Tesla | Q4-24 Review & Call

Not pretty, but finally closing a tough year.

I will not go over the hype & optimism - or delusion, depending on if you are bearish or bullish, around the company today. I'll try to remain factual & if you want to understand why owning Tesla is betting on the future & optimism, it's all here.

Overview.

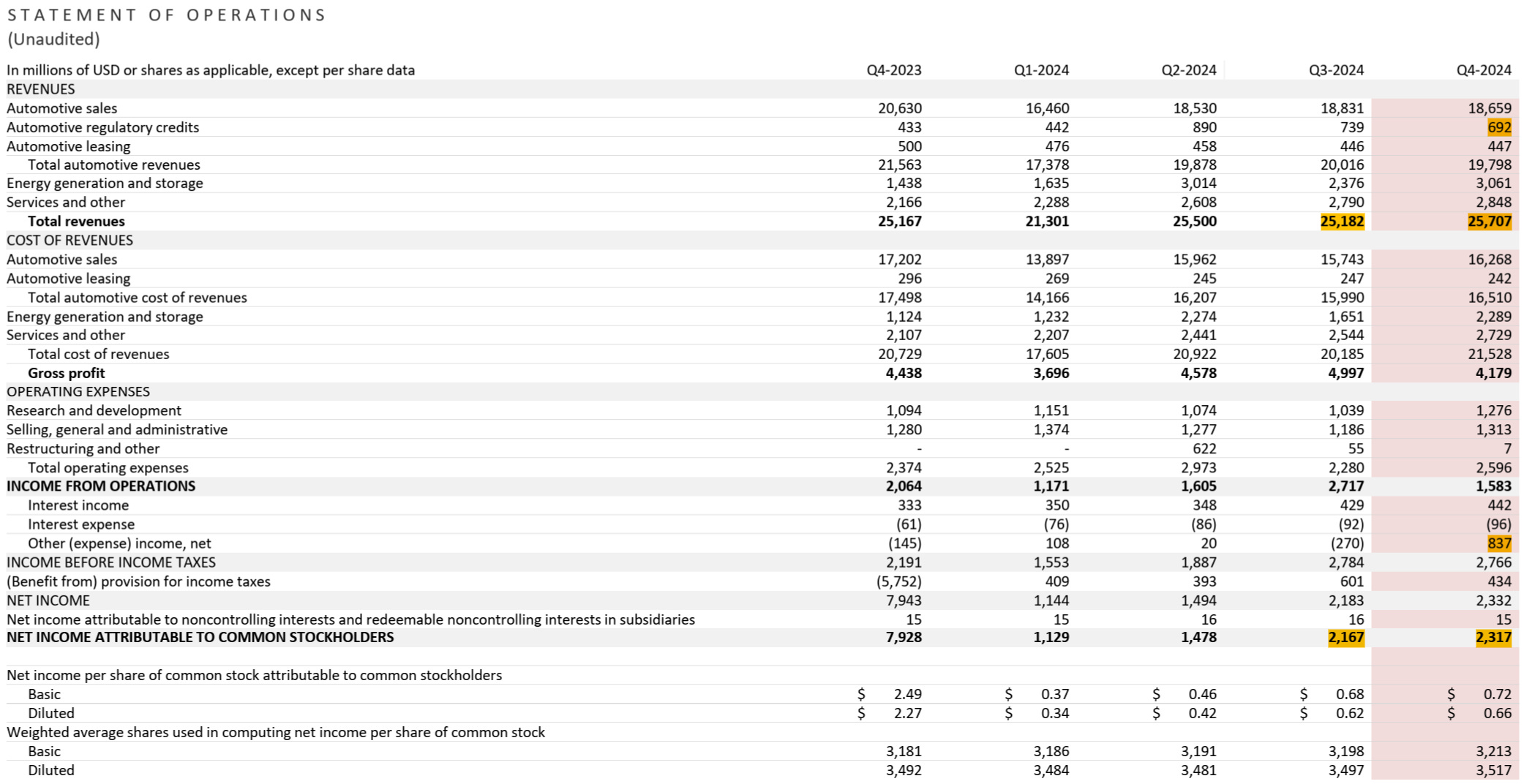

Revenue. $27.14B | $25.71B | -5.28% miss

EPS. $0.77 | $0.73 | -5.19% miss

FY24 will be a year to forget for Tesla.

Business.

As usual, lots of things to say.

EVs.

We are closing the year with a small decline in deliveries, which is not what you want to see for a car manufacturer, even considering the macro. Gotta note that the Model Y remained the most sold car of any kind this year, which is still a pretty great feat considering the refreshed version will be sold in FY25.

