Olo | Investment Thesis

The one who knows you.

It’s finally time to talk about food! Or tech. Let’s say it’s time to talk about a tech company that is trying to revolutionize the restaurant industry. So, a bit of both.

To summarize Olo in a few words: It is a tech company proposing services to help restaurants digitalize most of their business & daily tasks and to collect & use their own data to improve productivity, marketing & hospitality.

“Enabling hospitality for the digital age”

[The company]

So what does Olo offer? Many services, divided into three categories: Order, Engage & Pay.

Overall. Let’s start with a more global overview. Olo offers different services with different monetization forms and restaurants aren’t forced to subscribe to a full package, they can choose only one or a few functionalities. This modularity helps Olo to show the strength of their products and allow companies to slowly subscribe to more tools, as integrating the entire suit at once could be too expensive and complicated for many.

Let’s start with an image to understand their products. Ever been to Korea, or Asia?

You usually have those tablets and order/pay directly from there, digitally. The order is then sent to the kitchen to be prepared and served by a waiter, whose only role is to deliver the food. A world with fewer waiters – as long as Hooters keeps theirs, I’ll be fine. Those systems already exist at McDonald since long for example but not many franchise build in-house softwares. This is the base of what Olo offers: a digitalization of restaurants.

But it goes further than just on-site ordering. Olo will manage on-site, online & deliveries. It will manage paiement & tips. It will also collect and share the clients’ data, from its meal to its payment method, building a profile to be leveraged. It will also help with numerous other aspects of a restaurant’s day-to-day operations, from optimization to supplies and other organizational aspects invisible to consumers.

It will digitalize & optimize the entire restauration workflows.

Order. A pretty classic option when you go to a restaurant, isn’t it? But there are many possibilities to order food nowadays and lots of ways to consume it. Olo offers them all with a possibility for complete and detailed customization. They simply deliver the framework and backend interactions - that is, the connection to other Olo tools and the data collection.

You can order on-site, with QR codes, tablets and more or online from the restaurant website or even from Google. You can order to pick up, to dine-in, to drive-thru, to be delivered - Olo partnered with Dash in the U.S who will deal with the deliveries.

Everything is meant to be as simple and intuitive as possible and another functionality called “Rails” allows restaurant franchises to manage the entirety of their menu or customization from a central console, which means fewer people to deal with all those complicated topics - and collect & analyze all the data.

We are simply talking software here. Olo offers a customizable framework to do all those things and is entirely invisible to the end customers. Restaurants or franchise owners can configure it and deploy their new, fully functional and seemingly in-house website or sit-in techs thanks to Olo’s technology, working behind the scenes.

Engage. Restaurants which use Olo software own every bit of data. I probably don’t need to detail how having access to your restaurant's data is a game changer as it allows management to know their customers, their habits, their meals and products performance or underperformance, the paying method and much more. Here’s Olo’s webpage if you want more information.

https://olo.com/gdp

A rapid example to what Olo can propose to restaurants.

John comes four times a week at lunch, between 12:30 and 1 PM to WR’s sandwich stand and orders either the chicken sandwich or the Caesar salad, with a long coffee and pays by credit card. I know this because of the data Olo collected for me over the last year. John is a known customer and you know his habits so why not make everything ready for him already? Maybe send him a text or an app alert: “Hey John. Sandwich or Salad today?”. From there, my beloved customer only needs to present himself to my stand where his food is already waiting for him with his coffee. He won’t even wait as I know he’ll pay by card and those things can be automated.

Just for you to have an idea, but things could go much further.

This is Olo’s end goal. I know, I know. Many will react saying “I don’t want this, when I go to a restaurant I want the restaurant experience.” Very well. Two things. First, Olo won’t take over the world so you’re fine! Second, I’m sure we will always have “old school” restaurants which will charge more to have the “old school” experience with a waiter, a paper menu, and a bill to pay at the entrance.

