Palantir | Q4-24 Review & Call

Better than good & valuation keeps stretching.

If you do not know Palantir yet nor why I personally believe it could become one of the bigger companies in the world during the next decades, here it is.

“We are still in the earliest stages, the beginning of the first act, of a revolution that will play out over years and decades.”

Overview.

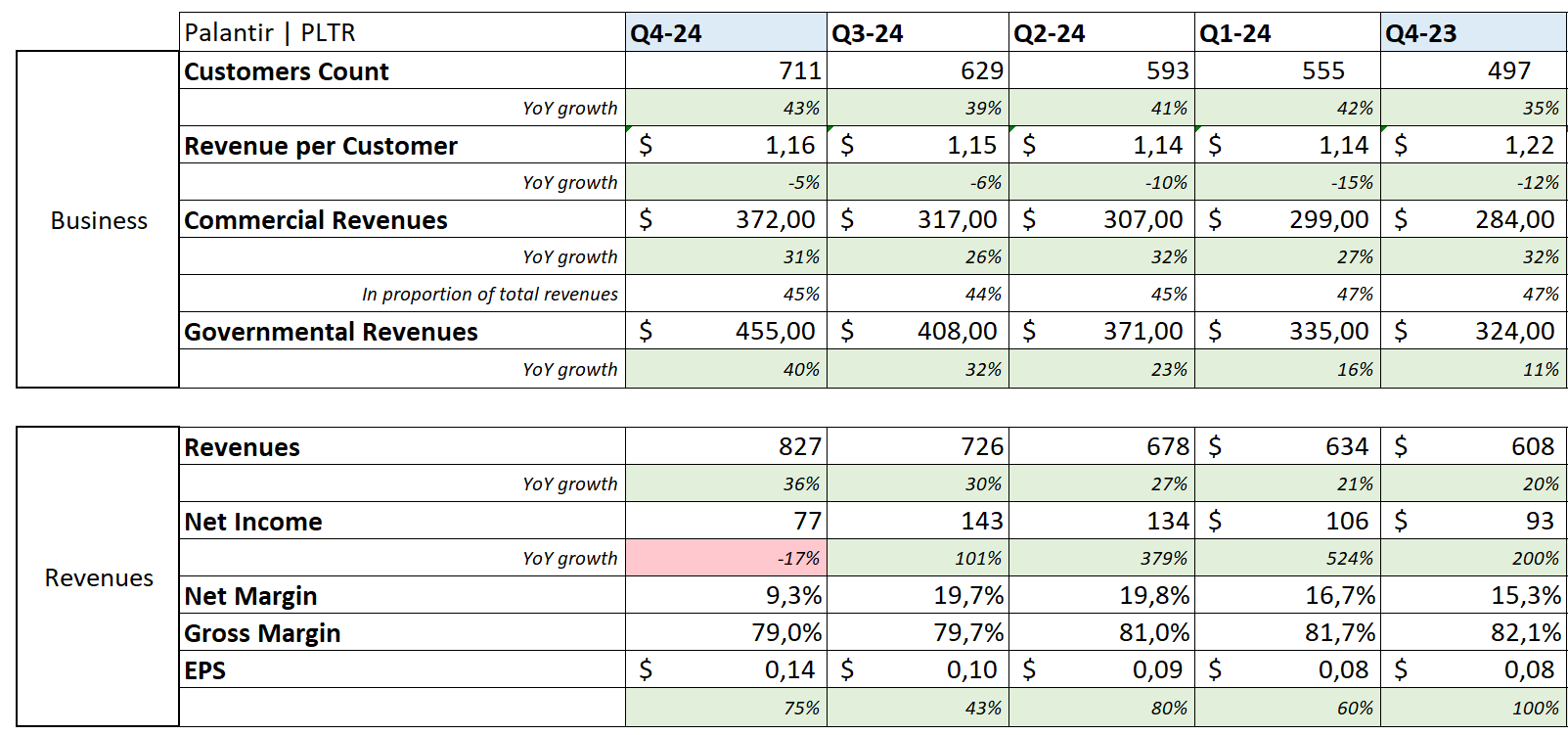

Revenue. $781.24M | $827.52M | +5.92%

EPS. $0.11 | $0.14 | +27.27%

This is the kind of report where we see rapid progress, but what really matters is to understand the company, not the quarter.

Business.

My bull case has always been the same: Continuous proofs of demand for AIP from commercial clients. there softwares are designed to help companies optimize their workflows. As long as this is confirmed by the numbers, my thesis holds.

And this quarter shows that it holds strong.

Customers continue to grow boosted by the commercial branch, which is exactly what we want to see.

