Palantir | Q1-24 Earning & Call

I'll let Karp introduce this earnings call review.

"Welcome to our Q1 earnings. I think it is fair to say we crushed Q1 in the U.S. We are on fire."

The first takeaway is very easy for me: Great. We have everything we want and need to see.

Business. Let's start by talking about the business itself.

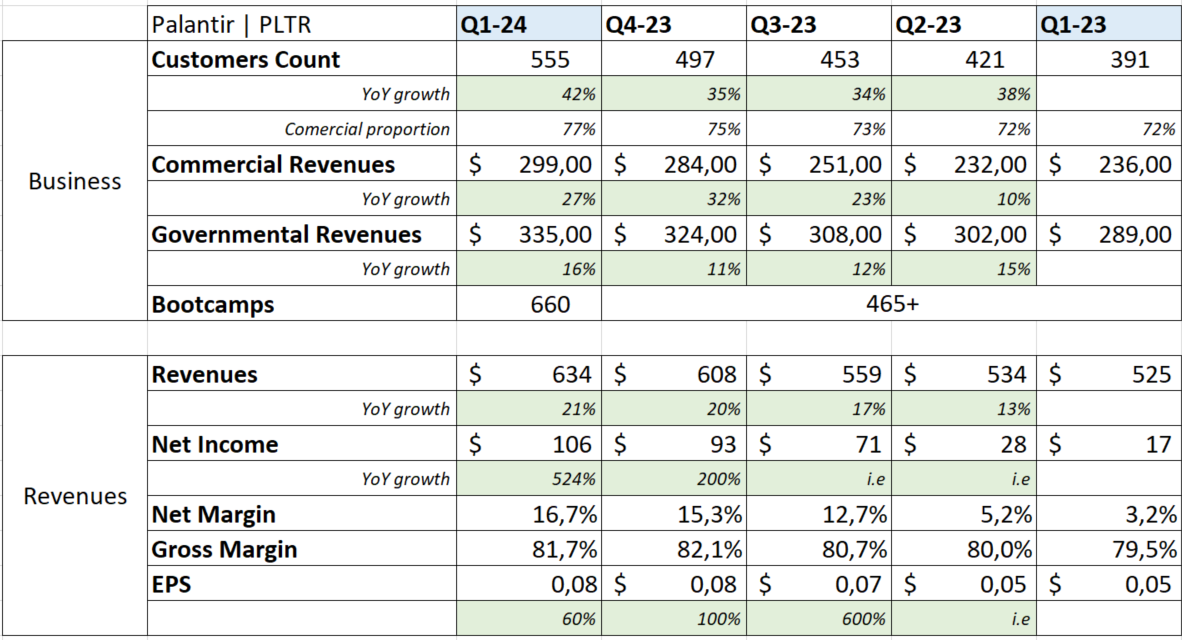

Customers. Many investors and naysayers are trying to argue that Palantir isn't really offering anything special, is an AI fraud or a simple consulting company. I strongly disagree with all of those, and I think the customer count here proves that they are delivering a highly demanded service to more and more companies. And it is proven by different data.

We're talking about 915 organizations that participated in a bootcamp - almost twice as many as last quarter.

"We've sustained our high volume of bootcamps with over 915 organizations participating to date to meet inbound demand."

And actual customers are deepening their relations with Palantir's products.

"Net dollar retention was 111%, an increase of 300 basis points from last quarter."

In terms of pure data, they grew the customer count by more than +10% QoQ and +40% YoY, which are clearly not small numbers. Their service is needed and demanded, and that isn't happening at this pace for an AI fraud or a consulting company.

More importantly in my personal opinion, commercial revenues and proportion in the global customers count are growing. This sector is the future of the company, what will make Palantir a $1T company one day and is growing faster than the rest, with revenues up +27% YoY and +5% QoQ.

Most of the growth coming from U.S companies as E.U is still scared and regulating AI, and I'm not sure about the links between Palantir and APAC, sadly...