Digitalization cannot be avoided and most restaurants will go through it to reduce costs and deliver a more personalized & optimized service, it simply is good business for them. Also, keep in mind that there is dining and eating, some people don’t have lots of lunch time and hate to wait 45min because everyone eats at the same time, at the same place. Olo can make a difference there.

Besides this, engage goes further than just your customer’s data as it also includes any data related to your restaurant. That could be Google or TripAdvisor comments and grades for example which would be collected and available from the Olo software, allowing management to dispatch and collect information from centralized software, once again.

Every bit of data that concerns your business is collected & analyzed.

Pay. I am not sure I need to detail this branch of Olo’s service. They have been working this last year to implement on-site and online payment systems and are now deploying them.

This was developed as it became obvious for Olo’s management that they needed to propose a solution for any potential interaction between a consumer & a restaurant to be relevant and integrated. From the moment a consumer wants to eat somewhere, heir software will manage everything. The online data, the information, the menues, sit-in or order online, be delivered and pay. All of it.

The value. This is a summary of each branch of Olo’s software. All of them are then divided into tons of different services which restaurants can contract or not - they do not need to subscribe to it all. They do not need to, but they should as this is how Olo’s products are meant to be used & deliver the best performances.

Olo is an optimization service, helping restaurants boost productivity, improve client relations, reduce owner costs while collecting and analyzing your business data, the most valuable resource in today’s world. Olo’s products allow franchises and restaurants to start a virtuous wheel of improvement, optimization and therefore growth and revenues.

A win-win-win service in one of the oldest and most important industry of the world: restauration.

[How do they make money?]

As for the business description, we’ll need to divide this into different categories as they have more than one revenue stream - the perk & flaw of modularity.

Order. This is the largest part of their service and the main one. It usually is accepted through a three-year contract with a one-year auto-renewal, restaurants and franchises are in it for the long term. In the case of a franchise, Olo signs with exclusivity which means that all the restaurants of, let's say, Five Guys, now use Olo's services - they rally do.

Olo’s revenues are then divided between a fixed subscription and a percentage fee on the restaurant's revenues.

Billed monthly. Again: Everyone wins.

Olo helps the restaurants and franchises upgrade their service and increase revenues while billing a subscription and a fee based on their performance. The setup is designed for everyone to scale.

Deliveries. As mentioned, the delivery service they offer is not done by them but by Dash although Olo keeps a small fee for the service - another one, after taking the fee from the order. How does that work? The order is taken by Olo, which interfaces with their provider, pays them, and takes a fee on the payment.

Engage. The engage suite is simply based on a subscription model depending on which service the restaurants want to subscribe to - as I said, restaurants can choose to only take one or another and do not have to subscribe to it all.

Pay. Very classic business here, Olo will take a small fee for each transaction passing through their system. Olo partnered with Adyen to manage most of its payment methods - notably online.

[Go to market]

You probably understood that Olo’s services are a bit complex to distribute because restaurants already work very well and do not need (and probably do not want) any form of digitalization.

Olo’s goal is to convince them that their services are valuable, the future of their industry and that they live in a world where not adapting means slowly falling into irrelevance - most of them didn’t want to accept credit cards some years ago, imagine that today.

The question is who’s the main target?

Franchises. Not individual restaurants which could be an interesting target but wouldn’t bring enough revenue to Olo and wouldn’t even want to integrate this kind of solution because as said, they probably don’t need it much.

But franchises do as their goal is to grow bigger & optimize their business and to do so, you need to be efficient, cost-efficient, with the best tools to help you manage a big park of restaurants and your consumers’ habits.

