Palantir | Q3-24 Earning & Call

Another proof of AIP's market fit.

If you still do not know about Palantir, you'll find everything you need here.

Overview.

As a reminder, my investment thesis is based on the company’s comercial branch & on how AIP is essencial to optimize any business from any sector, indirectly becoming a must have software for almost any company. Palantir is also working with western governments but this isn't where its value lies for me.

EPS. $0.09 | $0.10 | +11.11% beat

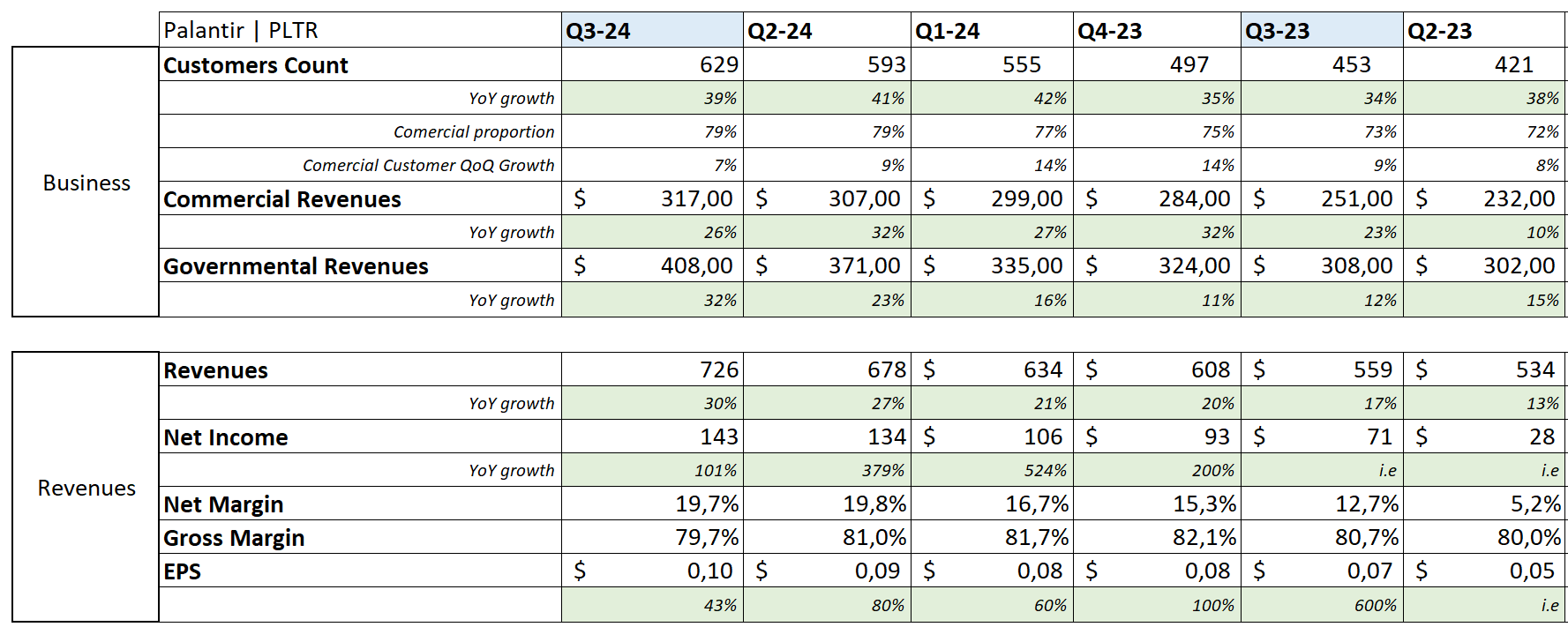

Revenue. $701.13M | $725.52M | +3.48% beat

$46.6M of buybacks the last 9 months.

“We absolutely eviscerated this quarter, driven by unrelenting AI demand that won’t slow down. This is a U.S.-driven AI revolution that has taken full hold. The world will be divided between AI haves and have-nots. At Palantir, we plan to power the winners.”

Everything related to Palantir's commercial branch is growing, from its customers' count to its growth rate. This is where Palantir's actual & future value lies and the data which I am looking at closely.

Business.

This quarter brings more proof of strong demand for AIP & how impactful the tool is for companies, with lots of clients' testimonies talking about either a significant price reduction, resource need reduction or time reduction for any given task since using AIP.

This is what Palantir is about.

It also highlights how excellent AIP is as Palantir is reaching such growth without much advertising, mostly thanks to mouth-to-ear of an excellent product & methods.

“We believe that by investing, and we know at this point, instead of trying to have 10,000 clients, all of whom hate you, this is kind of what people want, 10,000 clients that hate you, but they can't give you your product. We want a smaller number of the world's best partners that, quite frankly, are dominating with our product. And the way you do that is by not blowing up your margin and getting 10,000 salespeople. It's actually by going deeper on the product. And in fact, what we see is the deeper and better the product, the more we drive sales, the more we have our singular advantage as Palantir, not as a commodity product. We are not a commodity. We do not want our customers to be commodities. We want them to be individual titans that are dominating their industry or the battlefield.“

And as they say, and I said in the investment case, there will be those with Palantir & those without Palantir.

