OlO | Q4-24 Earning & Call

The easiest stock to hold.

If you do not know about this company, you’ll find everything you need here.

Overview.

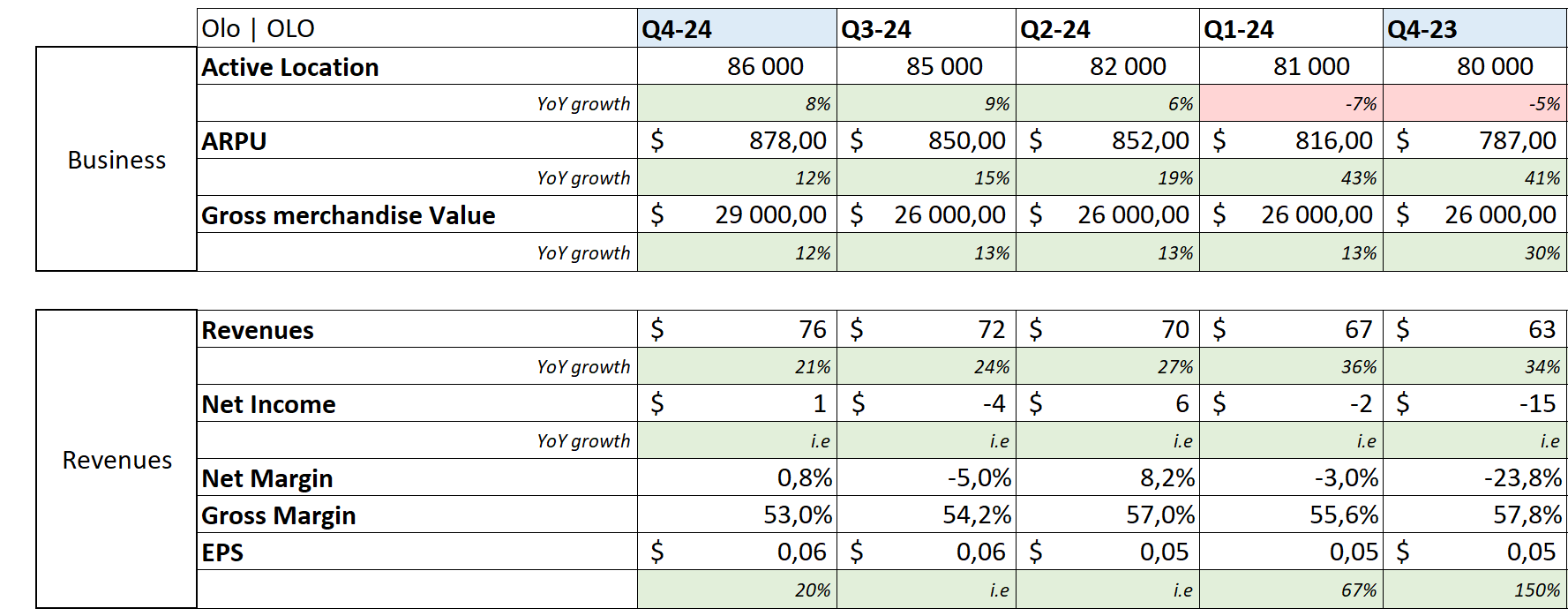

Revenue. $72.76M | $76.07M | +4.55% beat

EPS. $0.07 | $0.06 | -14.29% miss

As advertised: very easy to hold.

Business.

Everything is going according to the original thesis. More franchises are attracted to Olo while others tighten their partnerships, driving better results for their own business while Olo flourishes & drives always more volume.