Exactly what Olo proposes and that is why they insist on exclusivity. So far, it seems to be working quite well, considering their user base growth, with names like Five Guys, Applebee's, Cheesecake Factory, Chili's, Denny's...

https://olo.com/case-studies

[Finances]

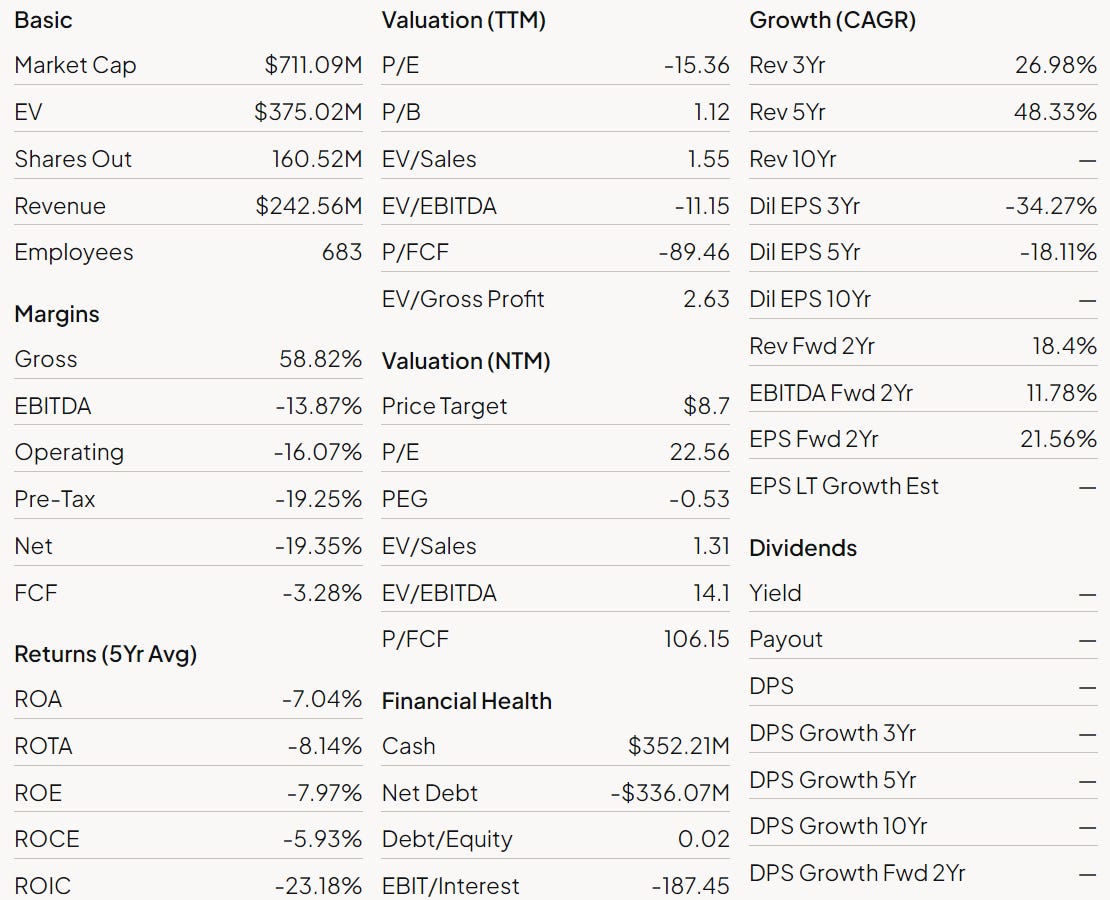

Olo is still a very small capitalization of less than $1B and is still focusing on its growth. Before going through their finances I’d like to talk about their leverage to grow.

Active locations. Obviously, the more restaurants they offer their services to, the more revenues they will generate as they base those on a fixed fee but also on a performance fee.

The marketing team has a huge task to convince franchises that they need their products.

ARPU - Average Revenue Per Unit. This is the medium revenue per restaurant. This data has to grow over the next years to confirm two things: demand for their software & that restaurants make more money by using them - hence Olo makes more as well.

This is to my opinion the most important data to watch to know if Olo is doing great or not - and so far it has been growing very well.