I wouldn't be surprised if this branch were to outgrow the governmental branch before the end of the year. This is what I want to see and what I expected.

It is important to note that the governmental branch is also growing correctly, but it simply is a bonus to me. This isn't my investment thesis.

Bootcamps. Now let's turn to what made the difference since 2023 for Palantir because the company wouldn't grow that fast without this new go-to-market strategy. We are talking about 660 bootcamps done in one quarter, which is more than the entire 2023 year.

But the good new doesn't stop there as the conversion rate stayed around 20% - that's a rough number and not exactly right as new deals can be made out of bootcamps, but it gives a rough idea of their efficiency.

The company closed 136 deals - compared to 70 in Q1-23 - with 87 above $1M. Which gives a total conversion of 20.6% and a conversion for deals above $1M of 13.18%. This is very strong, and I'll run my old model later on with those new numbers to see where we could be going for Palantir as a company and as a stock.

In the meantime, the company intends to keep going.

"The continued interest in AIP is loud and clear in the conversations I'm having across our customer base. We've shared our plans to capture the market with AIP. And our results show that our strategy is not only succeeding, it is accelerating."

Expectations. II wrote my expectations before the earnings, and they've clearly been smashed.

I wanted to see commercial growth in terms of customers and revenues, and I had both, with the commercial branch taking more and more importance in the customer base.

I wanted to see bootcamps grow while maintaining a conversion rate around 20%, and I had both - bootcamps grew more than I expected as I said I'd be happy with 250 of them, ignorant as I was.

There is nothing disappointing in the entire report.

Revenues. Nor in their finances.

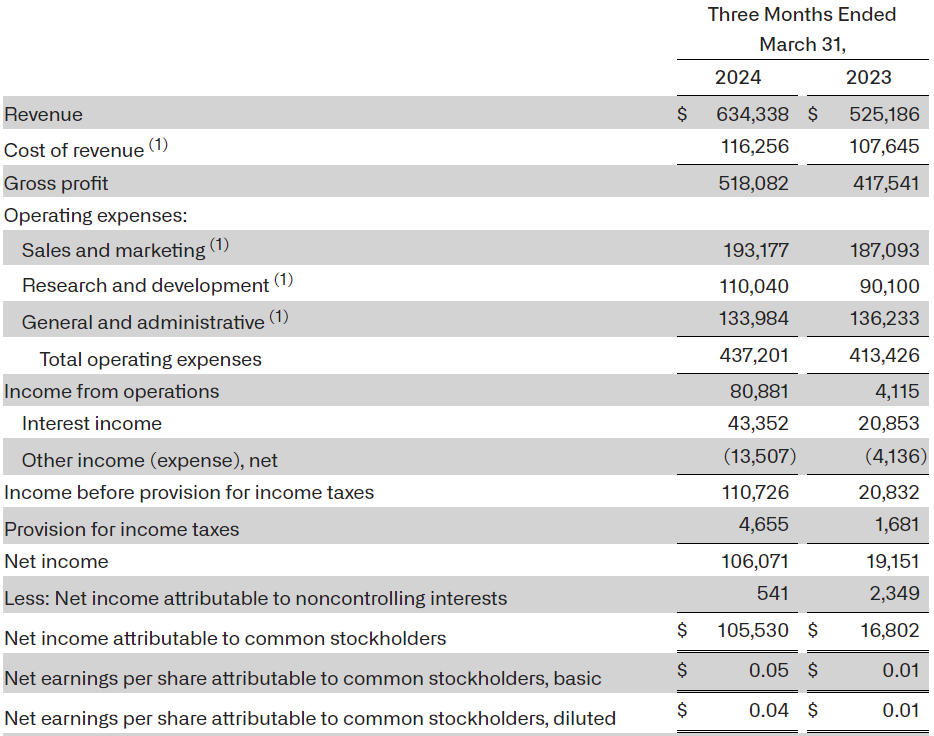

We saw revenues and net income were strongly up YoY but there's more to it as net margin also grew, thanks to kind of flat operating expenses. I know I say it often lately as we are having great earnings, but a company able to grow revenues rapidly while stabilizing operating expenses is everything any investor wants to see.