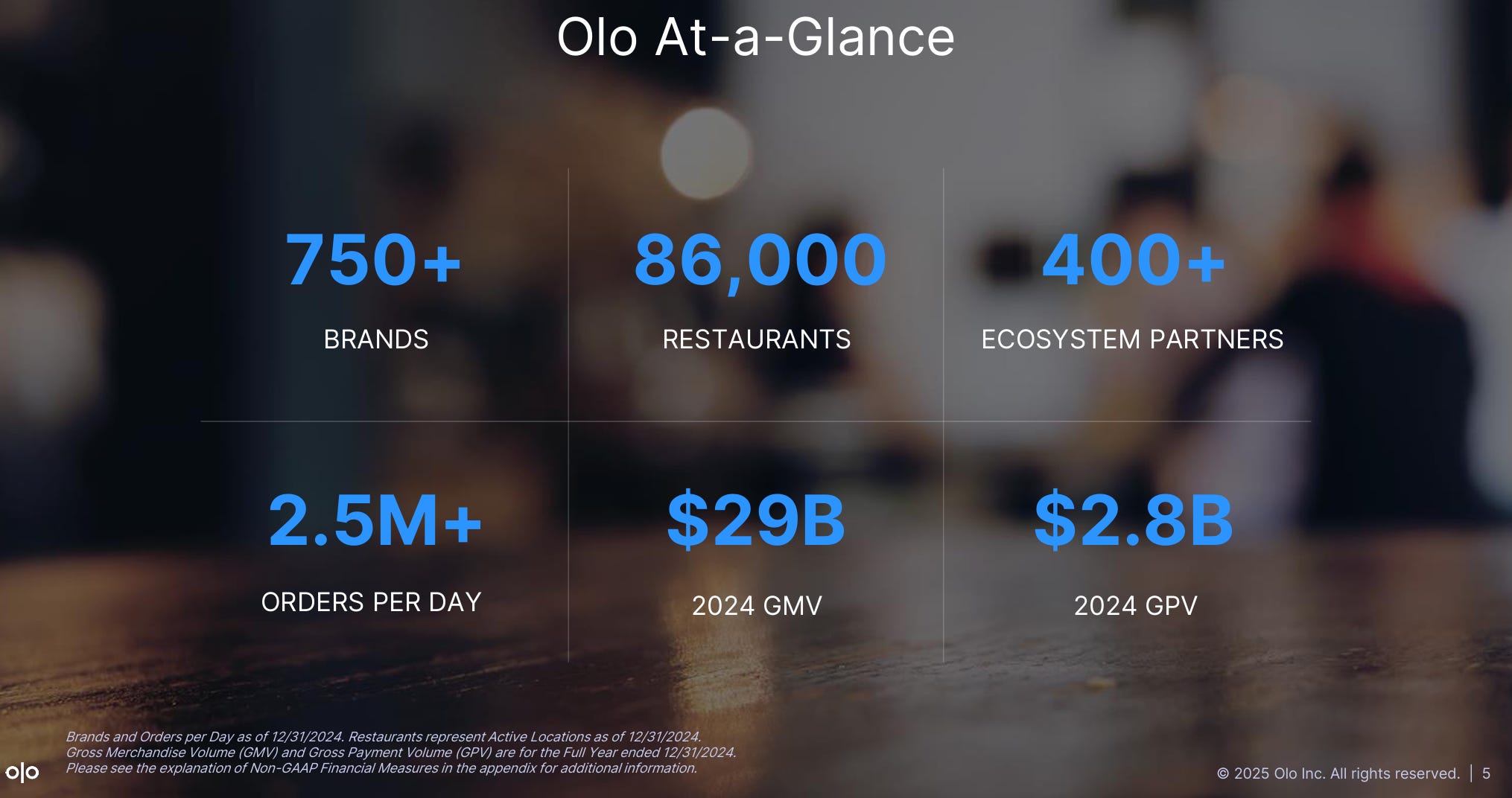

“If Olo was a restaurant brand, this level of sales would make us the second largest brand in North America ahead of Starbucks and trailing only McDonald's.“

The key metric to me remains ARPUs which translates the demand for Olo’s product & confirms that their clients grow their module usage. They grew 12% YoY for the quarter and reached $3,387 for the year, up 25.3%.

