Various Q3-24 Earnings

Shopify, Spotify, Cava, D-Local, Disney & JD.com.

Some quarters from companies I follow out of interest or for their potential but won't really dive into - for now. I know these can interest many here, so I still give my opinion on their earnings.

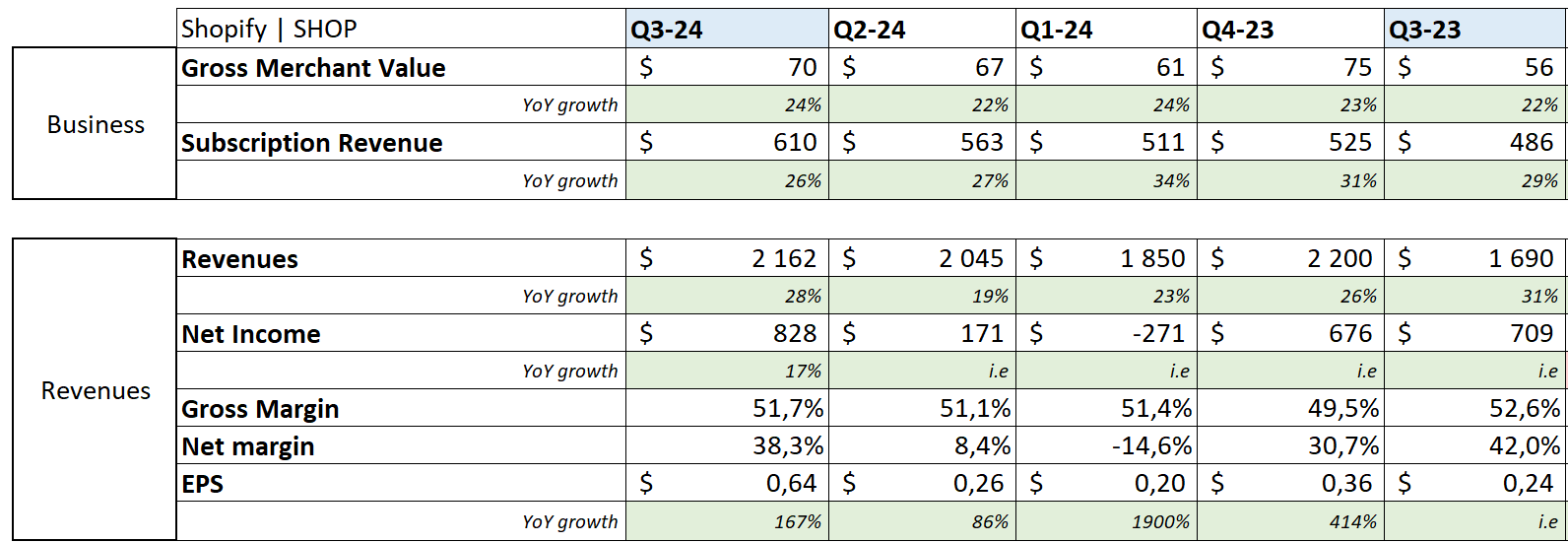

Shopify.

The e-commerce SaaS continues to impress with another pretty strong quarter.

EPS. $0.27 | $0.35 | +29.63% beat

Revenue. $2.11B | $2.16B | +2.46% beat

There isn’t much to say. Strong demand for their products combined with a strong retention equals growing market shares, in a very competitive market. Its products scale together & with their clients, with Shopify Pay now treating 42% of total GMV only a few years after deployment.

Growth remains stable although we can see some bumps. Growing expenses are responsible for a lower net margin this quarter - notably due to marketing but again, with a very bumpy history and overall expanding margins. Ending the quarter with $3.7B of net debt, $421M of FCF & a negligible YoY dilution under 1%.

A beast, no reasons to sell this in my opinion.

Spotify.

I still cannot understand this one but it is performing really well this year.

EPS. $1.84 | $1.59 -13.59% miss

Revenue. $4.31B | $4.38B | +1.69% beat

User growth is very stable and even if we could argue about a potential slower growth, it's too early to say & comps are getting harder & harder. I am a YouTube subscriber and cannot understand Spotify's added value but the company is healthy and shareholders make some bucks, so it’s all good.

Revenue growth is stable & the company is still optimizing, growing margins healthily. Balance sheet is growing with $4.3B of net debt & $530M of FCF this quarter, with a strong dilution around 2.8% YoY.

