Olo | Q2-24 Earning & Call

When everything goes well.

Everything you need is here if you do not know Olo yet.

Overview. I'll make it quick: things are better than good.

EPS. $0.03 | $0.04 | +33.3% beat

Revenue. $67.75M | $70.5M | +4% beat

$6.9M buybacks.

"The breadth of our platform and the scale of our network help brands to use omni-channel guest data to drive profitable traffic: a key metric for success in the restaurant business."

The overview might not look super bullish but the quarter is better than the numbers suggest. Investing isn't only about revenue & EPS.

Business.

As the investment case explains, Olo can scale through two levers: active locations and ARPUs, and it continues to do both.

Active Location. Let's start with the least important metric. Olo brought in 1,000 new restaurants since last quarter, and this trend should continue as the team expects to grow by about 5,000 more locations throughout the year.

“We continue to expect location count to ramp throughout the year and to add approximately 5,000 net new locations this year.”

This will be achieved mainly thanks to Dutch Bros’ restaurants being integrated during the second semester, which should bring the total count to around 85,000 active locations by the end of the year - slightly below my assumption of 89,000, but we'll review that later.

ARPUs. The most important metric for Olo, and it’s going very well with 19% growth YoY and 4.4% growth QoQ, driven by better performance from Order & Engage and the deployment of Pay.

“The year-over-year increase in ARPU was driven by increased order volumes and modules per location, in particular Olo Pay.”

We can notice a slowdown in the growth but this will certainly pick-up again with Olo Pay card-persent service deployment.

Olo Pay. More customers are expanding into Pay - El Pollo Loco, Miller's Ale House, Culver & the Pollo Tropical. This will be a very important part for Olo in the next quarter as it will be the next source of growth but also the source of lower margins - which isn’t as bad as it looks. This is a necessary service for the company.

We actually have two ways to pay by cards, online & physically.

“The latest data point that we've received via NPD is that digital transactions account for about 18% of all industry transactions.”

This highlights why it's so important for Olo to have card-present payment systems in its restaurants. This will grow revenue and ARPUs massively while helping collect more data. We already see how significant this is with HoneyGrow, which is already part of the physical Olo Pay service.

“By powering both digital ordering and all payment transactions, we estimate that Olo's gross profit per Honeygrow location was more than six times higher than Olo's gross profit per average location over the last three quarters.”

No need here to detail the opportunity and how this will grow ARPUs over time through different leverage - firstly the transactions themselves, but also the data collection which will help leverage the Engage suit and therefore bring more traffic to the restaurants, meaning more transactions, etc, etc...

To make this happen, Olo partnered with TRAY, another POS.

“TRAY joins NCR Voyix and Queue, and we have expanded relationships in the works with additional POS providers. These expanded POS partnerships move us closer to processing card-present transactions, which can help us drive meaningful scale in our Olo Pay business and help reaccelerate our gross profit growth.”

Engage. As explained above, the Engage suite is all about leveraging client data efficiently for both restaurants and Olo. We already have some feedback with Five Guys, which just started using Engage this year.

“In just over six months, Olo's GDP ingested millions of orders, created 4.5 million guest profiles, and automatically identified cohorts of Five Guys' most loyal and highest lifetime value guests. From there, our marketing module helps Five Guys create hyper-targeted marketing communications and measure their impact on sales.

The results, $2 million of incremental revenue attributable to the email campaigns, a 1% increase in shake sales, and a large base of new guest profiles that Five Guys can use for future campaigns.”

Those aren’t small achievement and are real world data. This is how Olo can help any restaurant chain be more efficient, bring more revenues and engage better with its own & potential new clients.

Retention. It's no surprise that Olo ends another quarter with very strong retention above 120%. Franchises stay in Olo’s system and expand their commitment to more softwares.

A good example of how well Olo's services work is &pizza, a restaurant chain that initially decided to build in-house tech but ended up coming back to Olo.

“With our gross revenue retention exceeding 95%, most brands remain on our platform and the trend we've seen since our IPO is that more brands migrate from in-house tech and to the Olo platform.”

This is why SaaS companies succeed: they focus time and resources on a specific part of a larger business. It’s very hard and expensive to do everything yourself, and &pizza realized it.

Revenues.

A few important things to note in term of numbers this quarter.

First of all, the data is pretty good in term of growth and we can easily notice a reduction in term of expenses, a pretty strong one. This is an important part of the report.

“In Q2, all three operating expense line items improved year over year on a percentage of revenue basis.”

There’s more I’ll detail now.

Margins. I’ll start with one of the most important concepts for any business: margins. They have been declining pretty rapidly over the last quarters - around 70% in early 2023. This is usually a sign of a declining business, but nothing could be further from the truth here.

Olo proposes three very different software suites: Order, Engage & Pay, each with various services within them. All of these scale with their clients’ success, but not with the same margins. Order & Engage are both high-margin software, but Pay, whether digital or physical, is a lower-margin service.

The decline in overall margins is mainly due to the faster deployment of Olo Pay, and this trend should continue over the next few quarters - hence, gross margins will continue to decline, and that would be good news. As mentioned earlier, Olo Pay will be a strong source of growth, allowing Olo to collect more data, bring more subscriptions to Engage, roll more revenues through it, and help the restaurants achieve better results - bringing returns to Olo.

