Alibaba Q1-25 | Earning

The bull case continues to play out.

If you do not know about Alibaba, everything can be found here.

The thesis remains simple: a growing demand for cloud & AI services in China which can be satisfied only by a Chinese company coupled with a growing consumption of leisure products locally & by neighbors.

Overview.

Revenue. $33.08B | $32.58B | -1.50% miss

EPS. $1.48 | $1.73 | +16.89% beat

$600M of buybacks.

Business.

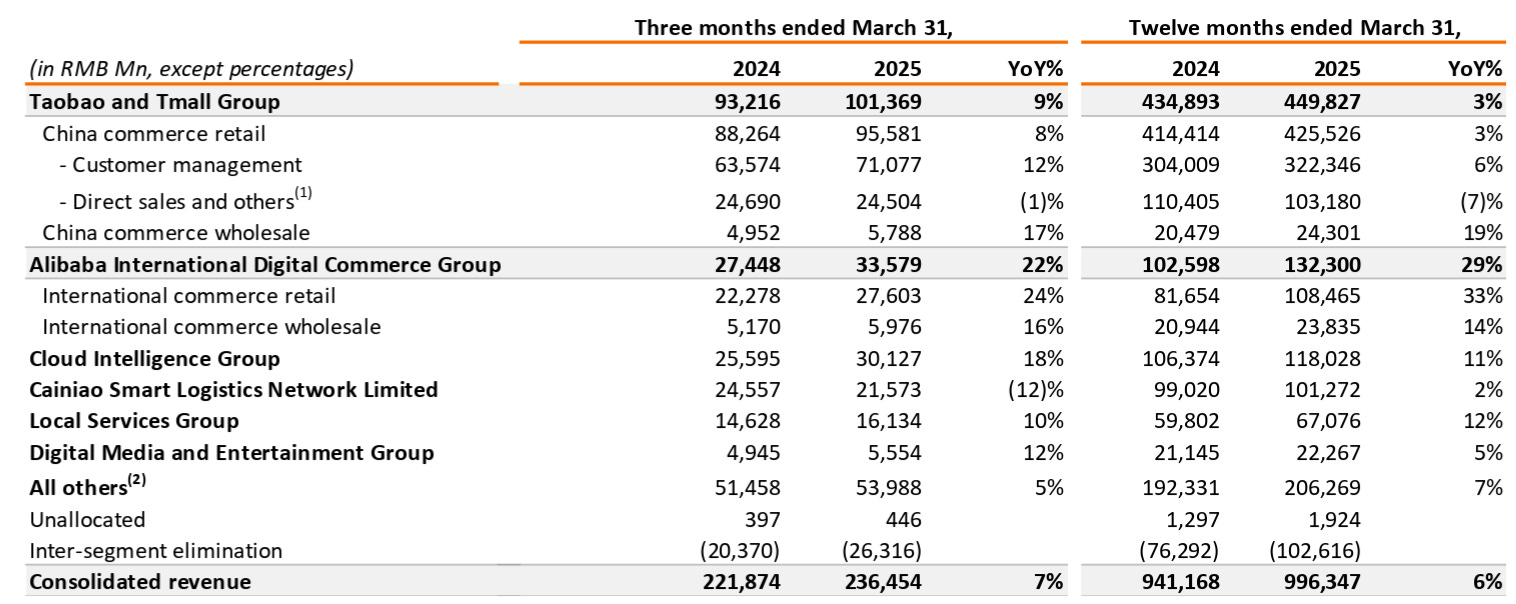

My bull case continues to play out with strong & stable growth in every important branch, accelerating in some cases.

The local e-commerce is as healthy as usual with accelerating growth over the last year, fueled by their change of monetization from a year ago & a growing take rate more than growing consumption though. But usage remains strong globally.

“We continued to invest in user growth and other strategic initiatives such as price competitive products, customer service, membership program benefits and AI technology applications to enhance user experience. These efforts led to stronger momentum in new consumer growth and continuous increase in orders.”

Nothing more to comment. More improvements to come on their platforms which seem to please users as the VIP members are growing double digits YoY. More work to do on conversion to reboost consumption, but this will play out with time. Will be important to monitor it though, growth has to come from consumption to really confirm the thesis.