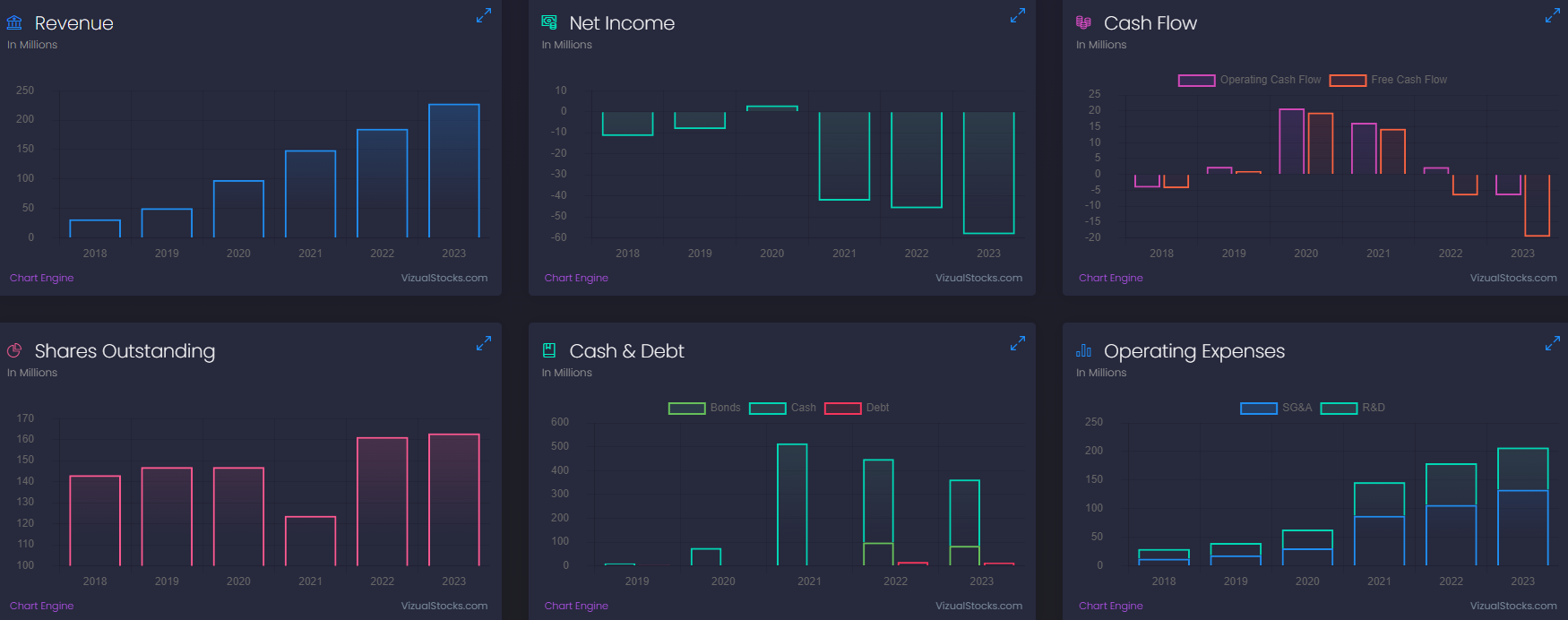

Now, about the finances.

Classic gowth.

Revenues. Olo grew 27% CAGR over the last 3 years and 48% CAGR over the last 5 years. Those aren’t bad numbers but the market needs more as this growth isn’t showing a really strong potential for such a small capitalization. Far from saying this is weak but for big money to be interested by a $1B cap, they need a success story.

That being said, we’re still early and on a very hard business to disrupt and I am not surprised that things take time.

Income & Cash Flow. The company is burning cash to grow more rapidly which is a very normal behavior, as long as we have a strong growth.

Balance sheet. The balance sheet remains strong with a $350M net debt financed through shares dilution.

The story. Those are the data as they are but they tell a story, the one of a classic growth company: Raise cash through shares program and use that cash to fuel your growth, spending it on marketing and sales expenses to bring clients and revenues.

No surprises to see shares outstanding & S&M expenses grow, that’s how things should be - and it seems to work as the increase in expenses is largely offset by the revenue increase.