The company closed 188 U.S. commercial deals this quarter. 129 deals of more than $1M, including 58 above $5M & 32 above $10M, a new record for the latter which confirms a growing usage from existing clients.

“AIP continues to fuel new customer acquisition as we have nearly 5 times the number of US commercial customers as we did 3 years ago and significant expansion opportunities at existing customers.”

This tendency is very bullish for the future as the total number of deals shows that some companies are dipping their toe into the AIP machine, while those who did it some months ago tend to confirm with bigger contracts. Meaning those who do it now might very well grow their AIP usage in the future.

“One of America's largest pharmacies has been a customer since early 2024 and signed a $67,000,000 TCV engagement with us right after the pilot for workflows including automatically load balancing prescription fulfillment and orchestrating patient outreach.

An American telecom company became a customer approximately 2 years ago and recently signed a $40,000,000 TCV expansion deal to help manage and accelerate their decommissioning of old network technologies and equipment in order to achieve significant cost savings.”

We now have enough proofs of the perfect market fit of AIP to any kind of business, with excellent results in many sectors including healthcare, transportation, manufacturing, sales etc…

Over all, what matters is to see that the company keeps attracting clients & delivering fundamental results, optimizing their business while the average contract remains flat or grows for Palantir.

And this is what the data shows. There’s nothing much more to say.

I also have to talk about the governmental business which is doing wonderful, with apparently some ties with Elon Musk’s Doge. It isn’t necessarily part of my bull case but it remains an important part of the company, growing 40% YoY and accelerating QoQ, exactly like the commercial part.

We had an interesting question about the impact of Doge on their governmental branch as it could mean closing some parts of the government using Palantir.

"Palantir's real competition is a lack of accountability in government, these forever software projects that cost an insane amount, that don't actually deliver results."

I believe this answered the question pretty well, Palantir could actually capitalize on this trend as the government would require more efficient tools. Palantir is that tool. The government would certainly do well spending more money onsoftware & less on human resources, and this was actually one of the first goal of the Doge.

It remains the main source of revenues for the company & this is a good thing at the end of the day. But the bull case remains with the commercial sector.

I will also add a few words about DeepSeek which has no impact on Palantir. Karp has been saying for months or even years that LLMs were a commodity & that the value added was in the models themselves. Palantir’s AIP is unique, and that is what gives value, not the LLM used to converse with it.

Financials.

It comes without surprises that the financials are excellent & beat expectations.

Growth is really impressive & continues to accelerate with a 14% rev. growth QoQ & 28.7% YoY - compared to a 7%, 7%, 4% & 4% QoQ growth over the last quarters & 16.8% last year. This is what pushes Palantir’s valuation through the roof, we’ll talk about this just after.

Margins remain strong, flatish around 80% for the gross margins, sometimes slightly above sometimes slightly under, it doesn’t really matter as long as it is only fluctuations.

The decrease in net income is due to a one-time stock compensation increase as Palantir includes them in its revenue statements as expenses. It’s their way of doing & comes from compensation to the team for achieving targets.

Some will not be happy about it as it dilutes shareholder 6.6% YoY, others will argue that without such compensation the team wouldn’t be motivated enough to produce such results… I’ll let you pick your team, I’m personally fine with the deal as my shares are up more than 500% since I bought in.

Besides this point, the business remains very profitable & growing as excluding those compensations & interest on their cash, we’d be talking about $918M income FY24 compared to $449M FY24, a 104% growth YoY for the business only.

I believe interest on cash should be included as the cash stacked in treasuries isn’t used for investment & is part of the business, while SBCs are arguable. What I try to share here is that even without those, the business is highly profitable & getting better each year.

Besides this, Palantir closes the year with $5.2B in cash for no debt, $1.15B of OpCF - including $691M of SBCs, hence a 56% margin excluding SBCs & $517M of FCF - again, excluding SBCs.

I am trying to paint the honest picture here as I know Palantir’s SBCs are controversial. As I said, I am all in for companies to reward their workers in shares as it should motivate them more & as long as it pays out positively.

It did pay for Palantir. But I can understand if some find it outrageous. You have the information, you get to decide.

Guidance.

The report was great already but guidance was the cherry on top as it proves that there is an even stronger demand in the future.

The Q1-25 is a bit slowing with only 4% growth QoQ but the FY-25 guidance is talking about 30.5% revenue growth, which confirms the company’s acceleration & the market even expects more as it bases itself on the FY24 outperformance.

It gets better, this states that U.S. commercial should drive the future growth which falls perfectly into my bull case & expectations - and many others'.

