Airbnb Q1-25 | Earning & Call

Nothing is really improving.

If you do not know Airbnb nor why I believe they can change travelling during the next decades, it’s all argued here.

Overview.

This will be a rapid report.

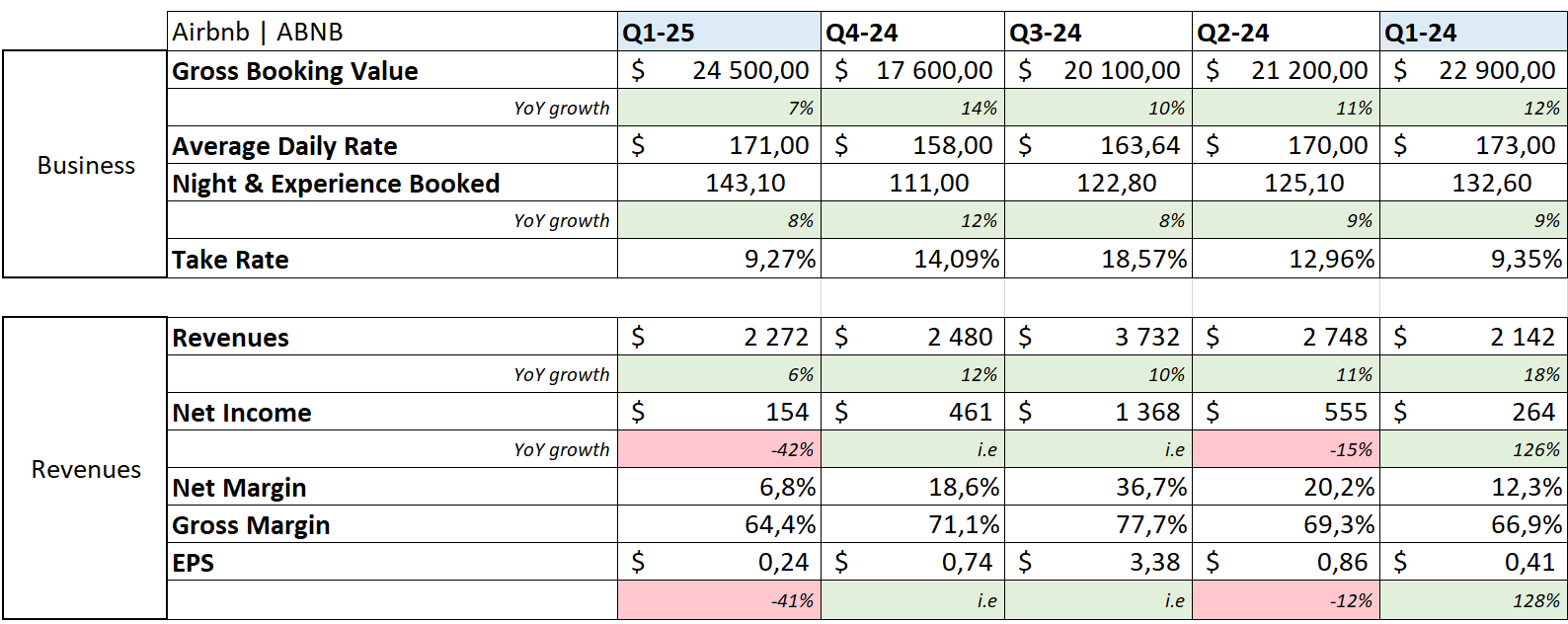

Revenue. $2.26B | $2.27B | 0.53% beat

EPS. $0.23 | $0.24 | 4.35% beat

$807M of buybacks.

Business.

Global usage growth is clearly slowing YoY - sequential comparisons make no sense. Airbnb is now a single-digit growth business which management tries to explain with comps timings due to Easter & currency mix. Truth is, the decline is since quarters now & FX or Easter can’t explain it all.

Comps are obviously getting harder as the business grows but you’d expect Airbnb to be able to maintain & attract more as the renting market is not a small one. But is isn’t happening, growth remains stable in dollar value hence declining in percentage.

On take rate & average daily rate, those remain stable & have to as Airbnb is meant to scale on volume, not pricing - I detail this on the IC clearly. To remain competitive, they need prices low so volume grows as travellers choose Airbnbs over hotels.

“We're trying to get them to the best price for their listing that will drive more bookings. And in many cases, that will be to reduce your price.”

Low prices are a good thing for Airbnb as long as volume is here, the problem is… It isn’t at the moment.

In terms of geographies, the new ones continue to outperform. Latam is growing in the low 20s% - Brazil leading the growth with 27% increase in nights booked, Asia is healthy with mid-teens growth while NA is growing 2% & Europe around 5%.

On the bright side, there is growth in their new markets which means they are able to onboard new users outside of west. It is important to grow Airbnb in the heart of those who’s buying power is growing - namely Asia.

“In Q1 2025, we saw both first-time bookers and domestic nights booked in Japan increase double digits with domestic nights growing over 20% year-over-year.”

On the dark side, the core businesses are really slowing down, without clear answers on the reasons - although I remain biased on the lack of consuming power & the growing uncertainties which do not allow to plan trips.

“Excluding North America, Nights and Experiences Booked grew 11% year-over-year in Q1 2025.“

Except for the higher income which, as I said many times by now, aren’t yet impacted by the actual macro but could be if asset prices were to take a hit.

“We see, in particular, the higher ADRs of our bookings, the growth is very stable and and and very healthy for The US traveler.”

