve shared this many times already & I’ll share it again: there is no disruption when it comes to Google Search, there is simply a shift from one usage to another one, from Google Search to Gemini-powered services.

And this quarter kind of confirms the thesis.

The advertising business is growing really well both from Search & YouTube. Any data showing lower usage of search is because those reports do not include Gemini powered models, which are included in Google Search revenues.

Search revenues sequential growth this quarter is stronger than both previous years, despite starting from a higher value and competing with other LLMs. Even better, Gemini services are more & more used, for search, shopping but also globally.

“We also saw strong growth in the use of multimodal search, particularly the combination of lens or Circle to Search together with AI overviews.”

“Google Lens search is one of the fastest-growing query types on Search and grew 70% since this time last year. Majority of lens searches are incremental, and we're seeing healthy growth for shopping queries using lens.”

“We are seeing significant demand for our comprehensive AI product portfolio. The growth in usage has been incredible. The Gemini app now has more than 450 million monthly active users, and we continue to see strong growth in engagement with daily requests growing over 50% from Q1. In June alone, over 50 million people used AI-powered meeting notes in Google Meet. And powered by Veo 3, our new short video product in Workspace called Google Vids reached nearly 1 million monthly active users.”

“Overall queries and commercial queries on Search continue to grow YoY. And our new AI experiences significantly contributed to this increase in usage. We are also seeing that our AI features cause users to search more as they learn that search can meet more of their needs. […] We know how popular AI Overviews are because they are now driving over 10% more queries globally for the types of queries that show them, and this growth continues to increase over time.”

This is what we want to pay attention to, that the shift is happening within Google’s ecosystem and not leaving Google to the benefit of another provider - that could happen. So far, the only thing data shows is that this shift is happening organically within the ecosystem which offers incredible tools leading to consumption.

Another problematic issue could be the potential need to change business model as advertising on LLMs is not organic and could lead to less demand from advertisers, but once again, this is not what we see.

As shared above, those new AI features generate more engagement & drive to more consumption, through different but as efficient use cases. That’s why demand from advertisers continues to pour, because of a growing efficiency.

“Over 2 million advertisers now use Google's AI powered asset generation tools to run ads, a 50% increase on this time last year.”

“Last quarter, we introduced AI Max and Search, a new suite of AI-powered features in existing search campaigns. Advertisers that activate AI Max and Search campaigns typically see 14% more conversions.”

“One, the number of deals over $250 million, doubling year-over-year; two, in the first half of 2025, we signed the same number of deals over $1 billion that we did in all of 2024. Three, the number of new GCP customers increased by nearly 28% quarter-over-quarter; four, more than 85,000 enterprises, including LVMH, Salesforce and Singapore's DBS Bank now build with Gemini, driving a 35x growth in Gemini usage year-over-year.”

Nothing new here as we’ve been saying the same for a few quarters now: AI is driving a clear growth in targeting efficiency & ad quality, which makes consumption rise and grows the value of advertising on the biggest ecosystems, and Google’s is clearly not losing users thanks to constant release of useful AI services.

YouTube, King of Video Consumption.

The platform continues its wonders, keeping its crown as the most-watched platform based on Nielsen reports with a 12.8% total TV viewing share.

We continue to see strong performance in YouTube as well as subscriptions, reflecting great momentum across these high-growth businesses. In the U.S., shorts now earn as much revenue per watch hour as traditional in-stream on YouTube.

A generation that grew up with YouTube on their devices is now increasingly watching their favorite creators and content on their televisions.

Not much more to say…

Google Cloud.

The service used to be late on its competition, but not anymore; it even seems to be catching up fast as the branch now has a run rate of $50B per year… Massive.

Google Cloud backlog increased 18% sequentially in Q2 and 38% year-over-year, reaching $106 billion at the end of the quarter.

And revenues continue to accelerate while operating margin is expanding, pushing from 11.3% to 20% in a year. Google Cloud is an accelerating business generating more cash per revenue…

Again: Massive.

Waymo.

Nothing specific was shared on Waymo despite new records in terms of miles driven and range covering as they expanded them in almost all cities the service is present, but as other bet financials are not better, I assume that the service continues to scale but is not ready to participate in the company’s financials.

Still good news.

Financials.

As you can expect, financials are nothing short of perfect.