Valuation.

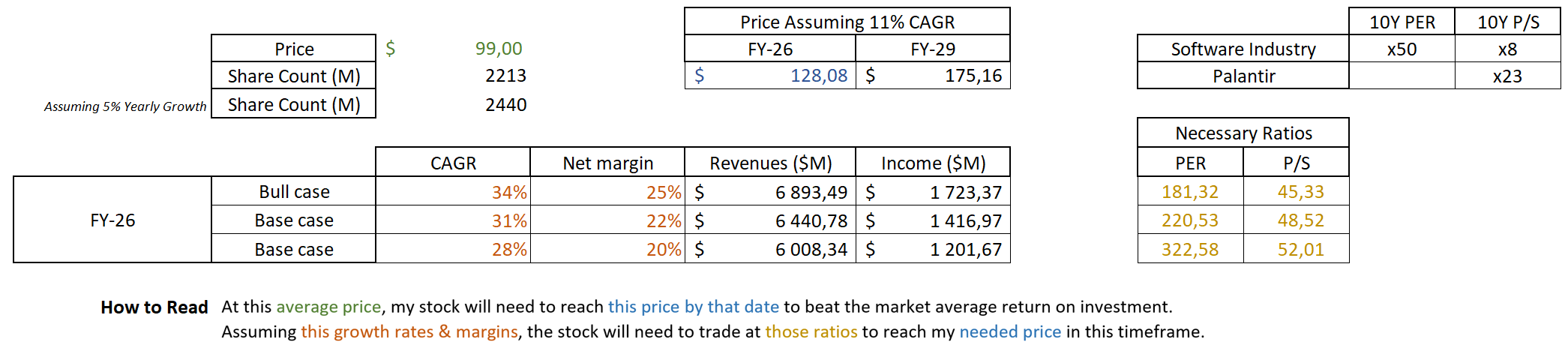

Now to the bigger subject. Valuation was already stretched but got even more after this quarter as the stock is around $100 pre-market. Why is that?

Palantir is a growth stock. There are plenty of ways to value a growth stock, but the market mostly uses P/S & F.P/S and its capacity to generate growth, of course.

If a stock trades at 10x P/S and guides for 40% growth while its stock price doesn't move, it'll trade at 7.14x P/S the next year. If the company beats its own guidance & talks about a growth acceleration, it trades at 4.86x F.P/S.

As growth acceleration continues, the forward multiple keeps decreasing, and the market gets excited & anticipates more growth accelerations, hence higher P/S as eventually it means lower F.P/S.

This is the only mechanism necessary to understand why Palantir is so expensive. The market anticipates growth, Palantir delivers growth, the market anticipates more, and by doing so, increases the actual P/S.

As long as the company delivers & accelerates, multiples can be ridiculous. When growth or guidance slows, the market will know how to price Palantir based on fundamentals.

And that day will hurt. But it isn't today.

As for what I would consider fair value for Palantir, assuming it can sustain 30% growth or more for the next two years… We’re far from it.

Buying at today’s price would require over 45x F.P/S to beat the S&P500 in the best case scenario. Useless to say, this isn’t something I’d buy as 34% CAGR over the next two years would require a really big acceleration FY26 based on FY25 guidance.

This quarter showed that acceleration was possible but FY25 guidance would barely have justified its old price. The market got excited & pushed the stock even higher, hence, back to a really stretched valuation.

My fair personal fair value doesn’t change much from the last report. Anything between $40 & $45 would be deserved based growth & its actual fundamental premium.

But my little finger tells me that the day this stock shows lack of growth acceleration, the market will simply destroy it & won’t bother about fundamentals anymore. Big chances we pass from extremely expensive to extremely cheap.

Only a hunch though, markets are always surprising and there’s no way to know when nor if this will happen.

My Take.

Quarter is excellent. Year is excellent. Bull case is alive & I honestly am glad to be on board of this train. Once again, I really advise you to read the investment case if you didn’t, it’ll help understand why this company is different.

"Organizations who have crossed the chasm with Palantir are driving real impact quickly."

I tried to share this quarter with a neutral point of view, leaving aside my excitement. Everything isn’t perfect & I understand some here or on X complain about SBCs or earnings on interest rates. But that is to be added to how great the company is fundamentally, evolving & growing. There’s more to the story.

I am entirely aware of the actual pricing, completely detached from fundamentals but I shared how I view it. I am clearly not a buyer nor would advise anyone to buy at those prices. I am sitting on my hands, Palantir will probably continue to show great results for some time but am aware naysayers will one day be right & the stock will get demolished.

It’s just not that time yet.