Globally a lot of uncertainty in the west which leads to different behaviour in terms of lead times & decision making, while new geographies are growing really well & their users are being onboarded on the app - which is great long term.

Beyond the core. We know since a few quarters Airbnb is working on expanding its offerings beyond housing & we will know more during their usual summer release.

Still no indications on what it will be but a good question was asked during the call as if it will be something entirely different or just a revamp of actual features - as we had a call a few quarters back where they said they’d redo their experiences services. No clear answer was given.

Not gonna lie, if it is what this is all about. It will be highly disappointing.

Financials.

Revenues tell us the story of a slowing business.

Low revenue growth partly due to external factors - FX & timings, but mostly from a lower consumption of the service - we have to be real. On another hand, expenses aren’t slowing down & SBCs are a big part of those - as we’ll see later, which puts huge pressure on the margins - both net & gross down YoY & QoQ, which isn’t good. Especially when you know they intend to grow marketing expenses to sustain their new services during the rest of the year.

“Marketing expense will grow faster than revenue in q two, mostly due to our upcoming summer release and investments in growth initiatives.”

In terms of cash, Airbnb holds $8.5B of net debt, generated $1.8B of FCF & returned $807M to shareholders through buybacks with $2.5B left on their authorized plan.

Important to note the growing SBCs which represent 20% of FCF while business is slowing. This isn’t a winning combination & doesn’t send the best message to shareholders.

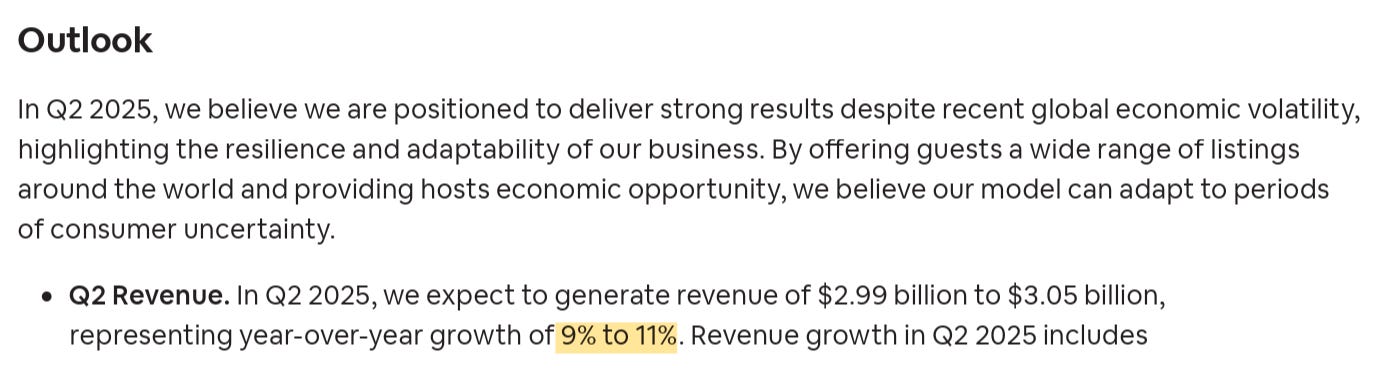

Guidance.

Data is also pretty weak.

We have to take in consideration a favorable comps due to Easter weekend - which Airbnb calls a negative comp for the actual quarter, plus a favorable currency environment as the dollar has weakened considerably those last weeks.

Only growing 11% at best under favorable conditions & comps clearly shows that the demand for the business itself is slowing.

My Take & Valuation.

As I said, pretty short. The bottom line is clear: business is slowing either due to a lack of demand for their business or because of external factors. The only light I can share is that Booking’s growth is following a similar pattern.

This tends to push towards the second argument, which is also my bias - as I share with you every day & you should know by now.

In terms of fundamentals, their playbook is working & fueling growth with emergent markets, global results are dragged down by their core markets & the actual situation with no visibility on where we are going, while their new service - which we do not knwo what it will be, is going to put pressure on the company’s cash generation through growing marketing.

I continue to believe the business is wonderful & it brings a lot of value for travellers. But it sure is struggling right now & that SBC tendency is not pleasing me at all. I am very curious on May 13th but am also feeling disappointment coming.

Valuation is tough to make. This model assumes a 9% & 7% CAGR growth until FY26 & FY29 respectively, 15% of net margins, 2% of returns to shareholders & multiples equal to its 3Y average at x38 earnings & x9 sales.

I have two comments to make.

The positive one is that growth assumptions are based on the actual trends, which are weak in the west. Any change or stronger growth in new markets as Airbnb releases its playbook could boost the numbers. Plus, this does not include their new business, which if interesting could yield more growth by FY26.

The negative is that if Airbnb’s growth doesn’t re-accelerate, it won’t deserve its 3Y average multiples as 9x sales & 38x earnings are pretty big.

In brief. My opinion is that Airbnb is a wonderful business with enormous potential. But I do not feel good attributing liquidity to it at the moment, too many unknowns short & medium term. I will hold my small position on the Buy & Hold portfolio until May 13th, to see what they have in store for us. My position will depend on it.

This is because I have a position. If I didn’t have one, I wouldn’t be buying. There is no rush and I don’t see the stock rocket without any reasons. We have time to see things coming, the economy getting better & demand grow.

Thanks for the update! Seeing abnb don't offer a dividend, why is it being held in your buy and hold? Just curious