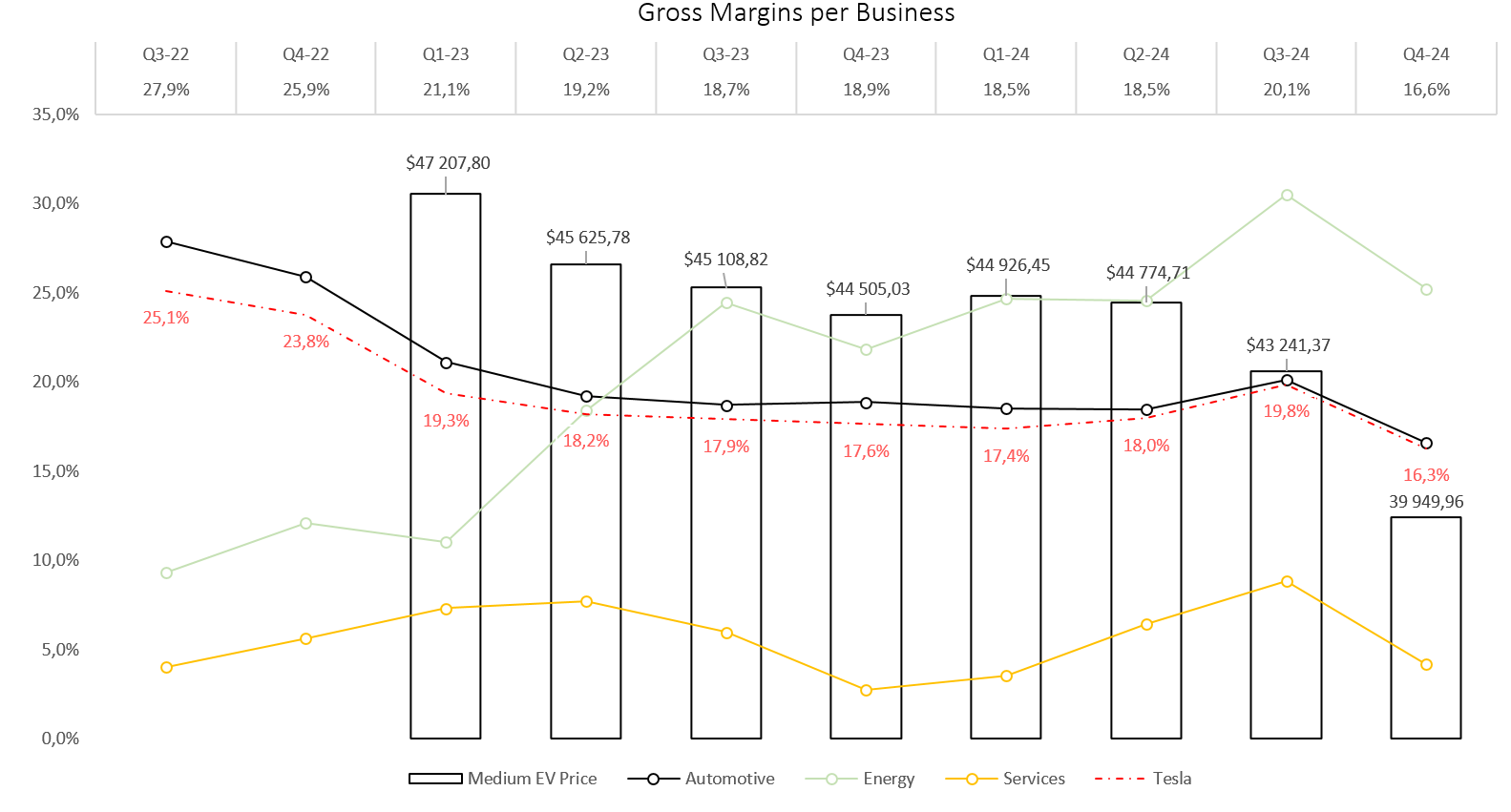

Tesla proposed lots of financing options & discounts this quarter which impacted the median EV price from $43,241 last quarter to $39,950. Less expensive EVs means lower revenues but also lower margins - as we'll see later.

On the other side, Tesla achieved its lowest production cost per car this quarter with an average manufacturing cost around $34,800.

This sure helped a bit the data & is a great achievement long term but it doesn't make this year great for the EV business.

About new models, management said that semis should be ramping up in FY26, more time to wait. Cybercab is also planned for production FY26 & the low-cost model is apparently still planned for the first half of the year without any public news…

“Plans for new vehicles, including more affordable models, remain on track for start of production in the first half of 2025.“

Energy.

Tesla’s light in the dark as the company continues to deliver strong delivery & growth with stable margins, mostly coming from Megapacks & Powerwall which are two very promising products.

The company expects the trend to continue with a 50% YoY growth FY25 or around $15B of revenues which start to be significant as it would represent 15% of FY24 revenues.

FSD.

“And the only people who are skeptical, the only people who are skeptical are those who have not tried it.“

I believe this is very true if you look at the people who discover it for the first time. I'm European so I do not have access to it but I've seen lots of feedbacks from first-time users who were sure, afraid, but really impressed by the software.

As for any product, if you want to convince others you have to convince & use it yourself first. That's what the company is doing.

