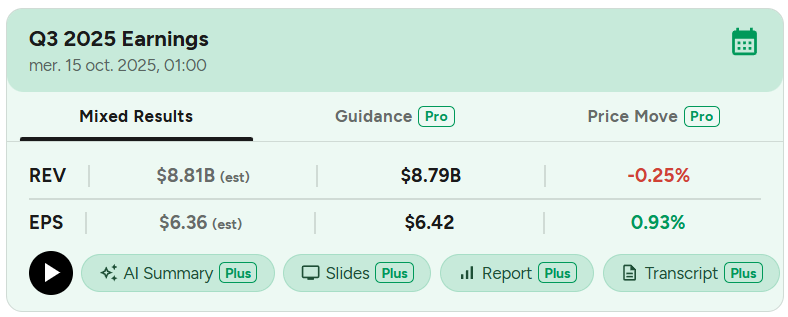

ASML Q3-25 Detailed Earning Review

Business as usual and market optimism.

If you guys are interested, you’ll get a 15% discount on FiscalAI through my referral link below. FiscalAI is the tool I use for KPIs in all my write-ups - powerful, data-rich and with great UX.

https://fiscal.ai/?via=wealthyreadings

Everything you need to understand ASML’s thesis is here.

ASML remains one of the strongest and most stable businesses in the AI sector, but not the best stock in my opinion, for one reason: management’s conservatism.

ASML does not expect 2026 total net sales to be below 2025.

A conservative management isn’t necessarily a bad thing though, as they have reasons to be, and it is refreshing to have a management who doesn’t oversell hype or unrealistic expectations.

ASML is a steady ship.

Business.

We can divide this quarter’s results into three key areas:

Resilience and growth from Western markets

Concerns about Chinese demand

Management conservatism

Quaterly Data.

In term of technology, lithography continues to gain momentum, as expected.

On the technology side, we see litho intensity continue to develop positively as EUV adoption gains momentum, including progress on High NA EUV.

In term of business, it was a solid quarter: healthy sales and a backlog that nearly doubled YoY - though helped by last year’s weaker order book.

Keep in mind that ASML recognizes revenue after installation and client validation, not at booking, meaning that backlog can take years to convert into revenue. An analyst pin-pointed one of the reason for ASML’s volatility in bookings.

Obviously, we’re all seeing the headline with AI and everything and you have been highlighting how AI could drive incremental investment. But the way I see it, you’re also constrained with increased concentration of customers on your logic and one customer is doing all the investment for the leading edge. And that by itself drives more volatility in your booking, backlog and even quarterly revenue. And I’m not asking you to name that customer, but is that the right way of thinking about how AI is incremental, but it does limit your visibility?

Yes. I don’t think we need to mention the customer. Your point is clear. But I think we discussed that. I don’t think there was any concern in term of either visibility or in term of sometime pricing power.

For those who need names, we are talking about TSM.

And as long as we are talking about pricing power, here is how it materialises. As products become more advanced, they’re costlier and take longer to manufacture, explaining lower volumes but higher value.

ASML’s monopoly on cutting-edge lithography puts it in a comfortable position with clients who have no alternatives, reinforcing a virtuous cycle of dependence.

The XT260 is an eye line scanner designed for applications that include advanced packaging and offer up to four times the productivity compared to existing solutions. 3D integration is of increasing importance to the roadmaps of our customer and the semiconductor industry, And our customers have been sharing with us the need to innovate in order to meet their future requirements.

Overall: we’re talking about a steady continuation for ASML’s business.

The Western Market.

Management remains positive on semiconductor and AI demand, with factual data pointing to more growth.

On the market side, we have seen continued positive momentum around investments in AI, and have also seen this extending to more customers, both in leading-edge Logic and advanced DRAM.

As we have seen earlier, ASML relies on TSM for its business so a broaden demand is a net positive for everyone. But they also have concerns on how the news - hence not factual data, will translate into revenues.

I think we are a bit careful with how the big announcement can translate into real capacity need on the ground.

