Weekly Recap | July - W3

Trump & the markets, Ethereum ETFs coming, Match Group & Starbucks under assault, Crowdstrick's mess, Amazon's Prime Day, some valuations and quarterly reviews.

Trump, Markets & Tech War.

We are hearing a lot about Trump lately as his chance to become the next president of the United States have never been higher - that’s what the polls show at least. This gives the markets a good excuse to listen to what he promises and react violently to anything he says…

Like when he proposed to cut down corporate taxes from 21% to 15%, which triggered a pretty green Monday. But he chose to come back on Wednesday morning to tell the world he wanted to review the U.S. foreign defense policy.

Nothing new for him, and although we’re talking about Taiwan here it is true for Europe, Japan, and many more countries. This scared the markets as most technology we use is built from Taiwan’s Semiconductors, and the risk of leaving the island defenseless against China was apparently enough to sell-off the entire chip maker sector.

I think there’s much questions to raise on this subject. Wouldn’t Taiwan accept to pay this “insurance”? Or would China invade militarily? Is the island really at risk? Cannot they defend themselves?

Lots of other factors to ponder here but the market chose to overreact and sell names like MU down -15%, Nvidia down -10%, TSM down -12%, ASML down -20%… The entire sector was trading at high multiples so it might be a needed breather.

Some tech stocks were also impacted even though they were not tradding at comparable multiples to the semi sector, the volatility gave some good buying opportunities to my opinion like with META around $460 & Amazon around $180 - personally bought both.

Lots of noise & sellings while fundamentals stay strong.

Ethereum ETFs.

I talked about Ethereum & Solana two weeks ago on the weekly recap - both bought at that time, noting that they were behaving very well compared to Bitcoin - expected since they were not under any selling pressure.

Solana is up 40% and Ethereum 20% since that post as the market wakes up to the Ethereum’s ETFs apparently going live this Tuesday although I am not as bullish for those as I was for Bitcoin’s.

There was a strong institutional demand to buy Bitcoin proven by proxies like Micro Strategy or Tesla earlier in 2020. Those (and the miners) were the only way to invest in Bitcoin. I do not know many institutions wanting to invest in Ethereum, and I do not believe any institution wants to invest in crypto other than Bitcoin.

More important is the selling pressure that will come from Grayscale once those ETFs are live, exactly like with Bitcoin some months ago. The fund owns a bit less than 3,000,000 ETH and their owners will likely get rid of those to buy them elsewhere - or to cash their gains, as soon as they can.

It’s hard for me to imagine anything comparable to Bitcoin’s net inflows but it is possible that this new brings optimism & volume back to crypto and that some players deverse some liquidity on other names than the two big ones - Solana comes to mind. Hard to imagine how it will play out short-term, although I don’t have much doubts about how bullish this is for the long term.

Match Group, Starbucks & The Activists.

Match Gr. This is the second time we've heard that Tinder’s home will be saved from mismanagement by an activist group. The first time was with Elliott, and now it's Starboard, which has apparently acquired 6.5% of the company over the last few weeks.

It’s hard to know what Match Gr. needs to make a comeback, but the new gave the stock a solid pump, up more than 10% after forming a potential bottom slightly under $30 in recent weeks.

Starbucks. Match isn’t the only company under assault, as Starbucks’ stock is also being bought in big chunks by Elliott, again. These are only rumors for now but it wouldn’t be surprising if true. Starbucks has always struggled to maintain its glory without Howard Schultz at its top management, and his return as interim CEO in recent years wasn’t enough.

I’m still not convinced about Starbucks at today’s valuation. The company has seen little growth over the past year and lacks plans to revive it. Meanwhile, its balance sheet is at -$17.5B net debt and only $3.6B of FCF for FY-23. Buying right now would be buying the hope that the ship can turn around. It can, but buying hope isn’t enough.

Both companies have concrete and valuable assets but they need to use them properly, and an activist is probably their best shot at doing so. Time will tell, but I’ll keep a close eye on both over the next quarters, they might become great opportunities.

Amazon Prime Day.

I am still overly bullish on Amazon for every reason someone could have. The business, the financials, the price action... But it’s always nice to have confirmations and we had another one this week with a record-breaking Amazon Prime Day - the company’s sales reached $14.2B in two days, up 11% YoY.

