Transmedics | Q4-24 Earning & Call

Finally some clarity.

If you do not know about TransMedics, you’ll find everything you need here.

Overview.

Expectations were low but let’s not take away credit from the team, they really did good.

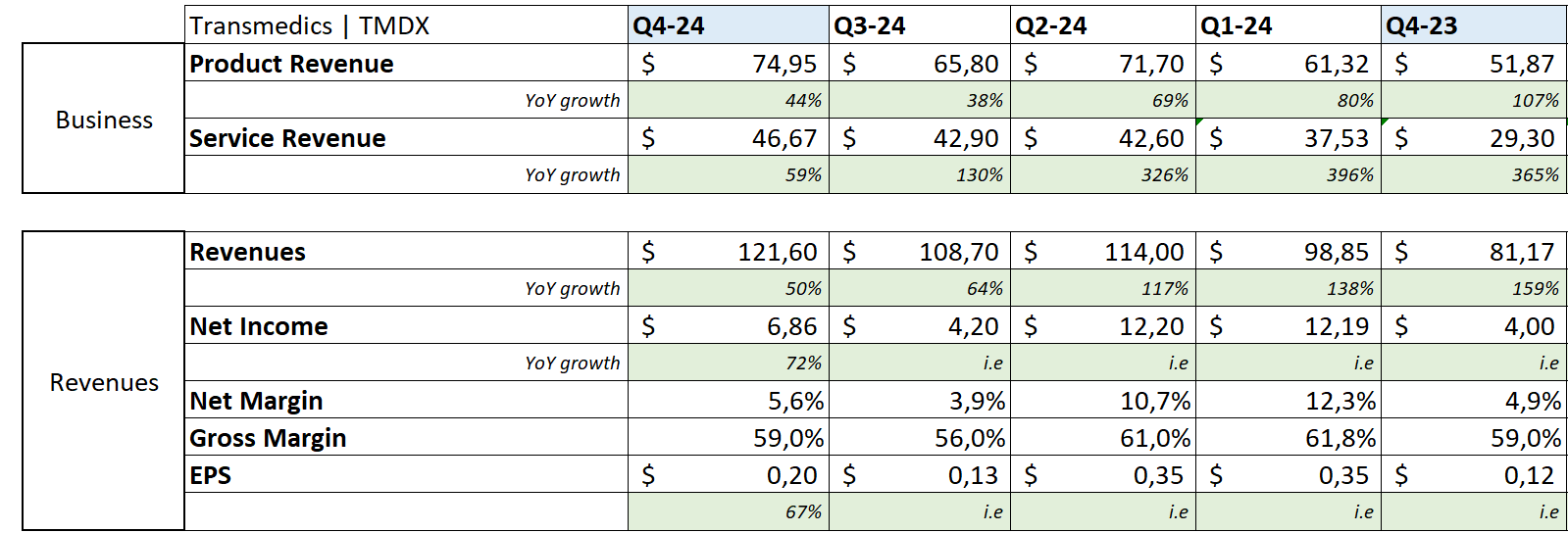

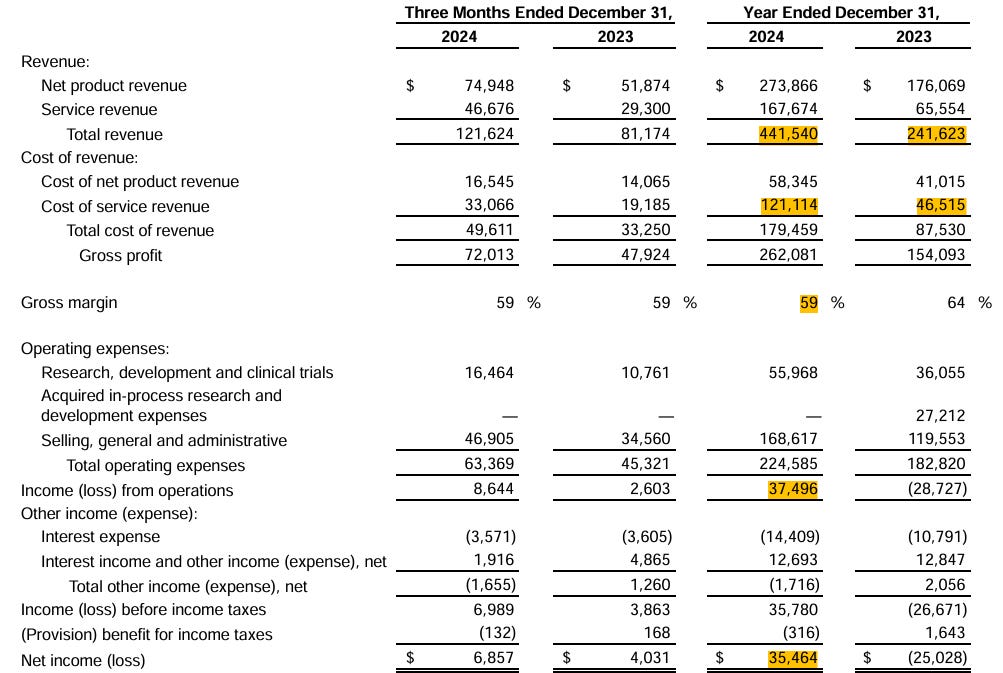

Revenue. $110.29M | $121.62M | +10.28% beat

EPS. $0.16 | $0.19 | +18.75% beat

We now know what to expect.