This is the most bullish data to me. It shows that fundamentals are improving while demand for their services is strong. This growth acceleration which comes from both growing usage of their modules & growing volume - as the company charges fees on performance.

This growth came from both a growing consomation & a tightening of Olo’s relations with its clients. the average module usage jumped from 3.5 to 3.7 YoY. Small bump considering the company offers 16 modules but the story is only starting & Olo Pay card-present should be the next driver to grow modules usage.

The second important metric is obviously the numbers of active locations which grew above expectations this year with a net addition of 6,000. Growing ARPUs & growing user base means accelerating growth.

Olo Pay.

Here is the bull case going forward. Olo already offers online payment but do not offer card-present payment. Their modules remained interesting but not having this service was a break to their growth as they couldn’t operate 100% of restaurants’ operations.

This is changing & will change faster as they started partnerships with different PoS in 2024 but reached a new partnership with FreedomPay this quarter, a payment provider with over 1,000 POS.

“This accelerates Olo's time to market, enabling us to sell and deploy Olo Pay card-present into the majority of our location base more quickly than by integrating with one POS partner at a time.”

Providing card-present pay can unlock huge growht as Olo Pay had only $2.8B of payment volume this year while Olo’s platform saw $29B of volume, a bit less than 10% of total volume.

Not saying they will have 100% of volume passing through Olo Pay but card-present will grow the proportion in much higher double digits.

Besides the growth coming directly from Pay, it should help convert franchises to use more modules as they will now be able to have their entire operations on Olo stack hence collect 100% of their clients’ data, allowing them to optimize their operation but also grow the long term value of each of their client.

Revenues.

Data is pretty good.

