Airbnb - Investment Thesis

The adventurous one.

Airbnb will be the first to have a new and complete investment case as I haven't discussed it for a while, although it is without any doubt one of my favorite companies and stocks for the next few years.

I'll detail here most of one needs to know before deciding to invest in $ABNB - or not.

[Company]

I believe everyone knows what Airbnb is and its services but I'll still talk about it briefly. It started with the simple idea of creating a platform to connect two kinds of people: tourists and hosts. Many attempted this over the years but failed because they lacked one very important thing: trust. That's what Airbnb brought, not as much the technical way of doing but a trusted platform where hosts could safely rent out their homes.

And it works because Airbnb found a way to create a triple-win situation.

Hosts need to rent out their property, a clean house which respects the description and pictures; otherwise, they'll receive negative reviews from tourists and their announce won't show up first in the app, attracting fewer visitors. Tourists need to behave and participate in the social aspect of the platform so their record shows good behavior or hosts will refuse their bookings. And the platform has to ensure that everything runs smoothly so both continue to use it.

Everyone has a role. Everyone needs to fulfill it, and those who do it well will be prioritized over those who don't. It incentivizes good behavior. A very smart and simple concept working with a well-developed and simple app.

Airbnb was meant to offer a new alternative to travelers, offering them more than just a bed, an entire experience. They want you to feel comfortable, at home, anywhere in the world. You can find every kind of place on their app, from simple and cheap rooms to luxurious villas. It is a kind competition to hotels in cities but that's not where Airbnb shines. Airbnb shines everywhere else because it offers things none of its competition offers.

That's how Airbnb grew during its first years, and that's where it is today with around 8 million listings all over the globe and a huge advantage for out-of-city rentals. The CEO and founder, Brian Chesky said last year that the company was now ready to expand its offerings. They'll still focus on their main activity, which is long/short-term renting and expand deeper into new countries, but they'll start to work on and release new services. The goal is to become the personalized travel agent, as he kinda teased in the Q4-23 earning call.

"You should start by seeing us do the things that are the most logical extension of what we already provide, and then we will move further and further out from our core as the things we launch are successful."

In the era of AI and data analysis, Airbnb can evolve and propose much more. They already have a pretty loyal user base which will probably use any new service they propose, as long as they're as good as the rental one.

[How do they make money?]