This is the only conservative comment in the call - repeated with different phrasing, so I wouldn’t worry much about it but I wanted to stress once again that this constant flow of news is a positive for the market, but until paid for, it is only news.

That being said, we had many more comments about the growing demand and broadening customer base, which is a net positive for ASML.

I think the one thing I’d still like to stress one more time is we see the broadening of the customer base […] I think we can all agree that we need to make sure that the market will not be supply limited. And this has always been a risk with a limited amount of customers supplying AI chips, both in logic and DRAM. So I think the broadening of the installed base is a very good news there.

Although that means more pressure on manufacturing.

And on the last question, we have said for a few quarters that we have been preparing for growth. So we were following those dynamic. And I think we know now that EUV most probably will be stronger next year. So we’ve been preparing for that.

ASML’s hadwares cannot be built in a few weeks and as we’ll see later, they are still clearing their backlog from two years ago which gives you an idea for the delays. A rising demand will require to accelerate or accept a slower growth.

I think it is fair to conclude that ASML is manufacturing constrained; demand isn’t an issue. But they need time as they recognize revenues once the hardware is installed, growth isn’t as fast as it could be.

On the positive side, a larger installed base and sustained demand continue to drive service revenues higher, a trend already showing a clear upward trajectory.

And so while we might have had a bit more upgrade business in the first half, the second half is really benefiting from the service business. As you know, the service business is very much tied to the development of the installed base in EUV, right? And with the increase in the installed base in EUV, of course, that also drives further drives up the service business. So that’s an important one that I think you can sort of back of the envelope calculate what the impact of that is going to be for next year.

And once again: the trend is for more complex devices to be installed in the near future.

The Chinese Market.

It’s no surprise that China wants to be part of the high-end semiconductor and GPU race. That means either relying on TSMC’s lithography or buying their own directly from ASML, which is what they’ve been doing, supporting a massive backlog placed few years ago.

I think on China, we have been very consistent that we saw that the level of business in the last two, three years was very high and in no way normal. So I think we have been experiencing a very high cycle in China, especially through the last couple of years.

Like Nvidia, ASML faces export restrictions: no EUV can be sold to China; only certain older DUV models are allowed and require export licenses. Management expects this temporary wave of demand to normalize going forward.

And again, our expectation and the visibility we have right now is that next year we go back to more reasonable business.

So for quite a while, the China sales were very high, because we’ve been eating into a substantial backlog because of underserving the Chinese market […] we were actually quite surprised that the China sales this year are as strong as they are. So that’s the reason why we’ve indicated this assumption of significant decline. So that’s based on our understanding of the market. It’s based on the dialogues that we have with our customers. Could that change? Absolutely.

ASML management has a much better appreciation of the reality, but China doen’t seem to be slowing on investments to catch up in the semiconductors sector.

Time will tell.

Management Conservativism.

I believe most of the data shared this quarter is enough to stay bullish on ASML long term, and I am. But management continues to be conservative in both their guidance and their tone, for a few good reasons.

Manufacturing delays. Management confirmed that a portion of the actual backlog would only be fulfilled post 2026.

But to your point, there is already a healthy order intake in the backlog that is beyond 2026.

News are just news. As mentioned earlier, demand trends exist but most of them haven’t yet converted into bookings. Until they do - and they might not, it’s difficult to establish a solid growth trajectory.

The Chinese market remains unpredictable. Geopolitical tensions and China’s growing tendency toward self-reliance could limit ASML’s access or slow orders.

Once again, a conservative management is not a bad thing. In investing, it’s often better to consistently beat targets than to miss overly optimistic ones.

Financials.

Nothing surprising here; we’re looking at 20.8% YTD revenue growth YoY, with margins continuing to expand.

As ASML sells increasingly advanced technologies and grows its installed base, this trend is logical and should continues with fluctuation between quarters depending on product mix - some systems have higher margins/prices than others, but the overall direction remains positive.

A larger installed base also means recurring service revenue, which benefits both growth and profitability.

In terms of cash, ASML posted a negative free cash flow of €2.1B due to significant investments. The company holds €5.13B in cash, repurchased €148M in shares and paid €620M in dividends.