The dilemma for any company is to create a healthy, growing, and profitable business before running out of cash - or ways to raise cash. Olo seems to be a good candidate, burning less than $100M per year on its operations while keeping its shares outstanding pretty flat this year and not raising any debt. With its $350M of net cash, it could run for at least four years on its current reserves at the actual rythm - enough time to bring more confirmation than the business is healthy & growing… Or not.

This is the most important to me at the moment, to see the business grow. Finances will follow with time.

[Valuation]

I won’t talk about valuation per se; I’ll do a rapid overview of some important ratios because I personally believe that the company is pretty cheap right now - although it’s hard to say with growth stocks & low caps.

And yet…

We’re talking about a company trading at a $700M capitalization and holding $350M of cash, hence an EV of $375M. With TTM revenues at $242.5M, the EV/Sales ratio is x1.55 which is pretty low - very low.

As the company is burning cash to sustain its growth, this EV/Sales ratio is bound to grow larger over the next months but revenues are also expected to grow more than 20% in FY-24 according to guidance - so probably a flatish ratio.

This seems to be a very reasonable valuation in my opinion. I believe the market isn’t very interested because it's a bit cold on low caps lately and Olo’s growth isn’t an hypergrowth story but rather a steady ship.

I’m fine with that.

[Olortunity]

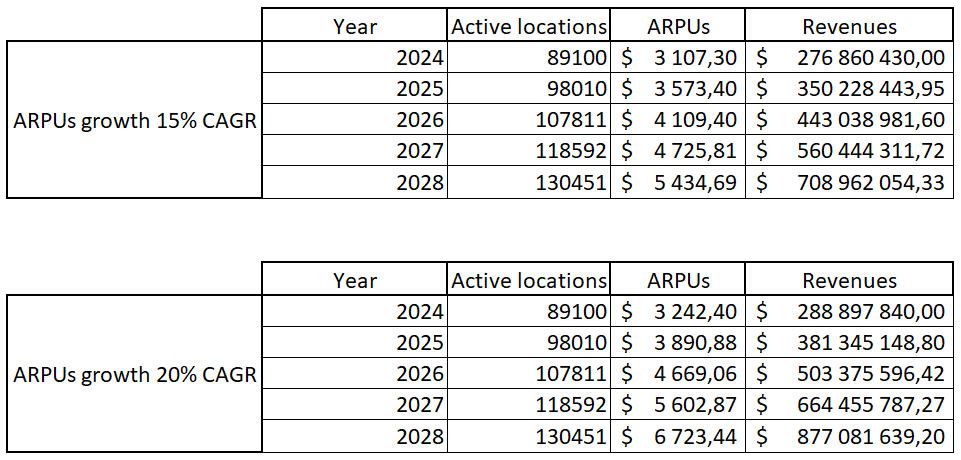

It is very hard to categorize Olo into a market and have an idea of its potential shares as they’re a software serving the restaurant industry, so instead of talking about a market I will talk about the potential of their two leverage: ARPU and active locations.

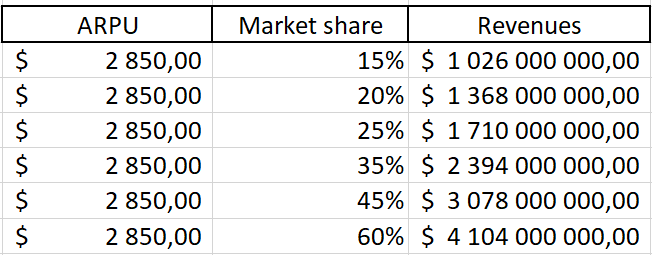

Active locations This section will talk about growing active locations while keeping ARPUs stable - around $2,850 FY-23. With more than 81,000 locations, Olo covers around 10% of U.S restaurants with one of their services or more - estimating around 700,000 restaurants in the country - Google’s number.

This raises a few question.