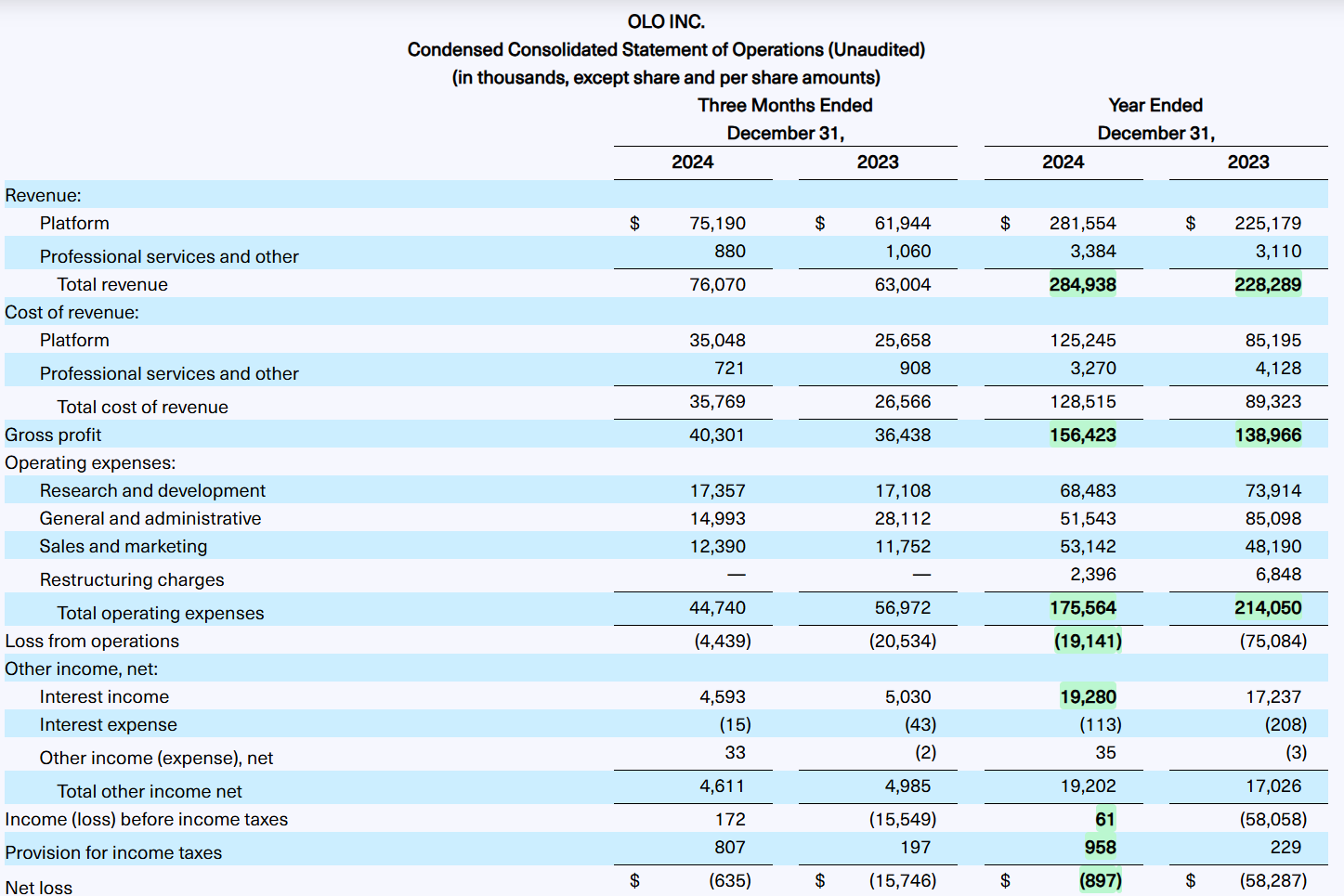

Revenues grew 25.8% YoY while gross margins are declining, partly due to the scalling of Olo Pay which is a lower margin business so nothing to worry about here. They agreed to sacrifice margin for future stronger growth - which is yet to come.

Truth is, they also optimized very well their internal organisation as expenses actually declined while revenue grew… You don’t see that often & this helps operating margins, although the business remains unprofitable - but getting better.

Interest on cash helps the year to only close at a $897,000 loss which is negligible, everyone prefers profitability but they’ll get there.

Olo ends the year with $403M of cash for no debt, no shareholders dilution as SBCs are bought back & $27M of FCF - boosted by SBCs as the company isn’t profitable.

Guidance.