88% of Prime users participated in the event - useless to note that this is a huge number. BNPL was used for 7.6% of purchases, which is not as much as I thought, to be honest. There are lots more statistics but I won’t go over them all. We can summarize the event as a huge success, which will certainly create more and more demand for Prime.

Crowdstrik & Microsoft break the world.

The end of the week was all about blue screens (in the U.S. at least) as many institutions, public services, companies, and basically anything relying on Windows saw their computers unable to start, blocked on the infamous blue screen.

It’s pretty hard to evaluate the damages as airports couldn’t use any digital tools, hospitals had to rely on their pens again and tons of the banking system were offline. Complete chaos, because of a small tiny human mistake.

Crowdstrike is a cybersecurity company selling different cyber protection services to many top IT companies in the world. As part of their job, they released an upgrade this Friday to their clients, including Microsoft. That upgrade conflicted with Microsoft's OS, freezing all computers using it.

Good thing Microsoft isn’t much used around the world, eh?

Consequences. The market has punished both companies harshly - Crowstrike more, but let’s talk a bit more about this event.

This mistake will have consequences. Every cyber company has SLAs to restore malfunctioning services in a defined timeframe, depending on criticality, etc. They sure failed to do so and will be penalized for it, financially.

Image one of the most important things for a cybersecurity company but in this case, the issue wasn’t an attack or a software bug; it was a human mistake. My personal take is that reputations aren’t ruined because of human mistakes. It should not happen at this level, but it won’t ruin Crowdstrike and probably not even hurt them much.

Switching costs for these softwares are just too high and I seriously doubt any companies already working with them will engage in the process of removing their software and finding another provider over a human mistake - as those can happen with anyone. Although this could (and surely will) push potential new clients to turn elsewhere.

Very hard to imagine the consequences already but Crowdstrike still proposes some of the most advanced cyber softwares and even if the headlines and the market are certainly not done hurting the stock, everything will certainly be forgotten in a few months or a year and the company will continue to grow as if nothing happened. To be monitored over the next months, might be buying in if the market punishees the stock too much.

On Running, Lululemon & Celsius valuation.

I have been running some valuations this weekend to review my buying prices for some stocks and have tried a new way to do so, a way which makes more sense to me.

A stock price is always reported to its multiples (PER, P/S & otehrs). Its earnings multiplied by X will give its capitalization, hence its stock price. Those multiples are nothing but the will of the market to pay for the business at a certain moment and can go very high or very low for no apparent reasons. In short: They are impossible to anticipate.

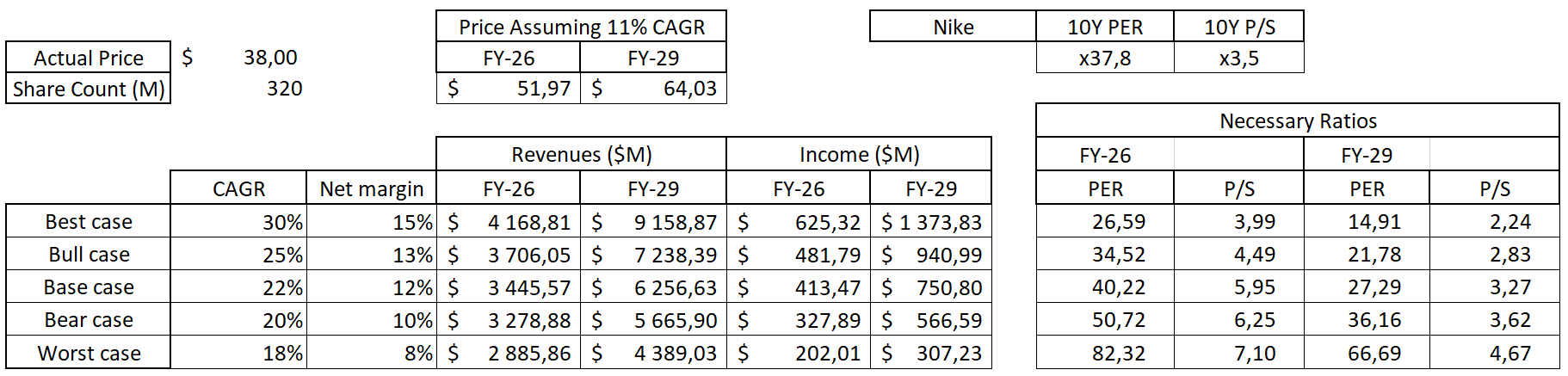

So I tried to take the problem backward and start from the return I expect, which is at least 11% per year as the goal is to beat the market with the SPY as a benchmark - which returns 11% per year.