Revenues continue to grow healthily, above the double digits since the company went deep into AI & more importantly, margins continue to expand with a really clear trend when seen over the last years, especially for net margins as Google grows the efficiency of all of its business - as shared earlier with its Cloud branch.

Everything is perfect.

Although those who pay close attention to the chart will see a strong decline with the yellow bar, which represents free cash flow. The reason is simple: Google is growing its CapEx expenses, hence less cash generation and a bigger difference than usual between income & FCF.

Google focuses on capitalizing on AI & this requires massive investments. And this won’t slow down as Google is now planning to spend $85B FY26, up from $75B.

Looking out to 2026, we expect a further increase in CapEx due to the demand we're seeing from customers as well as growth opportunities across the company.

This spending is meant to answer a demand, not just to throw money, even though many continue to say that dividends & buybacks would be a better use of capital. Yet, Google has a ROIC above 25% each quarter over the last 5 years, so I will continue to trust management to allow capital, much more than dividend lovers.

In terms of cash, the company returned $17B to shareholders between dividends & buybacks and still sits on a fortress of $60B of net cash, partly stored in short term treasuries yield great passive returns.

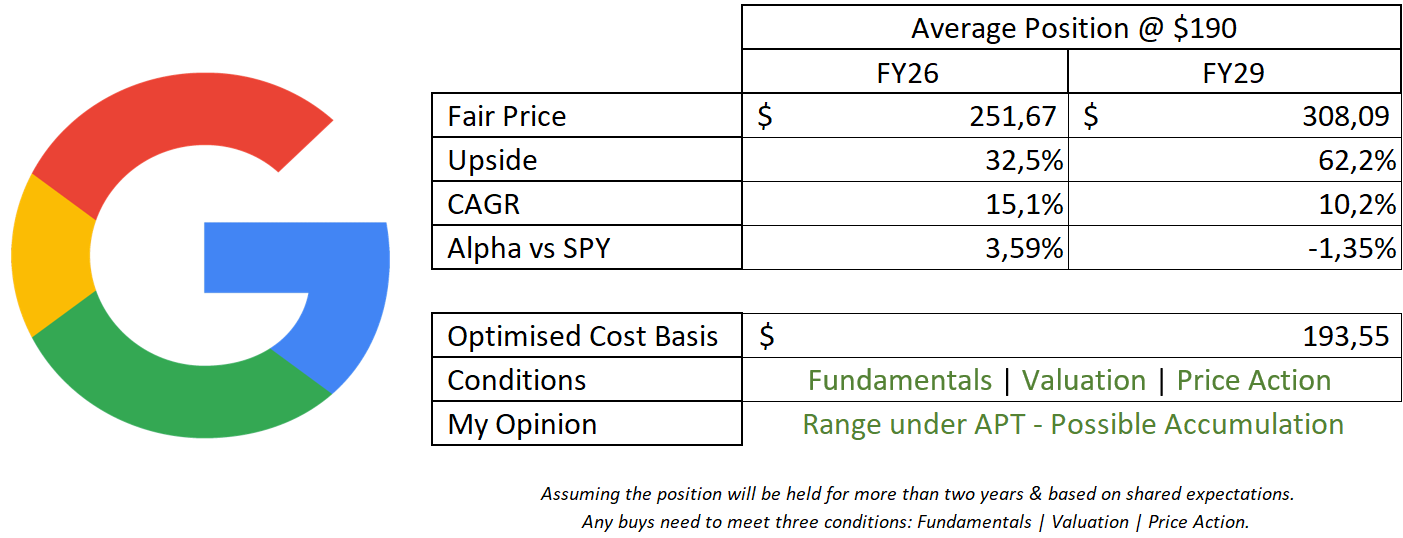

Investment Execution.

Google continues to be a great opportunity in my opinion, and anyone with a clear & bullish bias towards the company and no fear about that famous disruption could accumulate at today’s price.

This model assumes a 13% & 10% CAGR growth until FY26 & FY29 respectively, 30% net margins, 3% of return to shareholders & P/S & P/E at 6.3x & 28x respectively.

My assumptions are pretty conservative, nothing overly bullish at least, and yet it tells me that I could open a position at today’s price, even after a 35% pump from its local bottom. That speaks volume.