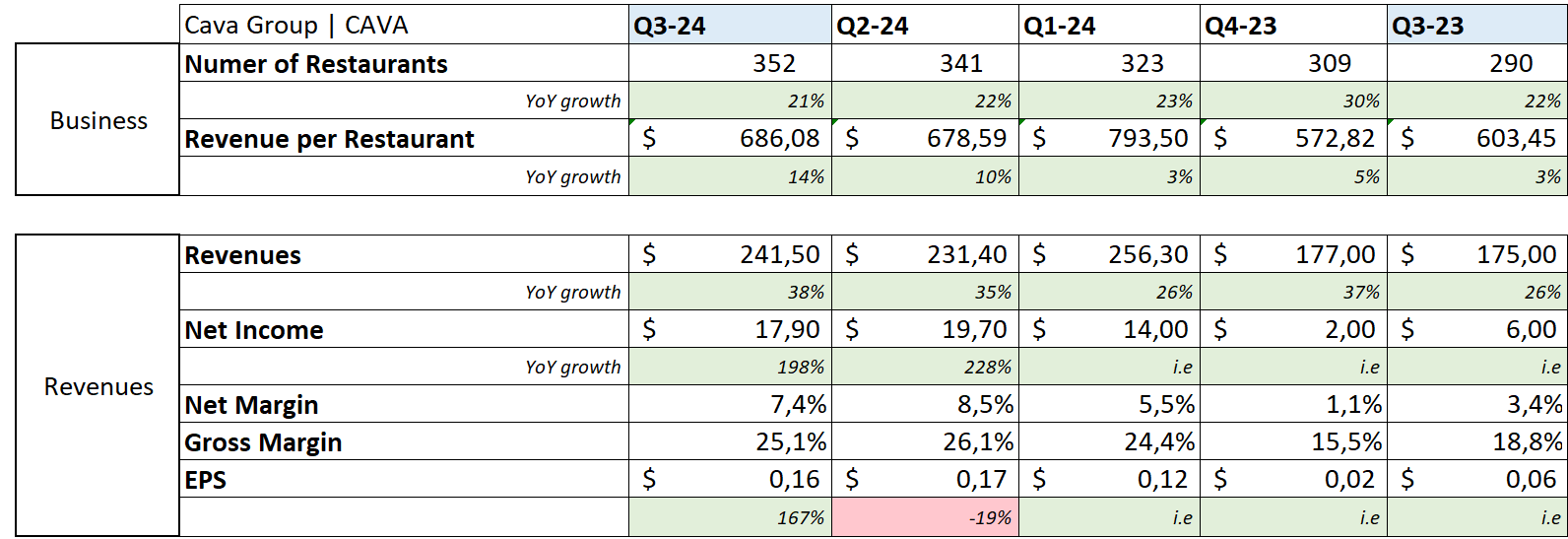

Cava.

The Mediterranean restaurant chain continues on its path of excellence.

Revenue. $233.59M | $243.82M | +4.38%

EPS. $0.11 | $0.15 | +36.36%

The most important metric remains a rapidly growing traffic & same-restaurant sales growth, up +12.9% & +18.1% respectively. Their brand keeps attracting more & more their new locations will certainly accelerate the snowball.

Financials are equally impressive with revenue growth acceleration & margins expansion YoY as the company focuses on execution. There's nothing more to say, everything is very bullish in this report and it becomes usual for Cava. Valuation is ridiculous by now but that is how the market rewards excellent growth.

I'm sadly not in but I would hold strong on those shares. Although the music will stop like for every growth story one day, and the market will be violent when it happens. Only question is when?

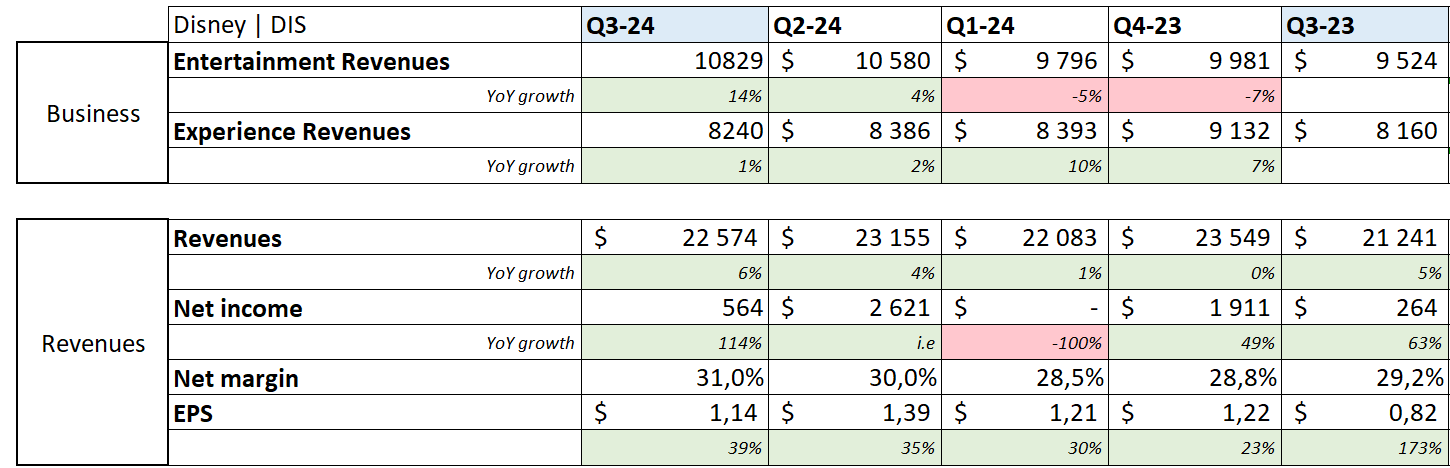

Disney.

