Nvidia | Q4-24 Earning & Call

As strong as usual.

I did not yet write an Nvidia investment case although we’ve probably all heard about the name by now, but I will try & remedy this during the next months, once the earning season quiets.

Overview.

The AI king keeps on beating.

Revenue. $38.04B | $39.33B | +3.39% beat

EPS. $0.84 | $0.89 | +5.95% beat

Before starting, it’s worth noting that Nvidia will hold its GTC conference starting March 17; this is where their next innovations will be shared.

Business.

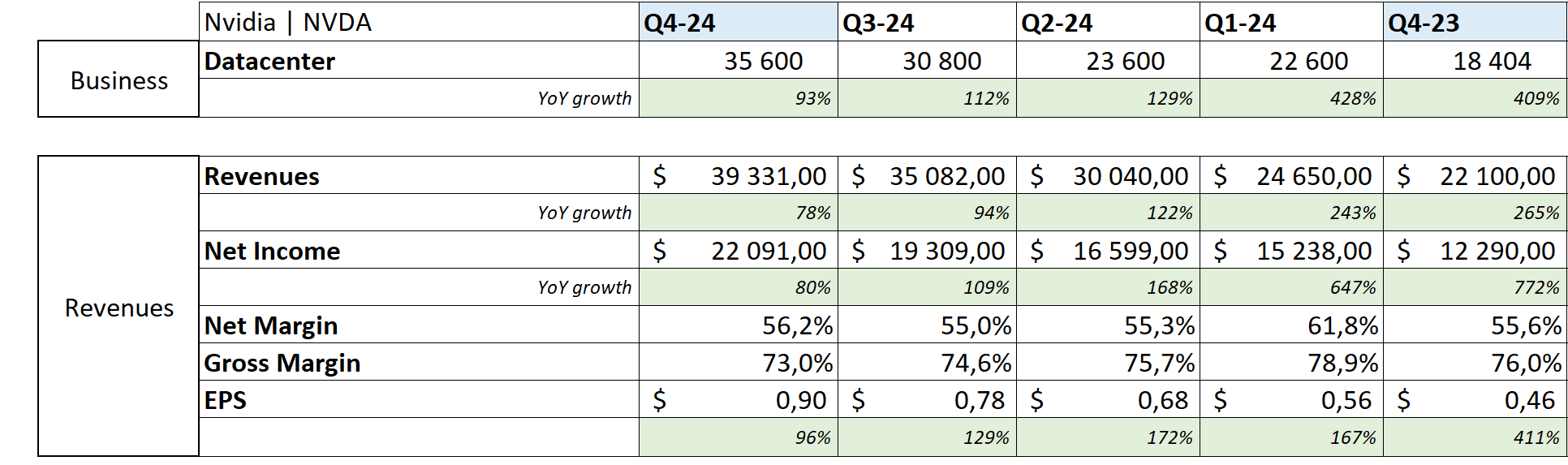

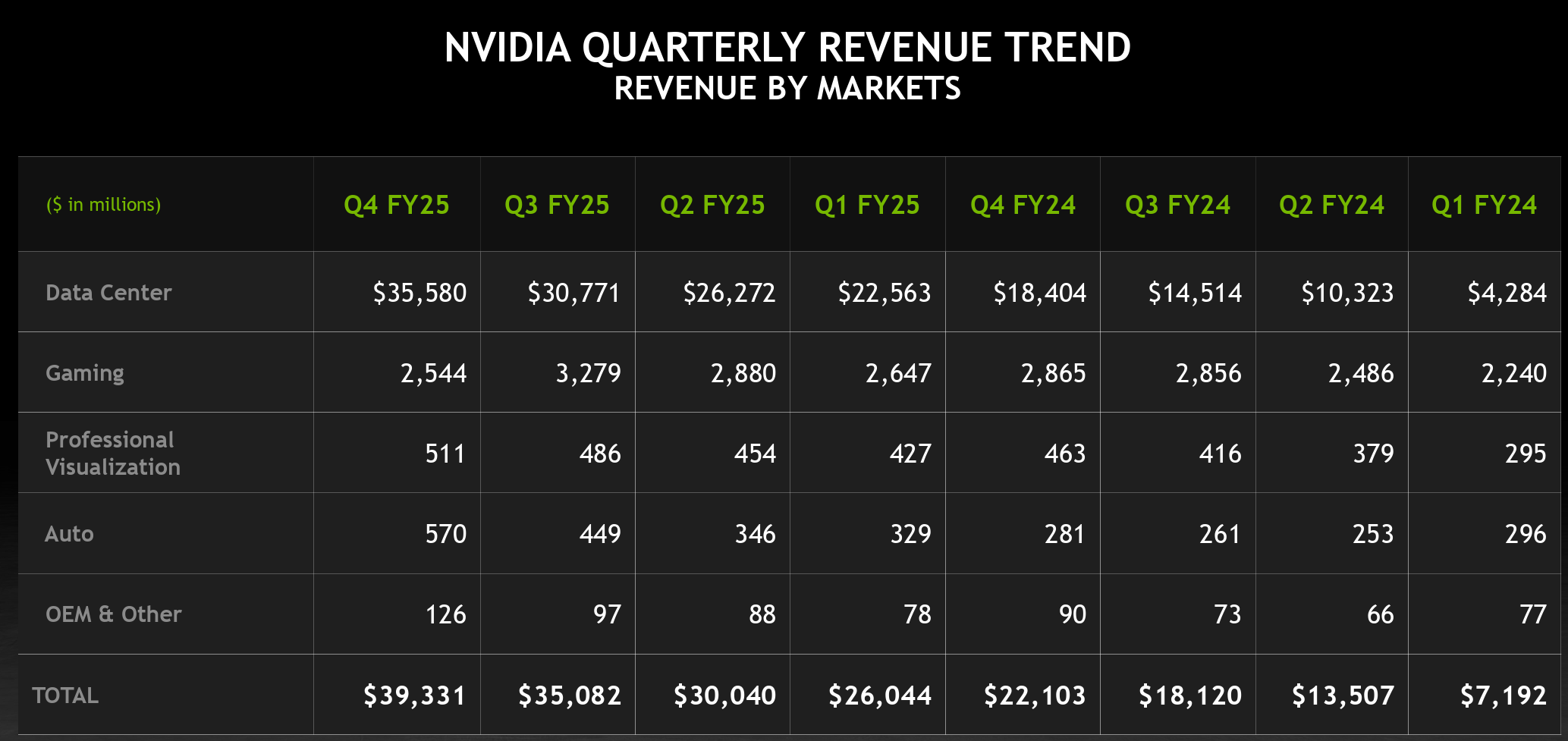

Here’s the big picture of what the company did this quarter & the previous ones for comparisons.

Let’s start with the most important before commenting some things on the rest.

Data Center.

Another record quarter for the company which did beat on revenues expectations by almost $2B. Blackwell was responsible for $11B of revenues or 30.9% of the total datacenter revenues, which shows that the need for those hardwares is real as AI advances in its stages.

“Post-training and model customization are fueling demand for NVIDIA infrastructure and software as developers and enterprises leverage techniques such as fine-tuning reinforcement learning and distillation to tailor models for domain-specific use cases.“

The first step was about building models & training them. The second step, which demands Blackwell, is about inference & reasoning which according to Jessen, “can require 100x more compute per task compared to one-shot inferences.” Their new hardware architecture is built to manage those new needs, pre & post training.

“Blackwell addresses the entire AI market from pretraining, post-training to inference across cloud, to on-premise, to enterprise.”

This shows the market & investors that DeepSeek sure was an important optimisation, but won’t change the need for computing power as the more the LLM is deployed & used or copied, the more computing power will be needed for post-training tasks.