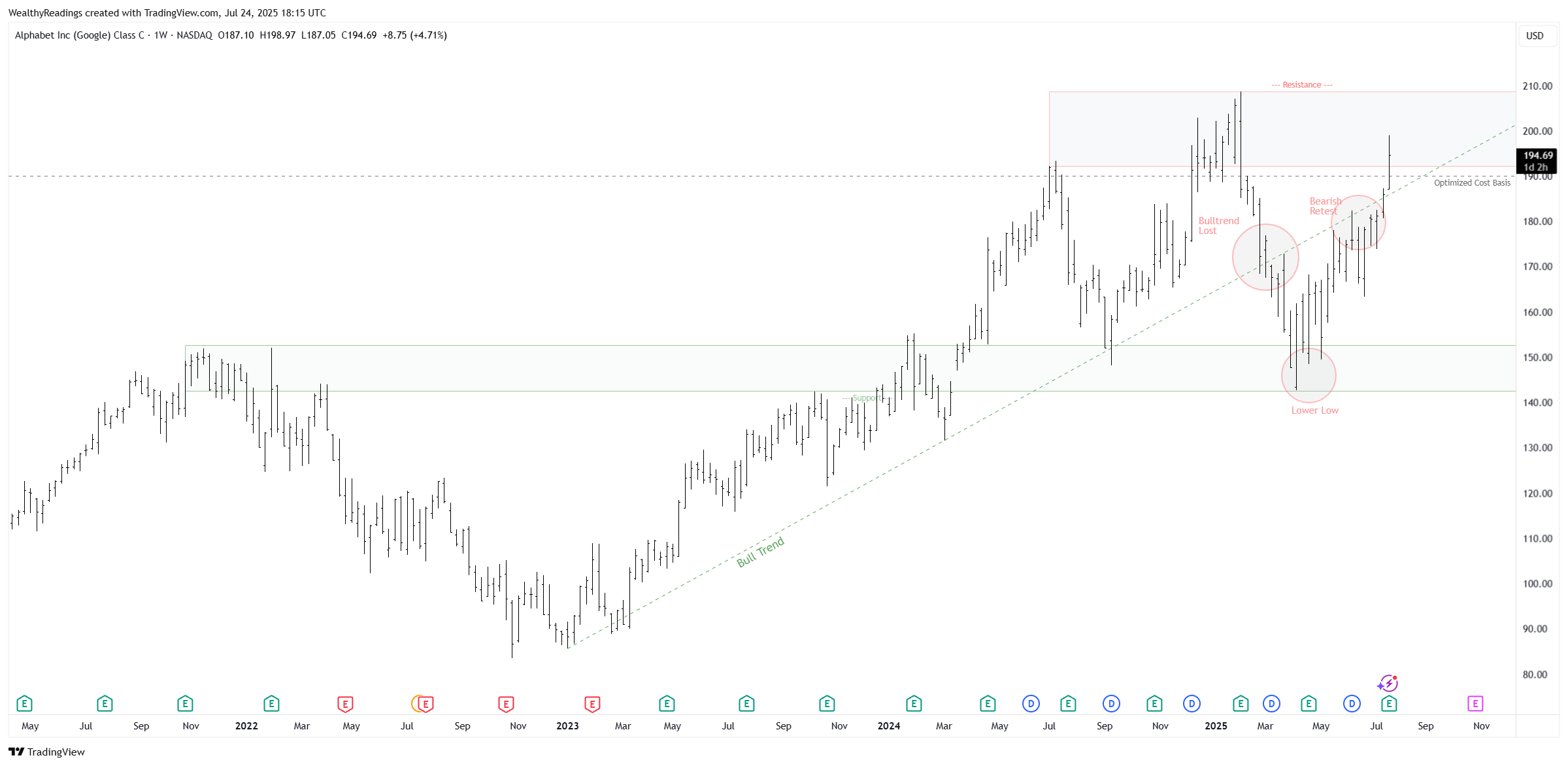

In terms of price action, I have not been the most bullish on the name as many stocks are posting ATH on ATH & shitcoins are pumping while Google struggles to stay green after a perfect quarter. It’s hard to know what the market expects from it. Potentially even more confirmations.

We’re up to a strong resistance while the market is at an all-time high. It’s all about time frames here in my opinion.

The quarter was perfect and showed that Search is very healthy. The stock will do what the stock will do, but I personally do not see anything wrong here in term of fundamentals, financials, valuation nor price action.

What else does a long term investor want?