It is the proof of a well-managed company with strong potential to grow earnings. It's the recipe for strong Cash Flow and balance sheet, which is the bare minimum to start buyback and return value to shareholders.

It smells good.

And it shows as the company is ending the quarter with $3.9B of net debt and $149M of FCF out of $130M of OpCF.

I won't lie, everything is great in this quarter, but I still will have two complaints although they might be more personal.

Stock-Bases Compensation. Firstly, those shares emissions were necessary earlier but we're now in the fifth quarter of profitability, and I'm not sure the company needs to dilute its share count anymore with their balance sheet and positive FCF - even without those.

Having said that, I am all for compensating employees with shares; it boosts morale and creates a will to make the company succeed as a part of your personal income depends on it. It's a win-win situation, so my take here isn't to stop those programs.

It's maybe to use some of that cash to buy shares from the market at least to offset the dilution. It's no biggy as the company will do it later on either way. I'm just wondering when. But again, it's just the art of finding something to complain about a great quarter.

Political stence. Secondly, and I have complained about it largely, I still do not like the company taking public stance on pretty controversial subjects. Karp says himself that they're the western go-to when it comes to direct conflicts and that is normal as they sell military softwares.

"There is basically no conflict in the world that is not -- where Western allies are involved and the battlefields involved and the stakes are life and death, where Palantir is not the first call."

This is normal for the company to publicly have a position on those subjects. But there are others where I don't see why they want to implicate themselves...

I don't see how this slide deserves to be the third one on their quarter reports. I do understand they have to publicly stand for Israel for example but what happens on U.S campus isn't their business. Only my take and it doesn't even reflect my opinion, no one cares about it and I won't share it.

Moving to greatness again.

Guidance. The company raised the FY-24 guidance which shows, again, everything I want to see.

Strong growth (above +20% minimum) led by the commercial branch of the business. Profitability through every quarter which leads to a strong cash flow, hence a stronger and stronger balance sheet over time.

Everything is simply going very well here.

Assumptions. I'd like to repeat once more that those are only assumptions and are based only on numbers written on an excel files so let's not get hooked to them, it simply is here to give a rough idea of where $PLTR could go over the next years. And the team is pretty bullish on where they're going.

"We expect the favorable unit economics and higher throughput to continue to accelerate our business. U.S. commercial is where we're seeing the greatest transformation."

I took some liberties which I consider pretty conservative. We're assuming 2,500 bootcamps per year which is normal at a rate of 660 boot camps per quarter, the only variables is: Will they have enough demand to keep up this number? Probably to my opinion.

The conversion rate is about 20% exactly as it is today but I assumed every deal was a $1M deal here for simplicity which shouldn't be very far from the real medium as more than 60% of those deals are of $1M or more.

I shouldn't be far from the truth with those assumptions.

And those would lead to a yearly revenue growth of $500M per year which ends up being lower growth than the actual company's guidance at least for FY-24. So again, I shouldn't be very far from the truth.

The stock price is based on today's P/S of x23 as I didn't want to juggle too much with numbers here, so it would need more detailed reasoning but that's what I propose today and it doesn't surprise me to assume a fair price around $25 with today's results and guidance.

Conclusion. You understood it, I'm really convinced by this quarter. I loved everything I saw - at least in terms of business and financials. I don't mind much the company displaying their opinion because they don't sell to retail either way, so they won't be impacted by it. Yes I complained about the small dilution but buyback will come in time so that's only temporary.

Simply. Great. I said I was waiting for the $20 gap to buy in, but this quarter changed my opinion. I have a medium price around $16 so I will keep accumulating at today's open assuming we stick under $25 and won't grow my medium price above $20 for now. Great companies have to be bought at fair price. And as Karp says, and I agree with him

"Currently, I don't believe we have competition."

As usual, I do me, you do you!

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!