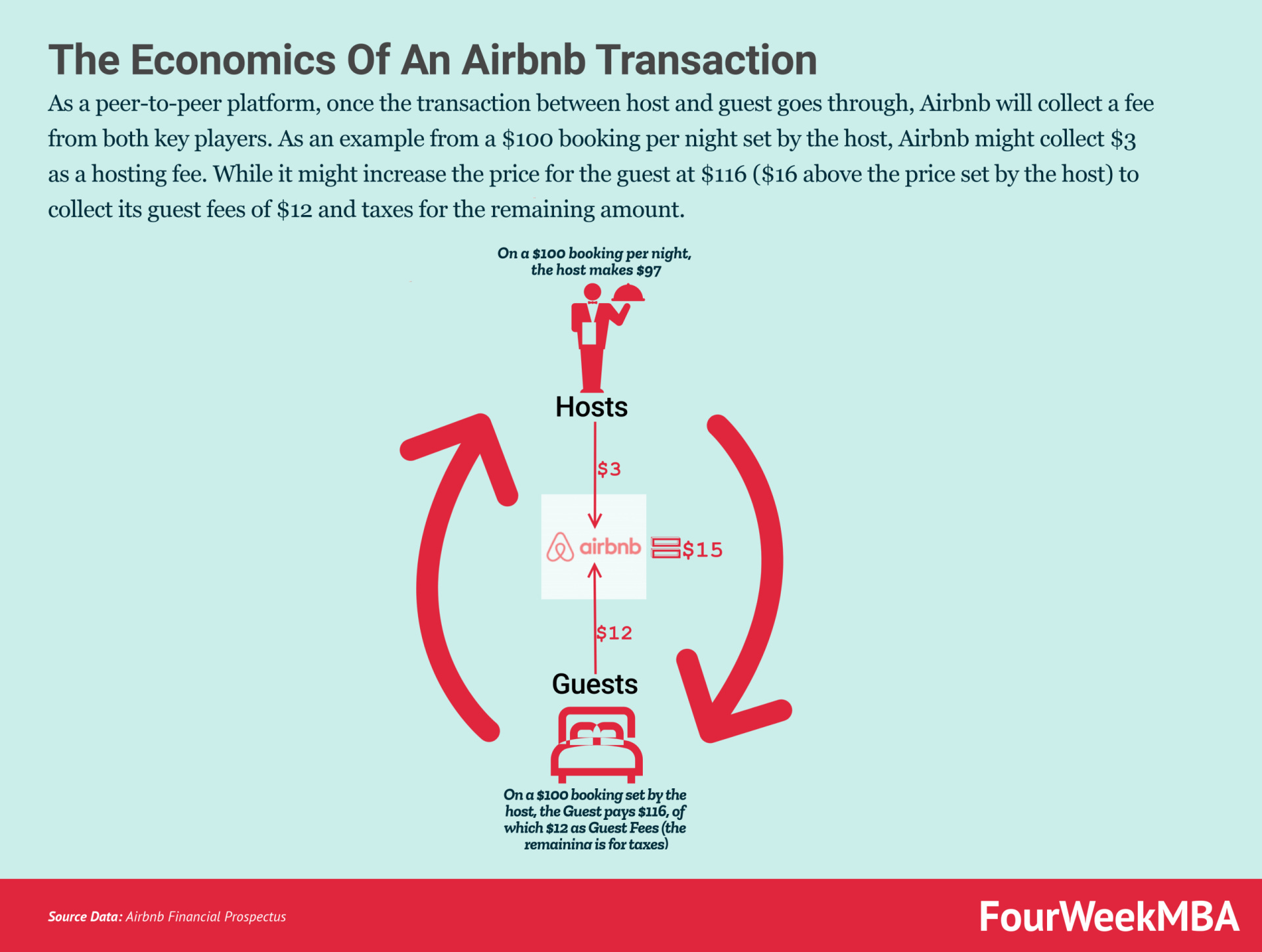

It's pretty simple. As I explained and as of today, Airbnb is simply a trusted interface between two persons. They'll simply charge a fee in between them, each time a transaction happens through their platform, hence, each time a home or flat is booked.

And because they're pretty smart about it (although this is common sense) the fee is a percentage of the amount booked - roughly 17% at the moment. The revenues of the company are therefore hardly depended on the success of their app - and the number of reservations through it or, more precisely, the amount.

It makes Airbnb a software company, one of the most influential house renting services - which do not own any house, with high margins, ROIC, and revenues per employee while maintaining minimal risks - in the same order, above 80%, above 45%, and more than $1.5M per employee.

[Market]

The company is still developing, but most of its revenues are from tourism and that's why the team decided to expand in some specific countries first - western Europe and the U.S where tourism is a big deal. They've been following the tendencies, growing very fast in Asia lately for example - since Bali and Thailand became some praised destinations.

Tourism is a huge market which has always been and should always be growing as most individuals on earth participate in it, and it shouldn't change soon, although a cyclical business - depending on holidays seasons.

The short term rental market is estimated above $100B as of today which would give Airbnb a 10% market share. Not bad for a decade old app playing "against" hotels existing since centuries. It clearly shows that Airbnb is offerng something new & demanded.

The market should grow around 10% CAGR over the next years to reach $315B by 2033 as displayed in the screenshot, which would give Airbnb revenues of $30B by then if they were to keep their 10% market share and not expand to other services. But they won't stop there so let's check larger targets, the tourism market at large.

This is very large and we cannot know what services Airbnb will propose in the futur but this is simply to show that there is a lot of space and a lot of potential revenues for them.

Now this is the market which impacts Airbnb but as I said early, Airbnb is a software product and its competition isn't really in the tourism market, it's in the tech market. More precisely, its "competition" are every company proposing online house rental, regarding of the type of rental - as once more, Airbnb is pretty unique in what it offers. We're talking about TripAdvisor, Booking and other Expedia for the bigger names.

It is a bit more complexe as Booking & Tripadvisor offer more services such as flights or car rentals and tripadvisor will also be used for informations about restaurants for example, so we cannot really compare the companies in term or revenues nor traffic, nor much... Not if we want to make perfect sense at least.

So I'll leave it here, to know who is the "competition". The quote are here because they're in the same industry and offer comparable services, but very different products. I already wrote something on the comparison between Airbnb & Booking which are often view as competitors. The reflexion goes further to my opinion and that's detailed here.

https://twitter.com/WealthyReadings/status/1761374117113008507

[Moats]

We gotta talk about what makes Airbnb so special because after all, they're only an application which interfaces two needs. What makes it different & better than other?

