Various Q3-24 Earnings

Duolingo, Match Group & Arista.

More quarters from companies I follow out of interest or for their potential but won’t really dive into - for now. I know these can interest many here, so I’ll still give my opinion on their earnings.

Duolingo.

The howl keeps showing how it’s done, how to hook users to your platform, how to keep them & how to make they spend, while it is all beneficial for them.

Revenue. $189.07M | $192.59M | +1.86% beat

EPS. $0.35 | $0.49 | +40.00% beat

I odn’t think there’s any need to talk about it for hours. The platform continues to attract without any significant sign of slowdown this year and even if paid subscribers growth passed under 50%, it is simply due to harder & harder comps.

About the financials, growth remains constant & profitability is growing as the company now can focus on its internal optimization while its business itself is stable with constant gross margins. Finishing the quarter with $826M of net debt & $52M of FCF with a strong shares dillution though, around 5% per year.

And I wouldn’t even call Duolingo expensive at today’s price assuming it can keep its growth pace at least over the next two years. It still is very hard to know how the market would react with growth stocks so I wouldn’t be a buyer right now but I wouldn’t be surprised if the up trend were to keep going.

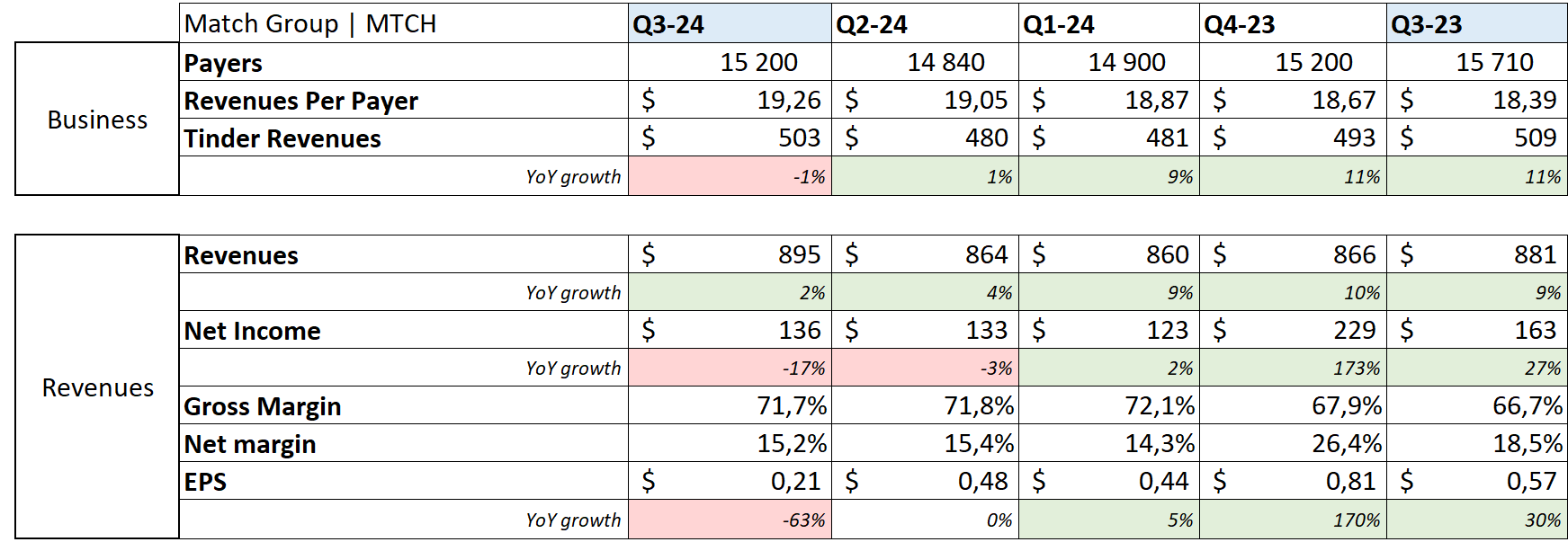

Match Group.

The story is a bit different when we look at Tinder’s home.

Revenue. $900.87M | $895.48M -0.60% miss

EPS. $0.48 | $0.51 | +6.25% beat

The global overlook show a decline in users with raising ARPPs which doesn’t seem like a good combo. Detailing a bit the business, it seems like the only dating app doing healthy is Hinge while the rest of the portfolio is losing users.

And it shows in revenues & margins as Hinge is a lower margin app than Tinder. Gross margins are still up YoY due to a constant business but expenses are growing rapidely while they are still losing users, hence a potential innefective marketing.

I keep following the company because Tinder is a hell of an IP but it might have passed its time by now. No reasons to have any cents tight to this stock at the moment.

Arista Network.

Back to excellence with the top network hardware company, boosted by the surge of AI and an increasing demand for performant infrastructure hardware.

Revenue. $1.74B | $1.81B | +4.08% beat

EPS. $2.08 | $2.40 | +15.38% beat

Business is as good as usual as demand continues to fly in from any company trying to build AI & Clouds infrastructure. Arista products are top class.

We’re seeing a constant growth and management hints that this demand isn’t slowing and shouldn’t slow over the short term, a tendancy confirmed by other companies from TSM to other tech hardware ones. Margins are also slowly but constantly expanding, following demand & optimization.

The only problem with most of those companies is firstly the ciclicality & secondly the actual valuation. I wouldn’t call Arista crazily expensive but I wouldn’t push my average too high, probably not above $300/$320. I’d be a buyer if I could afford, a holder otherwise.