Tesla Q1-25 | Earning & Call

That bad?

I’ll repeat, once more, that Tesla isn’t a rational investment, it is an optimist investment that the future can be autonomous & that Tesla will be the main actor for this transition. I explained this here.

And Elon says it himself, once more.

“The future of the company is fundamentally based on large-scale autonomous cars and large-scale, large volume, vast numbers of autonomous humanoid robots.”

Nothing says they’ll make it. But if the company which does will be one of the most important one on the market. And as of today, Tesla is really the best positionned.

Overview.

But for now, data is really bad.

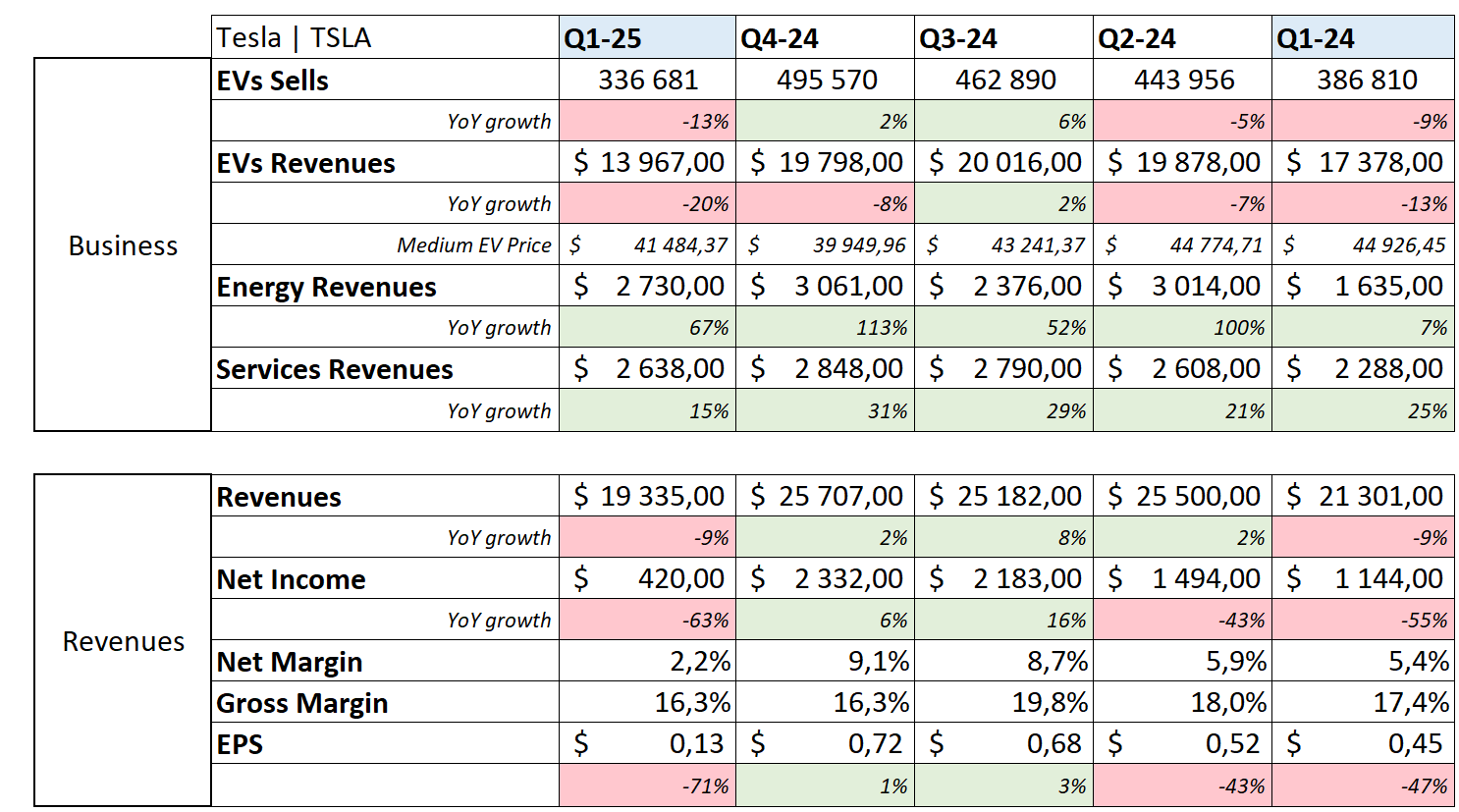

Revenue. $21.34B | $19.34B | -9.40% miss

EPS. $0.41 | $0.27 | -34.15% miss

I personally do not look much at analysts' expectations, but the misses here are brutal, and the fundamentals aren’t good either. Musk sums it up well.