Network effect. This is the first and most important point in Airbnb's investment case today, its network effect. The more users you have, the more important your app will be and the more market shares you'll own. I all started with the hosts, the company's focus was to grow their supply and it grew pretty fast the last years, up to bit less than 8M today.

The more choices you have around the globe, the more vacationers will come to your platform. And when you reach the amount of users Airbnb has today - with more than 400M bookings last year - we can call this a network effect. Users always come back to your platform & use it as their first choice to find a place.

I even have a friend who uses the app to scroll houses and have ideas for her next holidays.

The app. One more side of this network effect is the simplicity of their app (a really good one) and its accessibility to everyone around the globe. It's true for its competition as well but it's important to understand that wherever you go, you can simply open Airbnb. I travelled to Asia not long ago and it's much easier to open Airbnb than to find the proper website where you'll find the Asian short rental market, because they're of course different than the one I use in Europe or to go to the U.S.

Each continent has differents platforms and ways of working. But when you use Airbnb, you know what you'll find, how it works and how to book. It's convinient, for everyone to go everywhere.

Brand & trust. By now, the expression "rent and airbnb" is pretty common at least in Europe but I'm pretty sure it became global in the entire west now. That's the network effect combined with a clear app and a trusted service, it created an entire brand which has a lot of value today. And a new word.

Offerings. The question still is, why did people go and keep going to Airbnb instead of more traditionnal apps? Because Airbnb doesn't offer a traditionnal product, they offer an experience - I said that already, didn't I? But it's important.

Their offering are very different from what you can find with classic hotels - which is every competitors' offerings. If you want to go out of the cities, in the French countryside or Tuscany, you'll sure find hotels but it's going to be tasteless, boring, not really what you want to live la dolce vita.

In Airbnb, you'll find thinks like this.

I might look ridiculous to you (and I took some extremes on purpose) but you get the idea. An experience, not only a room to sleep.