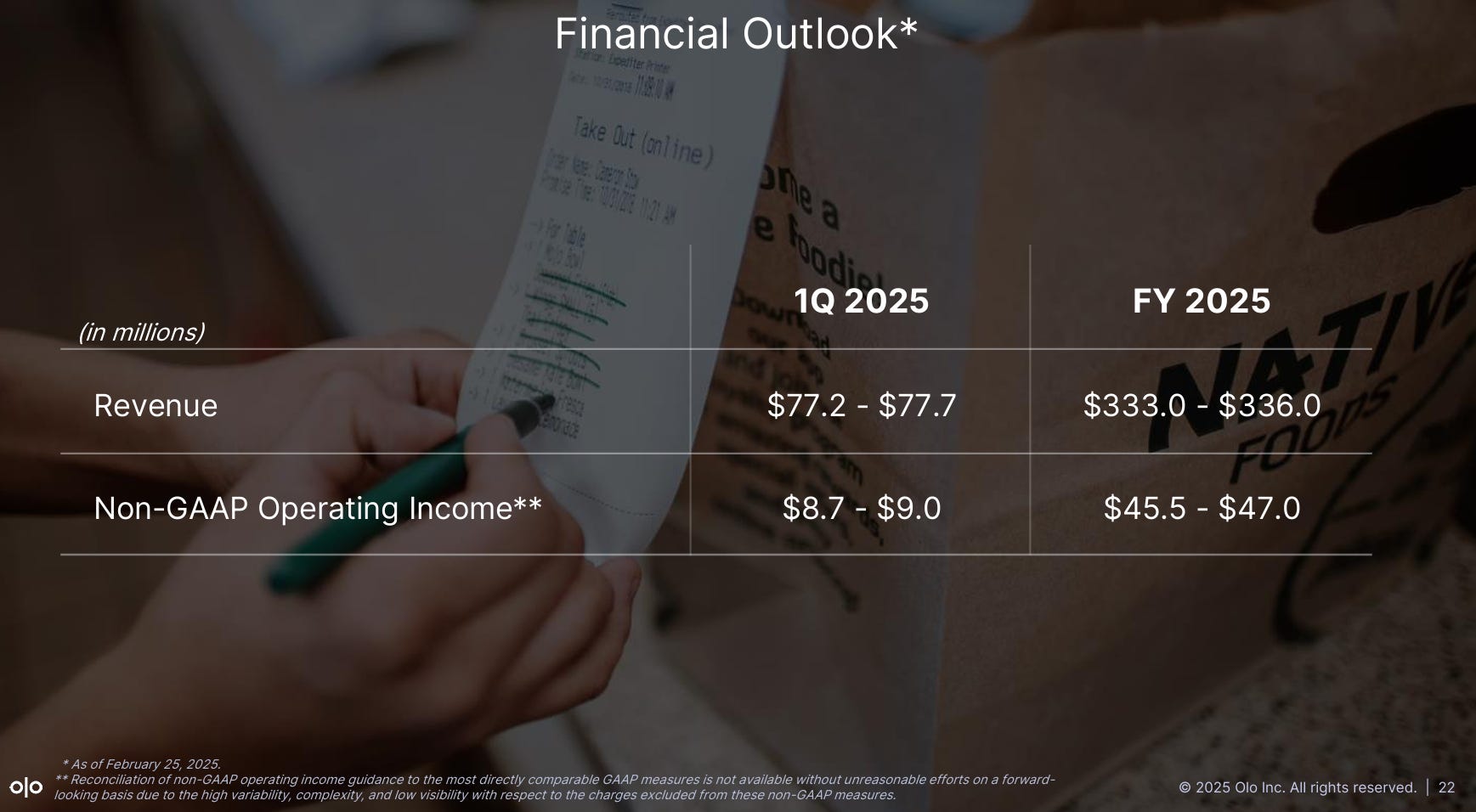

Guidance remains strong but I had higher expectations.

Don’t get me wrong, I am not disappointed as we’re talking about a continuous growth around 20% FY25 - 19.6% to be precise reaching the high range of the guidance, with profitability.

As I shared earlier, Olo Pay is the last tool needed for Olo to deploy its full potential & I assumed FY25 was the year, but it’ll take a bit more time to see acceleration as deployment isn’t as fast as investors might hope. Real life’s a bitch.

“We expect full year 2025 Olo Pay revenue of approximately $110 million with card-not-present transactions continuing to account for the vast majority of total Olo Pay revenue. We expect card-present revenue to begin to ramp in the second half of the year and contribute gross revenue in 2025 in the high single-digits million-dollar range.”

Gonna have to be a bit more patient to see if this really drives conversion but it’s not possible to be disappointed with the actual guidance. A steady & strong ship is a very good ship.

Besides that, company’s guiding to 5,000 new net location during the year & precised that guidance was made on the assumption that the economy remains comparable to FY24 - which I doubt but we’ll have to wait & see on that. Important precision as part of their revenues is based on their clients’ performances, not to say that they’ll have issues but to say that if things go wrong, we’ll need to distinguish what comes from Olo & what comes from external factors.

My Take.

This is a really good quarter & year and as I said, it is really easy to hold this company. One would love to see more fireworks but a steady boat is a boat which goes further. We’ll need to wait a bit longer to see if Olo Pay will, as expected, drive to a growing usage of modules by their clients.

Not much more to say. Holding strong.

they mentioned rule of 40 on the call and with yoy revenue at 25%, ebita should be going up