“To summarize, we have near-term challenges in our business due to tariffs and brand image.”

Business.

EVs Branch.

There is no sugarcoating how bad this quarter was in terms of sales. Management shared some potential reasons but it remains hard to be sure of any. Is it a demand problem, a brand problem, a macro issue, or a consumer buying power issue? The truth is probably in between. Let’s go over some of their arguments.

First, seasonality. December & January are historically weak in demand. Management took advantage of it to modify their Giga’s production lines, to prepare them for the new Model Y & others models. Which brings us to the second reason.

Reduced production. As the lines were being modified, Tesla couldn’t produce as much as they wanted.

“We had previously guided that we will be updating all factories and this will lead to several weeks of lost production, which did happen as planned. The ripple effect of the change is not having enough new Model Y available in most markets for people to see and experience till the last few weeks of the quarter.”

This is confirmed by a 18% reduction compared to their average quarterly production. It’s hard to know if demand would have been there but we can’t ignore this data. Inventory is also at its highest for the last twelve months.

But that can also be a timing issue; we can’t be certain. They also shared that interest for their cars didn’t slow down.

“And additionally, we had a record number of test drives globally in Q1 as well. So interest remains high […] But as far as absent macro issues, we don't see any reduction in demand.”

While Asia is apparently high on the new Model Y.

“We achieved record orders for a single day in the APAC region when we launched New Model Y.”

Third, the Model Y refresh did impact their sales in terms of volume but also in terms of pricing as they ran promotions to clear the legacy inventory - even if the average price per car remains higher QoQ.

Their fourth argument is about brand image & Musk; I will detail it later.

Bottom line: the company is selling fewer cars & isn’t growing its market share, at least in the total car industry, which is far from ideal from an investor point of view. Whatever the reasons.

On the cheaper model, timing has been confirmed, although macro & tariffs did slow down & will continue to slow down commercialization.

“This is the reason we're still focused on bringing cheaper models to market soon. The start of production is still planned for June.”

But there seems to be confusion as to what this model will be. We had no answer, but while many expected an entirely different product, what will apparently be sold is simply a cheaper version of actual products.

“And so, models that come out in next months will be built on our lines and will resemble, in form and shape, the cars we currently make. And the key is that they’ll be affordable, and you’ll be able to buy one.”

I am very curious on what it will be as no one has information on a model which should be sold in two months-ish.

FSD & Autonomy.

Management confirmed fully autonomous vehicles in Austin by June or July.

“The Tesla's that will be fully autonomous in June in Austin are probably Model Ys. So, that is currently on track to be able to do paid rides fully autonomously in Austin in June and then to be in many other cities in the US by the end of this year.”

As for Waymo & other competition, I made the case often already, but I’ll do it once more: the products are different. FSD is meant to drive like a human while Waymo & other AVs' are meant to drive in very specific & mapped geographies.

“So, because we're solving for is a general solution to autonomy, not a city specific solution for autonomy […] Once we can make it based to work in a few cities in America, we can make it work anywhere in America. Once we can make it work in a few cities in China, we can make it work anywhere in China, likewise in Europe, limited only by regulatory approvals.”

Besides their self-driving capacities, Waymo cars are very expensive - above $100,000 each, complex to manufacture & therefore scale rapidly, which will give an edge for Tesla in terms of volume but also pricing & geographies - you can have AVs driving you outside of cities, while Waymos won’t. Tesla’s vertical integration makes its product & software better & cheaper.

This is about the ride system. Besides that, Waymos & others are not meant to be commercialized to households.

FSD is meant for households & once safe enough, its deployment will depend on regulations only. This will make Tesla pass from few AVs to continents of self-driving cars overnight - & in my opinion, boost demand for those cars.

“Additionally, the advancement in FSD related features, including pilot robotaxi launch in Austin later this year, should help create a new era of demand.”

As for timing, most depends on regulations. Management expects unsupervised FSD to be available to households in the U.S. before year end. Not sure we should trust them on this as FSD still needs some fine tunning with some specific actions but that is what they are sharing.

Then… This sums it up.

“But in the in the future, in the not too distant future, buying a gasoline car that is not autonomous will be like riding a horse while using a flip phone. Some people still do it, but it’s rare.”

Energy.

The only business which is going relatively well. Demand for Megapacks continues to grow as its importance is being acknowledged by utility companies who are finally able to store some of their production.

This led to the highest gross profits for this branch of the company despite a -5.4% QoQ decline in installations - and a 154% increase YoY.