“We already have Teslas operating autonomously unsupervised full self-driving at our factory in Fremont, and we'll soon be doing that at our factory in Texas.”

That's pretty cool & proves the trust given to their software as it could easily go wrong and destroy many cars.

Although to be entirely honest, it's hard to know without going there every day if it happens all the time or was just the time to shoot a video, I can understand the skepticism.

Nevertheless, things are moving as Tesla expects to launch a first & small FSD fleet - company operated, in Austin to finally test the service in real conditions.

“So, we're going to be launching unsupervised full self-driving as a paid service in Austin in June. So, I talked to the team. We feel confident in being able to do an initial launch of unsupervised, no one in the car, full self-driving in Austin in June.“

And it should continue through the year as Elon talked about releasing unsupervised FSD slowly in all states through 2025. Hard to say how this will unfold as it depends on regulation but I think it can be reasonable to expect it to be available in a few states before 2026.

As for Europe…

“Europe is a layer cake of regulations of bureaucracy […] For example, for us, just to release unsupervised full self-driving in Europe, even though it works really well, we have to go through a mountain of paperwork with the Netherlands, which is our primary regulatory authority. Then the Netherlands presents us to the EU in, I think, May. And there's like this EU country committee. We expect it to be approved at that time. There's nothing we can do to make that may happen sooner.“

And China remains complex as I expected & shared months ago; driving there & driving in the west is really different. They're still working on training but it'll be complicated & longer.

There still are concerns about safety, not that FSD isn't safe enough but that Tesla wants it perfect to avoid bad press - understandably, as it is already hard enough to convince people self-driving exist. Still, last versions are pretty safe.

“Just to the safety aspect, we did publish our vehicle safety report today. And in Q4 was one crash for every 5.9 million miles driven compared to a crash every 700,000 miles without autopilot.“

Last point, licensing - very important one.

“What we're seeing is at this point, significant interest from a number of major car companies about licensing Tesla full self-driving technology.”

Management detailed that they’ll focus on licensing when FSD is perfectly ready so let’s not be too rushy, but this remains a huge part of the bull case around FSD.

Optimus.

Nothing much to share here if I want to remain factual as most comes from optimism - hence the name. One important point to highlight though that is too often forgotten in this robotic war: manufacturing is everything.

“The problem is there's like those who have never been involved in production or manufacturing somehow think that may -- once you come up with some eureka design, that you magically can make 1 million units a year, and this is totally false. There needs to be some -- there's some Hollywood story or where they show actually the problem is manufacturing.“

Tesla’s manufacturing capacities are largely above their competition - probably, who are mostly focused on training & design but not on how to produce them. When this hits the market, they will need to produce millions of it as demand will certainly soar.

Years until it happens. Still an interesting point.

Revenues.

Now let’s hit where it hurts. Financials are bad.

Yearly revenues are up 2% with automotive revenues down -1%, which shows that other branches actually grew pretty well. Although services didn’t move, so it simply means that the energy branch is slowly becoming relevant - with a 29% growth.

The rest is quite straightforward, although I have to say that accountants are out of their minds with how they treat Tesla's Bitcoin:

“It is important to point out that the net income in Q4 was impacted by a $600 million mark-to-market benefit from Bitcoin due to the adoption of a new accounting standard for digital assets.”

This is straightforward ridiculous; gains on assets should not be included in revenues. It boosts net income & indirectly makes EPS and some key metrics look much better than they really are.

The truth is that this year’s financials are bad, with no growth in revenues and higher costs, leading to lower margins, income, and cash generation. Tesla closes the year with $3.6B of FCF & a net debt of $31B, fortress as usual.

Margins.

Before concluding, we need to look at the margins, which aren’t good.

It’s hard to judge on only one quarter as the EV margins are down due to financing options & discounts to maintain volume in a tough economy. Service margins are volatile but remain on an increasing trajectory over the long term, same for the energy sector.

The global margins are brought down because of the EV branch, but this is a trend we want to see revert back to growth going into 2025 as there won’t be the excuse of a tough economy - although that remains to be seen. We had a nice uptick the last three quarters & we need this tendency back.

One tough quarter.

My Take.

Tesla doesn’t give outlooks & is very hard, impossible to value as we cannot quantify the impact of FSD on its EV business while not including this potential would make the valuation useless as the price target would be under $100.

Again. Tesla is about optimism.

And 2024 helped ont that with some great advancements with FSD getting better & unsupervised FSD almost ready to be released for real-world tests & hopefully more this year. The energy branch is ramping up well & management expects growth to be back for the EV branch during the year - which is honestly needed.

But optimism doesn’t make money.

Sure, the stock pumped after Trump’s election, due to optimism for the future, but there comes a time when companies need to deliver, and FY24 wasn’t that year, far from it. We’ll need a much stronger FY25 with EV growth & great margins to have great returns on our shares as high expectations are now priced in.

Closing a tough year. Everything cannot be fireworks & unicorns. That’s fine. But it cannot be that tough two years in a row.