ASML also invested €1.3B in Mistral AI - the French OpenAI, have a sit on the board and uses its LLM to enhance internal operations. A smart and use of cash to me.

Once again, business as usual.

Guidance.

Management expects €32.4B in revenues FY25, implying at least 14.6% YoY growth.

More details about 2026 after Q4-25, but management expects more demand higher-margin products in Western markets and slowing demand from China.

In this environment, we also expect the 2026 EUV business to be up, driven by the dynamic in advanced DRAM and leading edge logic and the Deep UV business to be down compared to 2025, driven by the dynamics with our Chinese customer.

Investment Execution.

The market has rewarded ASML over the past few months because sentiment flipped from pessimism to optimism after the numerous AI data-center news. Management remains conservative and the business is as usual; only market mood has changed.

That’s all it is.

This was another steady quarter, confirming strong global demand that continues to shift toward more complex - and expensive, hardware; a net positive. The remaining question is whether ASML can produce fast enough to match analysts’ growth targets.

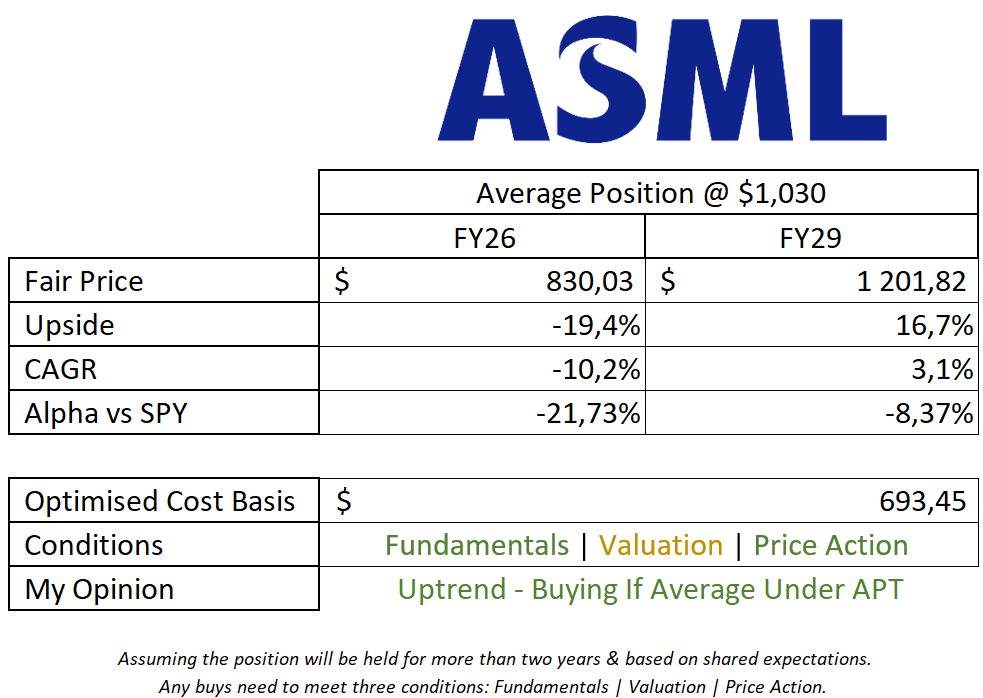

I have no concern about the business itself. I called ASML a buy around $700 or so two months ago, nothing changed fundamentally.

This model assumes a 12% CAGR growth until FY26 & FY29, 30% net margins, 1% return to shareholders, and a P/S & P/E at x37 & x9.5 respectively.

Logically, there’s no significant change in my valuation. I see ASML as an outstanding business with an expensive stock today given limited visibility on future growth due to manufacturing constraints mostly, as we know demand is here - which pleased the market.

In term of price-action, the stock is nearing all-time highs and is pretty extanded from its EMAs.

It’s impossible to predict short-term moves, but until Q4-25 & management updated guidance, I won’t have more business oriented data to change my assumptions. So I’d stay cautious & potentially accumulate on dips; ideally a retest of the 21 daily - red line, or the $820 breakout area. Nothing else.