Weekly Recap | October - W4

Option Portfolio Performance & Positions, The AI Bubble, Compute Optimization & Oversizing, Adobe Foundry, Avride Funding, Google the AI King, ChatGPT Atlas, Weekly Planning & More.

If you guys are interested by a 15% reduction on all FiscalAI subscription plans, click the link below!

https://fiscal.ai/?via=wealthyreadings

FiscalAI is the tool I use on my write-ups for any KPIs and honestly the best platform on the market to follow companies’ fundamentals. If interested, feel free to use my link!

Weekly Buying List Update.

Here is my watchlist & buying plan. Reaching those prices does not mean I always pull the trigger; those are only my view of valuation & price action today. I only pull the triggers on the ones I believe to be the best liquidity attribution at the moment - purchases are shared on my Savvy B&H portfolio.

https://savvytrader.com/wealthyreadingspro/buyandhodl

Optimized Cost Basis (OCB) - optimum average price for a long term position.

Accumulation Target - buying target based on price action, to average up.

Rating - Buy < 3.5 < Hold < 7 < Trim.

“(Slow) DCA” - trading at proper conditions to open a position or accumulate.

Bold - updates compared to last week.

Green - trading at accumulation target.

We’ve had lots of opportunities this week, notably Nebius hitind double digits and I hope some of you did take it - on Nebius or other names.

Macro & Market.

The U.S. government remains in shutdown - the second longest in history, driven by disagreements over budget allocation - mostly healthcare and foreign aid. This hasn’t spooked the markets yet, but the resolution terms will be important for key metrics like consumption and such.

CPI came in lower than expected at 3%, with the added “good news” that no further CPI data will be released this year due to the shutdown. Markets can now only focus on AI infrastructure and earnings narratives - exactly what we want. As I shared months ago: we’re reaching the perfect conditions to fuel that bubble.

We hit a new all-time high Friday after early-week panic. We’re still in a Trump/news driven market, where sentiment can shift in seconds. It’s getting harder to be bearish into the next few months given the setup, but we should continue to expect volatility, especially this week with lots of catalysts.

FOMC on Wednesday. Likely another rate cut. Labor market is softening and we had many more layoffs this week.

Trump/Xi Summit (Thursday): A double edged sword. My portfolio is hedged with Energy Fuels exposure against my China longs. Both countries have reached preliminary agreements on many topics, leaving it up to Xi and Trump to finish it off - based on some rumors this sunday.