“As we said, really, it's going to be the haves and the have-nots. The AI haves are moving quickly, making decisions quickly, and adopting quickly.“

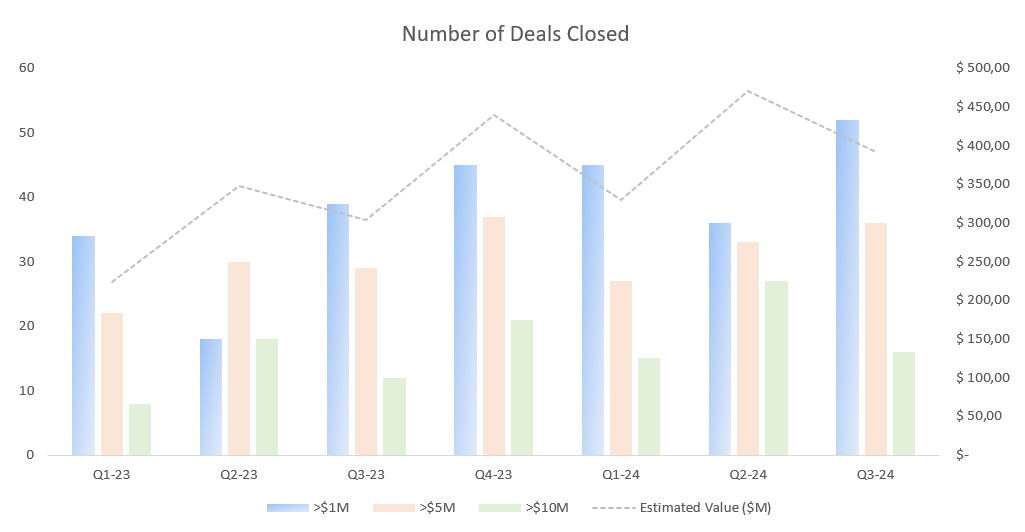

There are more & more haves lately and Palantir is working hard at implementing AIP within their companies as fast as they can while most clients or bootcamps participants come back to deepen their partnership. This shows in the numbers of deals closed & in the company's retention which is now around 118%.

The QoQ dynamic is pretty interesting but we clearly see a strong amelioration YoY in both value & number of deals closed.

To talk more about the commercial branch, we've seen a correct & stable revenue growth of 26% YoY while customers grew 7% QoQ which shows a strong demand for AIP. Combined, once more, with testimonies & management saying that most of their clients come to deepen the partnership, the data is pretty promising. Although up to now, Palantir's revenues are very concentrated with only 20 customers, responsible for almost half of Palantir's yearly revenue.

“Third quarter trailing 12-month revenue from our top 20 customers increased 12% year over year to $60 million per customer.”

I believe it is a good thing, a proof of growing demand & deepened partnership with older customers as they realise AIP’s impact on their company. A trend which should continue as again, everything points to a great retention & a growing demand from new & existing clients.

I don't spend much time on the governmental part of Palantir which, even if very significant & growing rapidly - up 30% YoY this quarter, still isn't my bull case. It is a great bonus though with such growth.

Revenues.

Financials are obviously excellent and improving.

The first 30% YoY quarterly growth with expanding net margins while nine months ending are positive on every metrics with strong growing revenues, up 27% YoY, stable costs & expenses hence growing margins - net margins reaching 19%.

The quarter closed with $420M of OpCF & $435M of Free Cash Flow for $4.6B of net debt. Very strong, although SBC is a big portion of FCF - still not an issue as it is an incentive for employees and goes well with the company's spirit.

Guidance.

That is where I kind of am surprised to be honest.

We're talking about a Q4-24 & FY-24 revenue growth under 30% which is far from weak & satisfies me, especially with how well the commercial sector is going and should continue to go - at least according to the info we have.

But the market reacted very well to a flatish growth... Too well.

My Take.

As usual, there are two ways of watching quarters: As an individual investor and from the market point of view. In the first case, I am very satisfied; commercial branch is growing very well and we have tons of data & testimonies of AIP's value & need across all sectors. Another proof of Palantir's market fit.

What surprises me is the market reaction to these earnings with the stock surging more than 10% and trading around $46 at time of writing. The data is great, but it's not great enough to justify today's valuation. I said many times that anything under 30% growth couldn't justify it; it was true yesterday so it obviously still is today, not with a guidance under 30%, without acceleration.

Those assumptions here are, in my opinion and from what the data shows, pretty optimistic already and would require a very high P/S to have proper returns.

We could make a case to buy Palantir today with a 5-year horizon expecting nothing less than 25% CAGR up to then while the stock would never trade under 24x sales during the period… Hard to call this a base case.

Palantir is expensive. Really, very, very really expensive. Everyone does whatever they want with their shares of course, I am personally holding everything and will be very happy to buy more when the stock falls because I believe it to be a when, not an if. But you guys can of course disagree.

The fundamentals are stronger than ever. The need for AIP is also stronger than ever. The demand is stronger than ever. The valuation is stronger than ever with a new ATH this morning and as it is said, "The market can stay irrational longer than you can stay solvent."

Holding hard, there’s nothing else to do.