Deployments will continue to fluctuate, but this one is looking good - the only one.

Optimus.

Nothing new. I will spare you the usual timelines & expectations. The only interesting information is that management expects to have “thousands” Optimus working at their factories by year-end, which I wouldn’t be surprised if true.

As to massive deployment & commercialization, we’re far from it.

Tariffs, Supply Chain & Business Operation.

Llike any other car manufacturer, Tesla is affected by policies, although the company is probably the best positioned of car manufacturers as they have a gigafactory & local production in every continent they sell their cars on.

“With respect to supply chain risk, something that Tesla has been working on for several years is to localize supply chains.”

It won’t bring the impact from tariffs to zero as many components come from other continents - especially for their energy products as some cells & batteries come from China, but it reduces their impacts compared to competition.

“we do have localized supply chains in North America, Europe, and China.”

Despite this & having a preferential position, the company is struggling & is trying to find alternatives to China, first of all, but to all of its supply chain dependencies then, which is pretty complicated.

“We've also been working on securing additional supply chain from non-China based suppliers, but it will take time.”

This highlights perfectly the actual uncertainty for most businesses that rely on other regions. Supply chains cannot be changed overnight. I won’t go over this too much as either way, things will probably be different tomorrow… It’s just important to keep in mind how complex this kind of company is to manage daily, even more in today’s conditions.

Musk & DOGE.

I am not sure if this is important or even interesting, but it is worth mentioning. The team is obviously trying to pin some of the underperformance on Musk’s link with DOGE & its mission to reduce waste in the government.

“The natural blowback from that is those who were receiving the wasteful dollars and the fortunate dollars will try to attack me and DOGE team and anything associated with me.”

It’s obviously impossible to quantify, although I believe it to be true - to some extent, as I personally had discussions with people who believe Musk is evil for what he is doing at DOGE - in Europe, so for sure Tesla’s image is hurt.

But it isn’t a valid argument. He knew this would happen and did it either way & has his responsibilities. As to whether this can be changed, no idea, but Musk said he’d reduce the time spent at Doge & refocus on his companies, Tesla first.

“And I think starting probably next month, May, my time allocation to DOGE will drop significantly […] So, I think I'll continue to spend a day or two per week on government matters for as long as the President would like me to do so and as long as it is useful. But starting next month, I'll be allocating probably more of my time to Tesla and now that the major work of establishing the Department of Government Efficiency is done.”

I’ll let you draw your own conclusion; I know this is a polarizing subject, I just wanted to share what was said.

Financials.

Talking fundamentals is great, but fundamentals that do not make money aren’t interesting. And here we are…

A struggling EV business - whatever the reasons, with a 31% & 21% decline in sales QoQ & YoY respectively. The total automotive revenues declined slightly less thanks to the regulatory credits, which are part of the sector but should not be taken into consideration for the demand of their products.

As I said, the energy branch is the shining one but not shining too brightly. What is a 67% YoY growth is in reality a 10.8% QoQ decline but also a decline compared to Q2-24. The business started to flourish early 2024 but if it doesn’t ramp up, comparisons are going to get tougher from now on, and without acceleration… Nothing shines.

As for services, we have stable growth over the years and even if fundamentally important, we are not there financially - nor expected to be.

In brief, the best portion of Tesla’s revenues is average at best.