Business.

Lot happened to TransMedics since their last quarter, mostly negative… Growth slowed & lots of concerns were raised by the Scorpion report, some not interesting – most of their arguments really, but some valid concerns about growth, market shares, safety or pricing. We finally have answers today.

The bull case remains the same. They are working on disrupting the transplant industry with their end-to-end service and their OCS hardware. Every data pointing towards that disruption happening is a positive so I’ll look closely at market shares, growth in terms of volume - not only revenues & other metrics pointing towards a growing demand for the service & hardware.

And to be fair, this quarter gave satisfaction starting by the fact that growth did come from a groing usage of the end-to-end service with their service business up 156% YoY.

“Growth was led by liver revenue, which grew 103.4%, while heart and lung also delivered strong growth at 50.3 & 49.6%, respectively.”

Service revenues grew 59% YoY & 8.7% seequentially, the acquisition of their aircrafts this year allowed them to grow their capacity to deliver. They are now reaching their end goal of 22 aircraft – ending the year at 21 with the objective to buy one more through FY25.

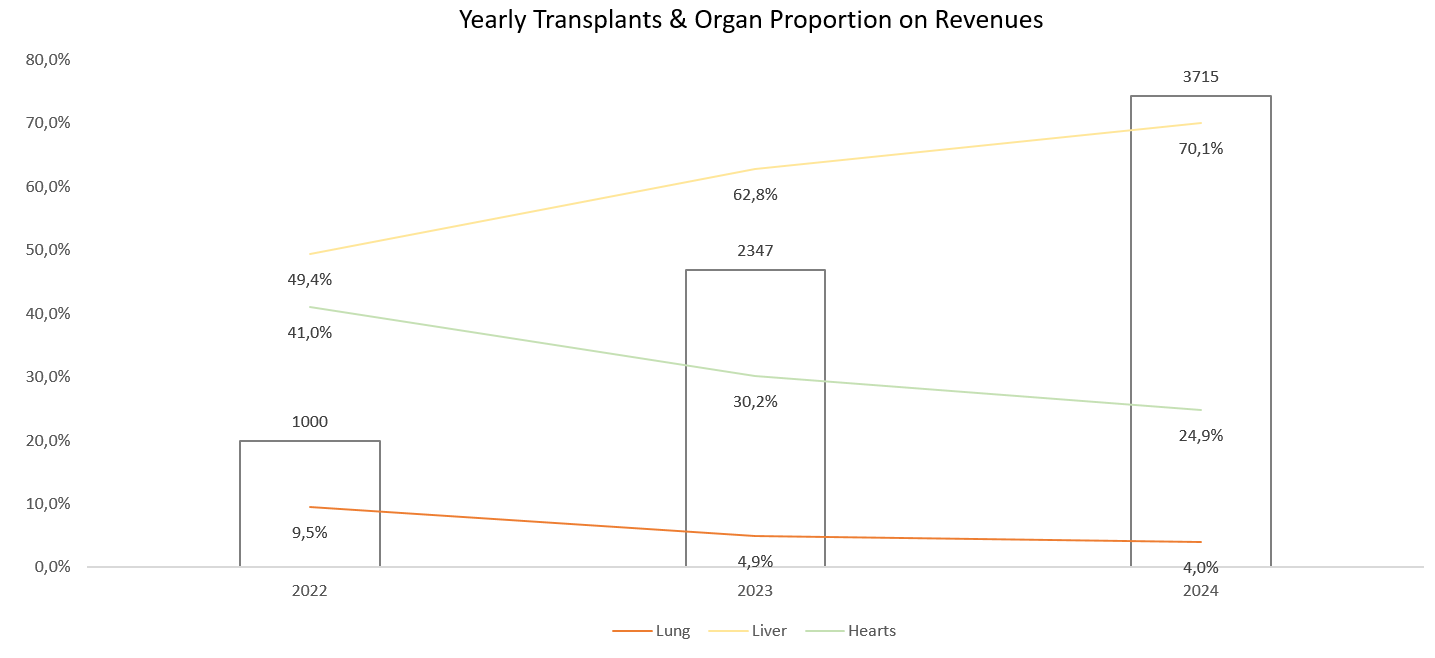

About the procedures themselves, TransMedics realized 3,715 transplants this year with the OCS, up 58.2% from 2,347 last year, which is a pretty strong growth, confirming they can reach their target of 10,000 yearly transplants by FY28.