Can Olo be sold to 50% of the U.S restaurant market? Uh… Except if their products were to be integrated with franchises like McDonald’s or Subway which own roughly 30,000 restaurants in the U.S - combined. Add to this independent restaurants which do not have the need and other franchises with in-house tools and… It seems a bit hard to reach such a market share in my opinion - short/medium term at least.

Even if, is it enough? Olo would need to own more than 55% of the entire market to pass the billion dollar of revenues… Which is of course a strong number but delivering Olo’s software to more than half of the restaurants of the country seems… exaggerated.

Now, let’s view things with a wider optic: Olo expands to the entire west and especially to Europe and its 1.6M restaurants - where food is an art. And let's be crazy and add Canada in the mix. That would bring the potential to roughly 2.4M restaurants but would add complexity as European restaurants are tons of small and independent ones and not franchises. But there is potential.

Now 60% of the western market is of course impossible and yet would “only” bring $4B in revenues. This whole discussion is simply to give some perspective and an answer to my original question: Growing clients isn’t the best way to grow revenues.

ARPUs. Growing ARPUs is, and to do so Olo has to sell always more services, bigger packages and to prove to the restaurant world that their services are valuable so they’ll trust their entire workflow to the company’s softwares. To go back to the American market with a stable market share and growing ARPUs.

Those numbers seem big but Olo is growing ARPUs around 30% YoY and growing them to $4,500 is “simply” a +57% from today’s - doable by 2026 at the actual rhythm. This is much more probable to happen as the company has released tons of new products in 2023 than to expand to 30% of the U.S market.

Active location & ARPUs. Obviously, both are better - with a focus on ARPUs. Again, this is just to give an idea of the potential and not at all to be a projection on the company’s future revenues or stock price. This is assuming they’d grow active locations by 10% each year, resulting in 13,000 restaurants using Olo by the end of 2028 which is less than 20% of all U.S restaurants - Not unachievable, especially if the company were to expand in Canada or Europe, although this is pure speculation.

It is very hard to estimate up to where ARPUs could go & how fast but the company is far from its ceilling at the moment as Olo Pay just rolled out and very few of their clients are using the entire Olo suit - I wish I had have deeper data on this.

The truth is doubling their ARPUs over the next five years wouldn’t be that surprising to me if the company provides the value it advertises as restaurants will slowly upgrade to the full package after testing a few modules. If something makes your life (and revenues) much better and the company who sold it to you proposes other softwares which all together would multiply the betterness… Lots of chances you end up subscribing to it all - or most.

Conclusion. This is the thesis on Olo, that over the next months and years, they'll gradually deploy some of their modules to new franchises, while existing clients will expand their subscriptions to add more modules. One module helps, but integrating the entire software package will completely transform their business - for the better.

And we're talking about the restaurant industry here, not a random or small sector. It's one of the biggest, oldest, and most competitive businesses that will very likely never disappear - imagine a world without restaurants. Plus, while I've been focusing on restaurants for simplicity through this write-up, Olo's software can also be applied to food trucks, catering services, small shops, and more - not just sit-in restaurants.

Now, Olo is still a risky investment with a very low capitalization and many factors to consider before buying in, this is a very long-term investment. I personally believe the company is offering great, valuable, and in-demand products that address a real problem, especially nowadays with the cost of labor. Their products are the kind of software that will allow some franchises to optimize their business so well that they'll have an unquantifiable advantage over the competition.

And that's very valuable for any business, especially in such a complicated and competitive industry.

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!

Very nice introduction to olo. I like the prospect of those companies, because if the software creates value for their customers, the fees will roll in.

In the other hand this platform doesnt sound like rocket sience and perhaps the biggest risik is that a compeditor will offer a better and cheaper software that undermines olo's prospect.

Does olo have any direct competitors right now?

To me, it sounds like a candidate for constellation Software, doesnt it?

Nice write up. I agree it’s long term look but they have the means and cash on their balance sheet that they will be bought well before then. I say within nxt 2 years we will look back on the shark that ate them. Mr Glass will be a board member on the company who bought them and the rest is history. Question is at what valuation?