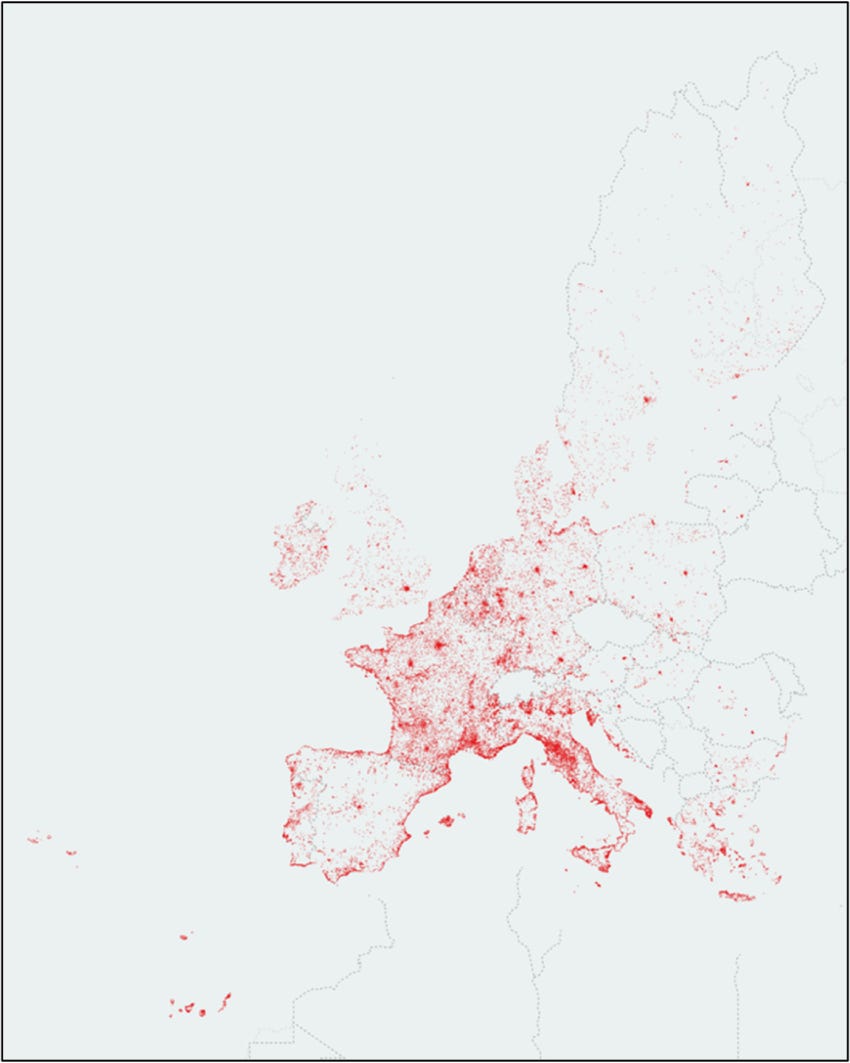

Geography. Because we're talking about an individual to individual service (through the app) we're also talking about house or flat to rent everywhere, not only in cities. Your grandparents can rent the countryside house to anyone while there's literally nothing around and the closest hotel is 50km away. That is something only Airbnb offers - other tried but got smashed by its network effect because if as an host you're not on Airbnb, you won't be booked - or will be booked much less.

I couldn't find a great map updated so this is from 2020.

Pretty easy to understand that if you go to France, Italy or even Ireland, you'll find an Airbnb wherever you want to stay. I went to Finland some weeks ago and I can assure you I was glad about my Airbnb choice, such a beautiful place which made our stay much, much, so much better than it would have been otherwise on the hotels around - pretty sad rooms without much choices.

Occupancy. A huge difference compared to most of its concurrence, their hosts don't care about occupancy. They are of course looking for returns on their properties but they do not need to cover costs such as employees or expense bills like hotels do. They're okay to have people, they're okay to have weeks without anyone.

Even though it isn't Airbnb's problem, it does matter for them as they do not need to push rentals in priorities to their clients as Booking needs to do for example - because yes, they do that. Airbnb only focuses on quality and when the end users look for anything, they'll find the most recommended houses first.

Quality is what matters and quality is what's brought up first in Airbnb. Be better, the algorythm will recognize it and push you forward, you'll have more clients.

Quality.

Pricing. Something else very important to understand for Airbnb is that they need their prices per night - or the rental prices of their hosts - to be low. This is a huge leverage for the company and they'll always work on reducing it. Why?

Simple enough: to grow their network effect. Cheaper attracts more users and therefore more revenues & a stronger grip on their market. And they can do it by promoting monthly or weekly reductions for example. The hosts will be happy to use such discounts because it'll make their rental more attractive to vacationers. It starts a pricing war in regions which should draw the global per night prices lower.

A mechanism which pleases the vacationers because they pay less, the hosts because they have a way to fight competition and Airbnb which grows its competitive advantage on other rentals agencies thanks to very hard to compete pricing & offerings.

Hotels have a minimum price per night as they need to cover fixed costs. Hosts don't.

Data. This is important for Airbnb's future. They said they wouldn't stop at short term renting and will expand to other services although they didn't clearly state which, but it doesn't matter. What matters is that they own the data of millions of users on their platform and that means their ways of traveling, their budgets, their preferences, the frequency of their travel, what they like to see & do etc...

Tons of valuable data to leverage in the next years.

[Finances]

I think we now have a clear view about the business and how it works, let's turn to the investment side of it and start with the company's finances.

I said it earlier but it's important to keep it in mind, Airbnb is a software company with software margins, gross above 80%, net above 40%, and a ROIC above 40% - which shows a pretty good management & resource allocation.

Revenue. Typical growth company since its IPO in 2020 with a CAGR above 40% for its last three years. The bump in 2020 is entirely normal as it is due to the COVID-19 pandemic which... Well, evidently wasn't good for tourism. It did impact the business but it didn't impact the growth at all, nor the financial health of the company.

Net income. We have the same 2020 bump of course but besides that, we can see that the company has gone to profitability very fast which actually helped very much for its growth, thanks to its cash.

Cash & FCF. Airbnb sits on $10B of cash for $2B of debt, a comfortable position although the growth and expenses have been fueled by shares emission more than debt. A better way of doing to me, and for them as well as it helped the company to show a very healthy profile for different M&As through the years.

[Risks]

Every investment comes with risks but I have to admit that I struggle to find many for Airbnb, besides the classic ones of black swans like the COVID-19 or missmanagement. Truth is, we're in one of the most important markets, tourism, which won't stop anytime soon. Their brand image is at its strongest and all the data shows growth and interest in what the company offers, amplifying their network effect.

Things can change fast of course and a really great alternative can show up in the next years but it will take a lot of time for anything to push Airbnb away from its pedestal. There's one thing to note though.