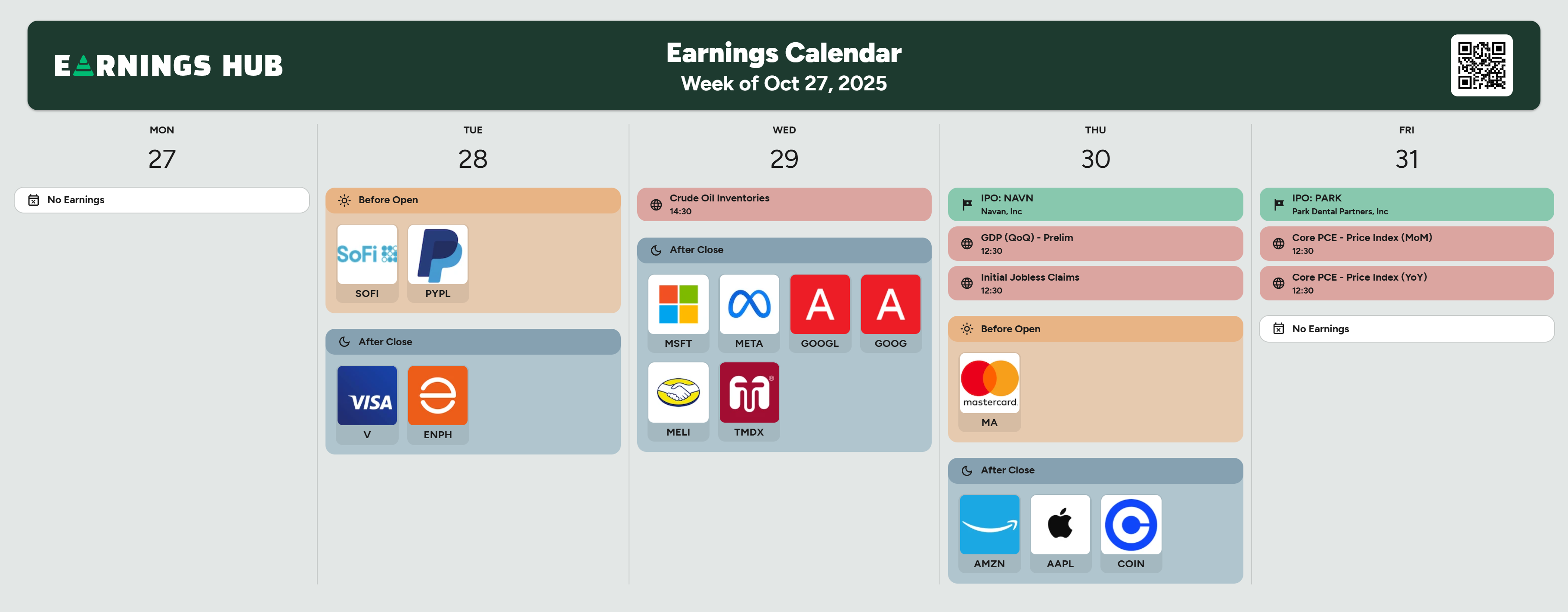

Earnings Super Week: Amazon, Microsoft, Meta, Google, Apple, all reporting. All signals point to strong numbers, but CapEx indications and AI infrastructures comments will be important - especially from Microsoft.

I’d expect most of those to end up in good news, but I wouldn’t try to play the hero with short term earning trades here. Things can change very fast from non-fundamental news, but I remain extremely bullish short term.

Longer term? We are clearly seeing some smoke. Can’t say how big is the fire or if it will grow, but it exists.

Watched Stocks and Portfolio.

Lots happened this week.

The AI bubble 3.0.

If you haven’t read the last three weekly reports, go back, they’ll set the stage.

Bottom line being: AI infrastructure is expanding fast, funded by aggressive leverage against future cash flows no one can forecast - they might never even exist.

And we had even more this week:

Oracle announced a $38B debt-financed buildout for two new datacenters to rent compute to… OpenAI, as usual.

Banks and private credit firms have been competing to underwrite debt deals supporting the development of large data centers. These types of properties are being built to house the technology needed to train and deploy the world’s most powerful AI models.

And the structure of those deals is not really encouraging anymore; while it used to be financed by cash or equity few weeks ago, we are talking abour high interest rates now - probably above 6%.

Preliminary pricing for the debt package is being discussed at about 2.5 percentage points above the US benchmark, the people said. The banks plan to eventually distribute the debt to traditional loan investors and private credit funds, they added.

Meta secured $27B from Blue Owl Capital via debt for its Hyperion datacenters, with

I personally see a big difference between Meta and OpenAI as Meta has cash flow, growing from a trusted business. OpenAI does not. Yet both are levering up on the assumption of future demand.

This is a new step in the AI datacenters build out. I’m not as bearish as some - future cash flows might be enough to justify this debt. The truth is that we don’t know yet. But there is a clear lack of “risk assessment” at the moment, from all parties, and the industry is highly interconnected by now. One failure would ripple across the entire AI sector and all its companies - success too.

OpenAI ChatGPT Atlas.

OpenAI launched its AI browser, Atlas, few days after Perplexity opened Comet.

I personally don’t see the value after days on Comet. The more important question is: how will they monetize? Ads require a full redesign to generate clicks in these environments. Subscription models may be the only viable path.

Which means… We circle back to the central question: where does OpenAI’s cash flow come from?

PayPal & LLMs e-com.

Regardless of AI’s business model, AI will reshape how consumers search, shop, and make purchase decisions online. The winners are those who adapt to it.

And PayPal already has services for it, with more to come.