Knowing the returns we’re looking for and our timeframe, we can deduce the necessary stock price to achieve our returns. From there, excel computes the minimum ratios necessary to reach that price, considering a pre-defined growth & margin - which strangely are “easier” to estimate than the market’s reaction.

It is like asking “Are the minimum ratios necessary reasonable for this stock assuming this timeframe, returns, growth & margins?”

On Running. I pay attention to people’s shoes for some time now and have seen so many feet dressed by On Running over the last months. In the streets, the gym but also on TV with Anthony Noto in an interview on CNN, Zendaya who I see everywhere, and in the movie Challengers (where she plays the main character), where the last 10 minutes of the movie are nothing but a publicity.

It was time to check the numbers and try to find a fair price because I definitely need more shares - much more.

It seems like a lot of information but it’s pretty easy to read, I’ll use the same format for all valuations below.

If I were to invest in On Running up to 2026, I would look at the bull case and accept that the company can grow 25% CAGR with a net margin at least at 13%. If so, I would need a PER at x35 or a P/S at x4.49 to secure 11% CAGR on my investment - stronger ratios would result in stronger returns.

Does that seem unreasonable considering Nike’s medium ratios over the past decade, for example? I personally think not, and those calculations are done at today’s price around $38. Lower the price, lower the required ratios. Every case, except the worst one, is pretty compelling if you extend your timeframe to 2029.

Those projections are still only this: projections. Nothing’s granted and tons of things can happen but it gives an idea.

Lululemon. I did the same for Lulu and reached comparable conclusions, although it is harder to find a perfect comparison for its ratios.

Yet, at today’s price, you’d need a x25.82 PER to reach 11% CAGR at the end of 2026 - this model does not account for share buyback programs, the calculations for 2026 are done with today’s share count, which of course won’t be the case for Lululemon. So we’d need a lower PER than what’s presented here to reach 11%.

Celsius. The controversial who finally broke the $50 mark this week. I got out of my position in the high $50s last week as the short-term momentum is terrible for the energy drink company and I wanted to avoid more loss. But the numbers start to be really, really interesting under $50.

It’s hard to imagine Celsius growing less than 20% CAGR over the next three years at least with the expansion going on and the company still ramping up in the U.S., just as it’s hard to imagine the company reaching 20% of net margin by 2026, but the in-between scenarios seem plausible.

And if we are to assume that Celsius deserves ratios equal to Monster’s… well, the only unfitting case for 2026 is the worst case and all assumptions are interesting if we are to extend our timeframe to 2029 - again, this model doesn’t take buybacks into account while Celsius will very certainly do lots of them by 2029.

ASML, Taiwan Semiconductors, Netflix & Banks Earnings.

We finally started the earning season this week but nothing stood out.

Banks. U.S. banks all released good to great numbers and gave some interesting comments on the consumer.

“The economic environment is very strong and stronger than anyone would have thought given the tightness of monetary conditions. Still, you are seeing slightly higher unemployment and moderating GDP growth… so it's not entirely surprising that you're seeing a tiny bit of weakness in some pockets of spend.”

“... While we continue to see an overall resilient U.S. consumer, we all see divergence in performance and behavior across FICO scores and income bands.”

“We feel good about where the U.S. consumer is. We’d like to see organic spending growth a bit higher, but this is a slower growth economy… the US consumer has been pretty consistent and we think it's going to be pretty consistent throughout the year… we also feel good about international growth right now...”

“We continue to see a cautious consumer, evidenced by less card member spend with lower income households being most affected.”

Quotes come from different banks and all seem to agree that, while global consumer is still strong, we start to see some population spending slowing down.

If you missed other earnings, links are below.

TSM & ASML. The stock market didn’t reward those two companies as it should have for both of them were good - TSM was even excellent.

Netflix. Netflix gave satisfaction without specifically shining.

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!