International e-com remains constant with strong & stable growth fueled by AliExpress & Trendyol. Slightly decelerating but nothing unhealthy. The branch remains unprofitable though as management continues to focus on customer acquisition & retention. Strategy doesn’t change.

More important, AI & cloud growth continues to accelerate, above triple digits on their AI services, and is growing profitability. This remains a huge part of the bull case & management plans to continue to invest in its infrastructure to keep its leader spot in this Chinese sector.

“We will continue to invest in anticipation of customer growth and technology innovation, including AI products and services, to increase cloud adoption for AI and maintain our market leadership.”

On the others, Cainiao is fluctuating as usual, other services are growing healthily, all others follow a compatible trajectory & Digital Media & Entertainment continues to not really matter in my opinion.

Financials.

Some improvements.

Revenue growth is stable & higher than expense with costs actually declining YoY, certainly due to their growing take rate & portion of revenues coming from services, hence higher margins. Interesting to note a growth in S&M, although really reasonable. All of those ending up growing margin & cash generation, with net income YoY comparison strongly affected by some external factors, namely Alibaba’s equity value in Ant Group & more.

In terms of cash, $26B of net debt for $516M FCF reduced by much higher CapEx for their AI & cloud infrastructures. Buybacks are slowing as the share prices pumped well these last months, which is pretty much what we want to see, reflects good cash optimization focusing on future growth trajectories.

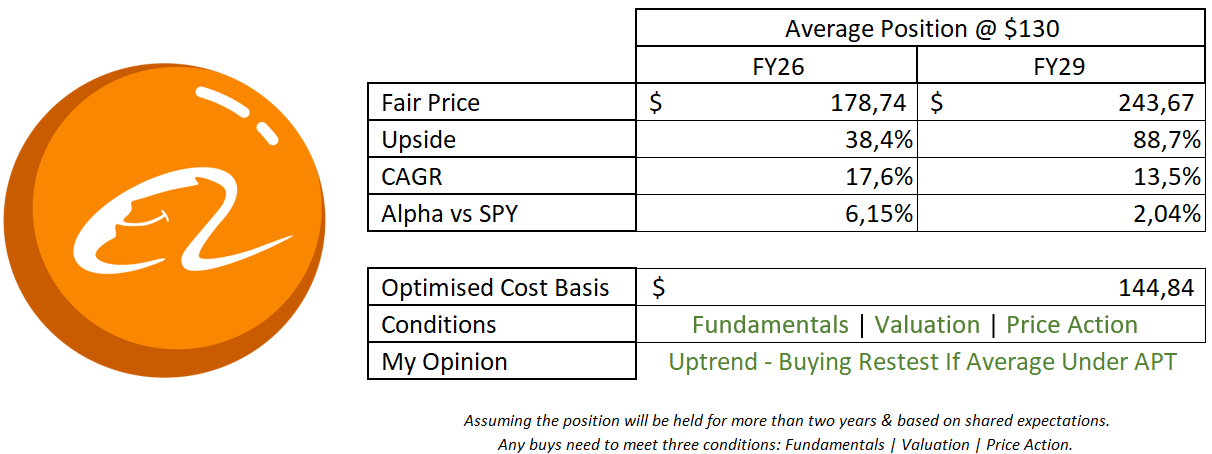

My Take & Valuation.

Pretty good quarter without much to comment on. The company continues to execute & respect the bull case. I would like to see the Chinese e-commerce grow organically, from more consumption, not take rate optimization. More revenues from services is a good thing as it means users are relying more on the app. But growing consumption is what we want.

Valuation is complex for Alibaba, multiples can be affected by many factors, including a Chinese discount. For references, Amazon is actually trading at 34x earnings & 3.4x sales but growing slightly faster & being an American company, while many consider it “cheap” at actual valuation. I wouldn’t use the same ratios, but slightly lower seems really fair while growth should remain stable due to their cloud business - also raising margins, & constant one from their retail.

This model assumes a 7% & 7% CAGR growth until FY26 & FY29 respectively, 12% net margins, 3% returned yearly to shareholders, P/S & PER at x2 & x30 respectively.

As usual, everything depends on China & how multiples will be applied to their stocks, but there are no doubts that Alibaba is healthy, growing well, perfectly positioned to take the lion’s share of its region’s growth both in terms of consumption & technical demand. Not to ignore, personally holding & ready to buy more on opportunities.