Regulation. We've seen it in New York City in 2023 and that is something which could hurt the company, bad. Victim of their success, regulators feel like they have to restrain the service expansion as it could otherwise hurt the real estate market in their cities - with more empty Airbnb and higher rent price for locals.

The comapny's management team said many times that they're in great terms with most of regulators of cities where they're implanted and are working with them to ensure everything goes well for everyone. But it still is something to keep in mind.

There of course are other risks, more basics and valid for every investments but I think regulation is the only one "out of the box" worth noting here.

[Opportunity]

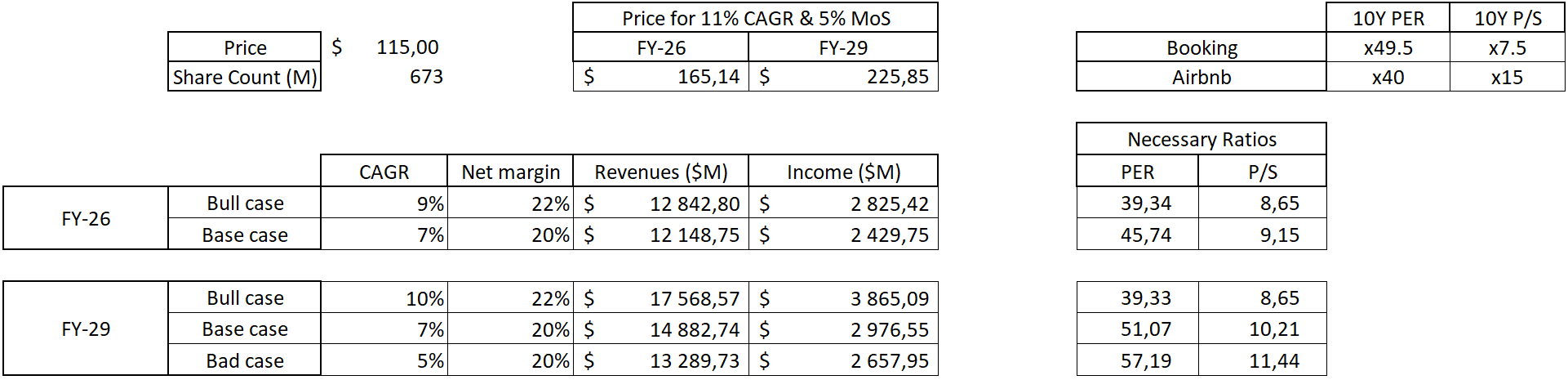

Investing is nothing but balancing risk and opportunity and it's time to talk about the latter. $ABNB did its IPO in 2020 and has been trading in two very large ranges since, one under $130 and the other one above $155. I won't dig too much into its actual ratios and will talk more about the company's fundamentals and potential.