Google, The Real AI Kings.

Ahead of earnings, Google dropped major news: Anthropic will rent Google TPUs - its proprietary chips competing directly with Nvidia.

Google isn’t just renting compute. It’s renting vertically integrated compute on its own hardware, and apparently efficiently enough so Claude’s home company wants to rent it.

Google is the AI king which the market was selling for nothing a few months ago.

Nebius & Alibaba’s Compute Optimisation.

Two big developments this week highlight a critical truth: the real AI bottleneck is not a lack of GPUs, but a lack of optimisation.

Alibaba released a technology improving GPU cluster efficiency by up to 82%, fully open sourced.

Nebius published a review showing how optimizing inter-rack efficiency drastically increases compute output without additional hardware.

Translation: In a few years, if we focus on optimisation, we could reach multiple times more compute capacities on already existing datacenters, rendering today’s overbuild potentially obsolete.

Those datacenters expansions are an accepted risk taken by companies as we don’t know if we can optimise compute, to what extend and when. It is therefore faster to oversize and see what happens.

Short term: market remains optimistic, which is what matters for us. But the risks are undeniably rising as while we do so, others focus on optimizing compute.

Avride Funding.

Nebius and Uber invested in Avride, Nebius’ autonomous systems subsidiary.

No information on the deal structure except for this comment.

The spokesperson said the deal is structured as a convertible note, under which Uber will have the option to convert its investment into equity at a future date. Avride will remain a wholly owned subsidiary of Nebius, the spokesperson added.

This increases Avride’s implied valuation and will help them expand. I still think this subsidiary remains massively undervalued by the market.

Adobe Foundry.

I’ve been very vocal on Adobe lately as price action is stabilizing, fundamentals are intact and the market continues to underestimate its adaptability.

Even more after they announced Foundry, a fully AI-enhanced creative platform built for large brands to train AI models with their data to generate marketing campaigns.

The market believes newcomers can compete with giants. They can’t… Adobe has the resources, the data, the clients, the talents, the products… They will not let disruption happen to them. They will lead it.

They know their clients and their needs. And they will meet those.

Option Portfolio & Returns.

Rapid review of the option portfolio before we enter an important week for me.

At Friday’s close, I was up 120.6% YTD and 362.45% since Jan-24, when I started sharing my trades transparently.

Small reminder that TWR performance doesn’t include cash injections. The portfolio reached a new ATH in dollar value on Friday.

Here are my positions and the pending returns on each, at Friday’s close.

Not much changed since I discussed it last time.

Nebius calls: Long-term conviction. Will convert to shares at expiration unless we’re clearly in bubble mode.

Transmedics & PayPal: Both long-term conviction plays. Market is finally waking up on the first - I was too early and should have done better in term of timing, and will on the second - in time.

JD and KWEB are long term plays as I believe China will stimulate consumption but the short term is uncertain.

Energy Fuels is a China edge to some extend; if this week’s meeting does not go well, UUUU will compensate for my Chinese positions. We have rumors that both countries’ found a preliminary consensus on rare earth export controls; potentially bad news but I would wait for confirmations, lots can still happen in a few days. Plus, even a deal on rare earth won’t change the fact that the U.S. need an independant supply chain.

Those three positions go together, which is why I am confident on my book, whatever happens this week.

I also shared a trade on Halliburton I didn’t take. shared are up 9.2% since and the trade I proposed would be up 10.1% due to new sanctions from the U.S. on Russia which gave a bounce to oil and its entire sector.

Weekly Planning.

This is one of the most important weeks of the earnings season for me. Transmedics and PayPal will report - a detailed review for both 24h after their release, plus review on MercadoLibre, Google and Meta when I can as they all report on the same day.

I’ll keep an eye on Microsoft’s comments on AI infrastructures; have answers on why renting compute and not building, and on other hyperscallers’ CapEx comments.

Other names are for information, V and Mastercard for consumer, Amazon & Apple because they are key markets’ movers, Coinbase for risk appetite. Enphase is giving some signs of bottom which could also be interesting.