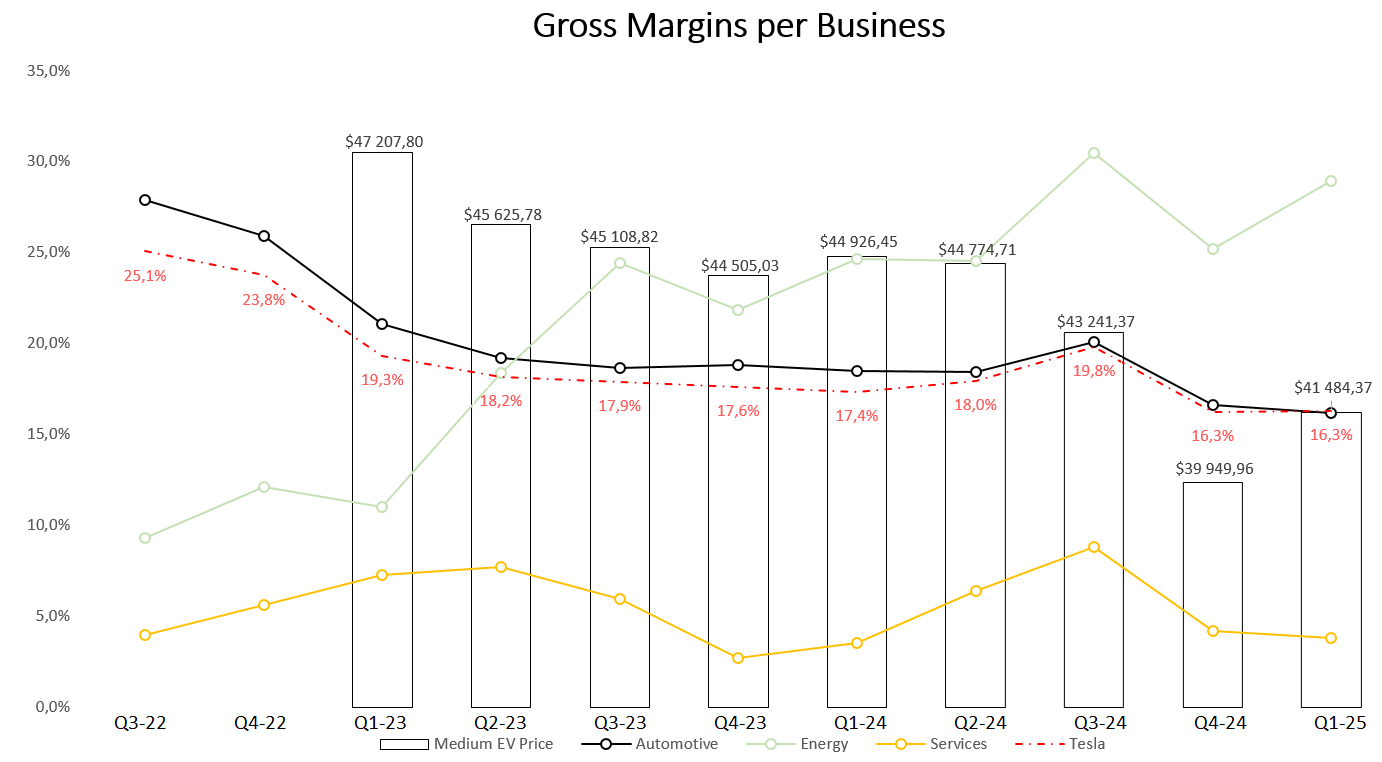

The silver lining of this quarter is that even if revenues are struggling, at least costs are maintained around the same percentage, which means Tesla’s gross margins remain flat-ish & each branch is also flat-ish.

At least that.

Lastly, expenses remained flat & even grew QoQ & YoY, which destroyed net margins, income, & cash generation - with pre-tax net margins at 3%… Terrible. Revenues are slowing but expenses remain stable to operate & improve the business - through Optimus, new products, Semis, Cybercab, AI, etc.

The only good thing, which is usual with Tesla, is their fortress balance sheet of $29B of net debt, which gives them lots of room to maneuver & continue to invest in their products and R&D.

“We believe even in the current environment, it is the right strategy, in making investments in these areas to position us for the long term.”

Conclusion.

I did not share any guidance because the company didn’t give any - we should get used to this with the actual uncertainty.

“It is difficult to measure the impacts of shifting global trade policy on the automotive and energy supply chains, our cost structure and demand for durable goods and related services […] We will revisit our 2025 guidance in our Q2 update.”

And I do not do any valuation for Tesla as everyone would disagree with it.

So I will simply conclude on the quarter, which was really bad, although the data on lower EVs production had a huge impact. It’s impossible to know how things would have been with normal production, but if demand met it, we would be having a different conversation & conclusion.

Tesla remains an investment for optimists who believe FSD is a superior product & will drive demand as anyone will want to have a self-driving car, and no one else proposes it. This remains the narrative & I will continue to hold my shares as long as Tesla is the number one in autonomous driving software & vertical integration. As long as this is true, it is only a matter of time for revenues to flow in.

“We expect to have these -- be selling fully autonomous rides in June in Austin, as we've been saying for now several months. So that's continued, but the real question from financial standpoint is when does it really become material and affect bottom line of the company and start to be a fundamental part of the -- when does it move the financial needle in a significant way? […] And then once it does start to move the financial needle in a significant way, it will really go exponential from there.”

Thanks for the update! Sooo many people hate on tesla just because of who's behind it, his public, shall we say, "performances", who Musk partnered with prior the elections and so on and so on... Those people just want to see Musk burn down, alongside everything he's doing.. very negative and animalistic style of response, but of course - that is just an opinion/observation. Future will tell if the haters were right in name calling towards Musk, or if they missed another good investment, based on their beliefs.