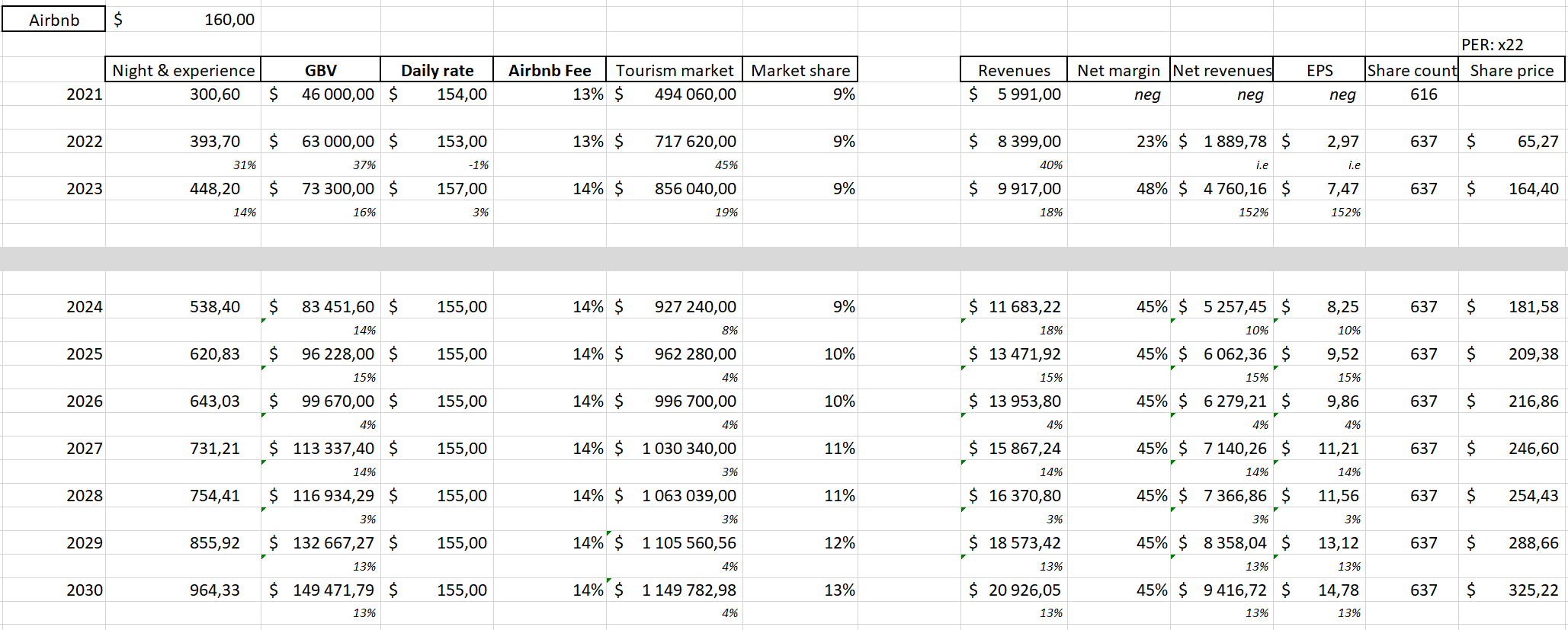

Again, Airbnb's revenues come from fees on the total amount of each booking passing through its app. Knowing that, the company has only two levers to grow revenues: Grow their fee or have more bookings - more precisely more Gross Booking Value (GBV).

As I explained earlier, it's very important for Airbnb to keep their price per night low to do more concurrence to hotels and attract more users to their platform so with that in mind, they probably won't increase their fee which should stay flat around 14% over the years - that's only my assumptions. So their only possibility left to more GBV (and revenues) is to grow their user base and the number of rentals they do through their platform. That's what I'll play with in my next slide.

I used the entire tourism market size shared earlier here for my computations.

All assumptions are based on the company's market shares which I intentionally grew over the years as Airbnb is expanding to more countries aggressively, its network effect is growing and they will very probably have released more services by then, possibly owning 13% of the entire market by 2030. Achievable knowing that Bookings' FY-23 GBV sits at more than $100B today.

Knowing the total market, Airbnb's market share & platform fees allow me to compute the company's revenues, net income considering a 45% net margin - which is what Airbnb does today so nothing crazy as to assume it'll stay flat in the future - and therefore EPS assuming that share count stays flat. With those assumptions, we would see a CAGR around 12% for the company, way lower than the 30% of the last three years but reasonable considering its potential & future services.

Update - 04/09/24.

Short tern growth has been revised since this write up as the sector is weakening with lower households travelling less and others not planning to far into the future & shortening their stays. We might be entering a slower period for this sector and the two years growth prevision should be revised.

Airbnb talked about an 8% to 10% growth YoY for FY-24, and we should not expect much more in 2025 as the new services, what Brian calls “the travelling concierge,” won’t be on the market yet. We might start to see them around 2026, but I wouldn’t base my assumption on it, so I will stay with very conservative growth.

Net margins are much higher this year only thanks to the tax provision they had during the third quarter of 2023; the company would be around 20% without it.

Even though the stock price dropped, we’re still around a pretty fair value assuming the slower economy and sector, but this last part is the most important part.

The travelling sector is a cyclical business, and bad economic conditions are always replaced by strong ones. Buying Airbnb around a fair value, assuming a weaker sector while the company is planning to expand its business and base its usage on AI entirely & expand aggressively to other geographies, all while nothing in its business changed… seems to be a pretty good deal to me.

End of Update.

[Conclusion]

I said it but once again, $ABNB is one of my favorite company and favorite stock to invest in for the next years, a very strong and growing company in a "safe" sector at fair valuation - to my opinion. I intend to DCA and hold my shares until... Either the company turns to sh*t or I need cash to buy something else I find better.

That's it for me, feel free to comment if I missed something or if you disagree with my take!

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!

Your net income assumption is crazy because ABNB benefited last year from a one-time tax bracket. I think more conservative is a 20-30% NI margin. Then the valuation looks different...