I've not been the best supporter of Disney lately, although I'm still watching all their movies. My bear case was that an entertainment company had to rely on the quality of its movies to sustain itself, and that wasn't the case anymore. Things might be turning around.

EPS. $1.10 | $1.14 | +3.64% beat

Revenue. $22.35B | $22.57B | +1.00% beat

The data which matters to me is to see a growing entertainment branch and that happens with great content. Last releases help with strong box office like Inside Out & Deadpool 3, and I gotta admit they have a strong pipeline coming with Moana 2, another Lilo & Stitch, Mufasa & more movies which could be great. The parks are now stable after coming out from the covid lockdowns.

The financials are what they are for a company this size, operating & maintaining some of the biggest attraction parks of the world. We see growth coming back, although comps are made easier with a terrible 2023. The company closes the quarter with $8.56B of TTM FCF & -$34B of net debt.

It isn't the kind of companies I like to buy so I am not in nor planning to buy, but if I were I'd be holding as things might continue to improve.

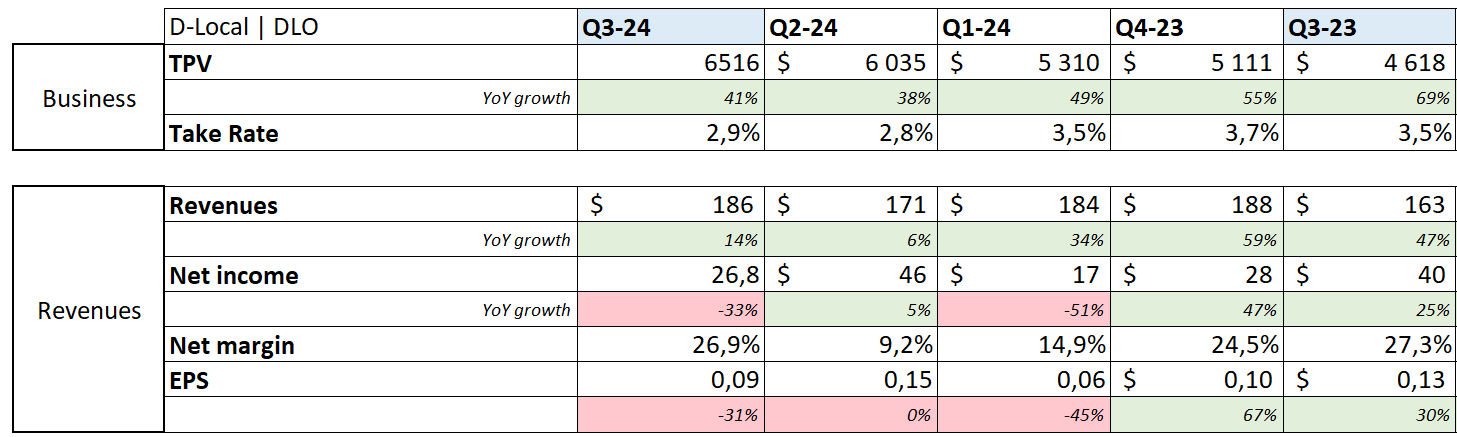

D-Local.

The emergent markets payment processor.

Business is globally going well with a growing TPV and despite a declining take rate which is explained as the company is present in different markets, currency & sectors and while it expends, take rates will fluctuate depending on revenues’ proportions.

Revenue growth is good but there is an issue on gross margins as costs grow faster. It's early and the company focuses on its market share for now, but it's not a good trend & hurts profitability.

DLO remains a very interesting company which has a place & should be monitored for anyone who believes, like me, that emergent countries - mostly Latam in this case, will get richer and spend more.

JD.com.

The Chinese e-commerce gave a pretty strong quarter which was of course not rewarded by the market as nothing Chinese sees green lately.

EPS. $1.09 | $1.24 | +13.76%

Revenue. $36.54B | $37.11B | +1.55%

$390M of buybacks this quarter | $3.6B nine months ending, with a new $5B re-purchase plan for the next 36 months.

It's hard to talk about growth acceleration yet but there sure is an uptick happening before the strongest retail season, while the logistics sector is growing its margins, which shows in both global gross & net margins expansion.

The argument to buy Chinese stock is always the same: there are no doubts that those companies are undervalued but as long as China isn't attractive, be it for trust issues or because liquidity is better elsewhere, those stocks won't see any green days. It's all about opportunity costs.