We had a great question from an analyst who estimated that continuing on their current trajectory, they’d reach 9,000 or so yearly transplants by 2028. Question was, where will they find the missing delta? Management believes that heart & lungs will grow faster once the new OCS are tested & results give reinssurance to practicioners, and that this should be enough.

“We are bullish on these two programs and that how we not only fill in the gap of those 700 or 800 additional organs, we think we are going to do more than 10,000 transplants into 2028 just from heart, lung and liver alone and not counting any additional organs that might be coming in the pipeline.”

In terms of organs, liver remains the biggest proportion of transplants for the company and is growing in term of market shares, which is exactly what we want to see as it translates a growing usage of OCS, because of its quality.

Chart leaning to the top right is what we want to see. Lungs aren’t growing much but this is due to the OCS hardware which isn’t good enough yet, that is why the company is working on clinical tests to prove its new version is an upgrade, safer & delivering better results.

We’ve talked bout the clinical programs already for their new heart & lungs OCS hardware which should start H2-24.

“Finally, the precise timing of launching the next gen lung and heart clinical programs will depend on several variables, especially FDA ID approval timeline, center IRB approval and center initiation process, etcetera.”

We’re not there yet but this is a long-term play either way so patience is key.

Liver is obviously the biggest portion of revenue & growing as their market share is growing faster than the rest. If anything, it highlights the quality of the product & the opportunity once lungs & hearts new OCS are approved & commercialized.

About their operation, the company is reaching its end goal of owning 22 planes with 21 at the end of the year. They intend to buy the last one to complete the fleet in the next months.

Lots was also said on competition – notably with NRP, while I remain with the same view: there is room for both & both have advantages. NRP remains complicated for long distances & Waleed confirmed that both can work together as NRP will allow the entire body conservation but won’t allow to check or really take care of the organs. Transportation remains complicated in NRP so OCS can take the lead from there. Two different methods, both with their advantages but not mutually exclusive.

“We do NOP liver cases post NRP. NRP is nothing but a surgical procedure to try to convert a DCD donor to a DVD donor, but it's not as simple as that. You still need to preserve the liver. You still need to assess the liver. You still need to protect the liver. So again, as I stated before, we do not see NRP as a threat to our liver DCD franchise. And based on the data, we've actually seen market share increase in the year to 53%.”

About pricing, we had the same answers as always. The product is sure expensive but the end-to-end service is competitive & priced on the value it provides, a value no one else can provide. Waleed concluded with the most valid argument there is.

“The penetration rates and the growth rates speaks for themselves. The market see that value, otherwise they would not have adopted the OCS.”

Revenues.

This is where things were better than expected.

FY24 up 83% YoY with 91% of revenues coming from the U.S. while OUS was flat YoY. It’ll take longer to expand geographically but we’ve seen during the investor days that it was in the pipelines – notably with a NOP in Italy.

Q4 is up 50% YoY & 12% QoQ showing that growth is back sequentially & confirming the management arguments of the last months that seasonality is a thing – and unpredictable.

“The variability in the transplant market, we usually see it in any quarter.”

Gross margins fell from 63.8% to 59.4% YoY as the proportion of revenues coming from their end-to-end service is growing & is a lower margin service. They also were impacted by a bigger inventory than expected as production ramped up this quarter.

The quarter & year are profitable with a FY24 8% net margin.

In terms of cash, we’re talking about $277M of net debt for a positive cash flow with positive OpCF.

Guidance.

The interesting part as management talked about revenues between $530 & $552M FY25 - 20% to 25% growth.

This is exactly what they talked about during the investor day but as the company did beat on FY24 revenues, the flat value in dollars is much higher hence a bigger cash production than the market expected.

We can also factor that management now knows how to be a bit more prudent in their guidance as they only guide full years & the demand & supply on their business is kinda… volatile. They said that this will happen again and do not want to get too cocky - my words here though.

My Take & Valuation.

The quarter was good without being exceptional but most importantly, it gave the market & myself clarity. We now know what we can expect & can work with our different models to value & find our buying prices or targets.

The only question is what ratios do you want to attribute to this business based on its growth & fundamentals, as we do not have any comparison points.

At today’s price & with the low end of their guidance - which should continue up to FY26 with the new OCS starting to be commercialised then, we’d need the stock to trade above 6x sales, which seems pretty ok when you compare it to the medical equipment sector.

Add to this the fundamentals which do not have equivalents with NOP and potential with hearts & lungs post clinical studies… I’d say 5x to 6x sales is alright as long as we respect the growth assumed here.

I’ve always loved the company and continue to believe it has great potential over the long term. It was all about clarity & buying at the right price so now that we got the first, we’ll need to wait for the second.

No point giving liquidity too early to a stock, let’s wait for the market to tell us what it thinks about it as once again, it’s hard to have any idea of “fair” multiples. As for a fair buying price based on fundamental & my opinion, around & under $75 would be good enough for me.