Gross margins will continue to decline, and this isn’t a bad thing in this case.

Income. This is the first profitable quarter for Olo, and this will change a lot of things for the company, starting with its cash balance. Driving growth isn’t free, and Olo has done it by burning through its cash pile, raised during its IPO.

This tendency is certainly over now that the company is profitable and closed the quarter with $387M in cash, up +$37M QoQ for the first time in its history. Olo is mostly a software company and will not have much capex nor investments through the next year, so its profitability will allow it to grow this cash pile again and either return or invest more freely, without the pressure of unprofitability.

Big change.

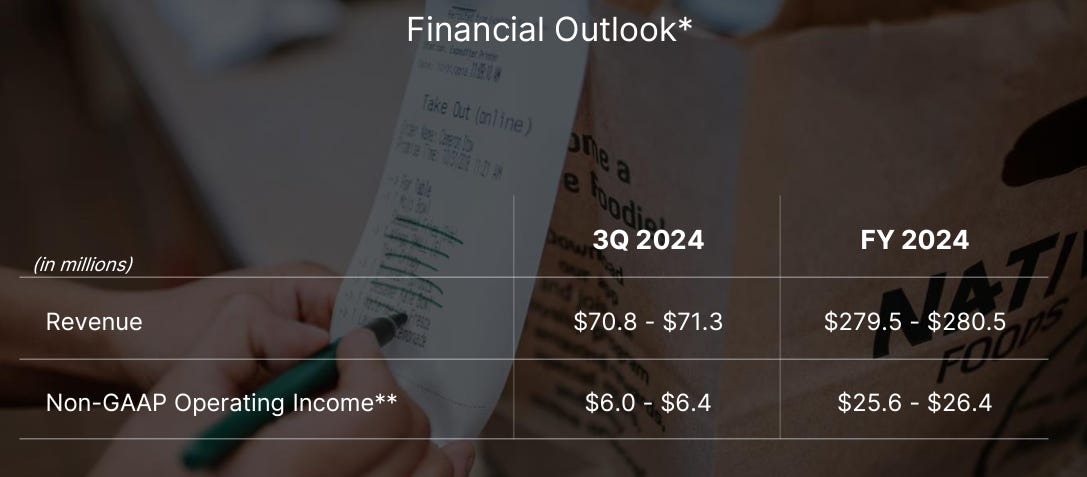

Guidance.

A good quarter starts with a great guidance and Olo wasn’t different as it rose its FY-24 expectations.

We’d be talking about around 22% growth YoY for both Q3-24 & FY-24, but most importantly, we’d be talking about a profitable company from now on, and as I said earlier, this will make a big difference for its future.

Most importantly, this guidance includes more newcomers and a significant growth of ARPUs.

“Revenue guidance continues to assume a two-thirds, one-third split between incremental revenue from existing projects currently in deployment and new projects signed and deployed in year, which will be driven primarily by ARPU expansion as Olo Pay scales and we have further success selling multiple modules in our order and engage suites.”

As shared earlier, guidance includes a decline in margins due to the expansion of Olo Pay.

“Lastly, we expect full year 2024 gross margin to be in the low 60% range. We anticipate second half gross margin will be approximately 200 basis points lower than the first half 2024 gross margin performance, with the majority of this decline occurring from Q2 to Q3. This reflects the timing of the revenue mix shift in the second half of the year due to Olo Pay's continued momentum as I discussed.”

Again, not a bad thing as this will boost the company’s scalling.

My Take.

It is very hard not to be bullish after such a quarter, and the market realized it - although the same conclusion applied last quarter, and the market ended up selling the stock after a similar +20% in pre-market.

We have more proof of the perfect synergy between the company’s software and the need for franchises to use them and to couple them together - and that this coupling yields returns for everyone.

“[…] which is a win for the guest, a win for the brand, and puts us in a really strategic position as that brand's digital consigliere and their conduit into their guest book.”

Olo Pay will make a big difference during the next quarter and was the last piece missing for Olo to be the sole and efficient digital provider for hundreds of franchises.

Future is bright.

Valuation. The 20% pump this morning brings the company around $900M of capitalization and an EV of $530M, growing around 20% for now, this growth should continue through the year and very probably the next one as Olo Pay will need time to be deployed and installed, and this should take up to 2025 at least.

I think we can be pretty confident assuming 20% growth up to 2026 - without any black swans. It’s a bit harder to estimate the future net margins, but again, we shouldn’t be far off with a high single digit, up to 10% as shown in the guidance.

I wouldn’t call those ratios small but they’re also far from unachievable for a company growing 20% CAGR with a very strong balance sheet and great prospects, so I wouldn’t call Olo expensive even after that 20% pump.

We’re still talking about a very small capitalization, and lots of things can happen - much more risk here than with big caps, so let’s not take those valuation assumptions too seriously; they are meant to give an idea, not an answer.

As for me, I have a much lower base cost already, largely under $5, so I intend to continue buying. I will just wait a little bit for the excitement of this quarter to calm down and will buy a big chunk once more.

This quarter is giving more and more indications that Olo could turn into something great.