“Future reasoning models can consume much more compute. DeepSeek-R1 has ignited global enthusiasm. It's an excellent innovation. But even more importantly, it has open-sourced a world-class reasoning AI model.“

This is where we are at the moment but we still have room to go further with tons of new potential applications for AI, in the logical world with new software methods.

“And then the long-term signals has to do with the fact that we know fundamentally software has changed from hand-coding that runs on CPUs to machine learning and AI-based software that runs on GPUs and accelerated computing systems.”

We’ve heard about this many times from Bryan, Airbnb’s CEO, who said that they’ll need to redevelop their app entirely to adapt it to AI rules as it won’t work as it used to. This will also require tons of computing power as most, if not all applications will need to be revamped on this model.

But also in the physical world with robotics - be it humanoid or autonomous vehicles.

“One of the early and largest robotics applications are autonomous vehicles where virtually, every AV company is developing on NVIDIA in the data center, the car, or both.”

Management estimates that the automotive vertical will reach $5B of revenues next year - from $1.7B today, as more compute will be needed to reach autonomous vehicles but also more companies work on their own systems.

We’re far from being done with computing power.

“The next wave is coming, agentic AI for enterprise, physical AI for robotics, and sovereign AI as different regions build out their AI for their own ecosystems.“

In terms of geographies, management mentioned the European projects of $200B to build AI infrastructures locally, part of which will need to go to Nvidia for computing power but also mentioned China where demand is rapidly growing but Nvidia cannot satisfy it due to export regulation - no growth to expect from there.

Revenues.

What is nice with Nvidia is that everything is simple.

Revenues grew 114.2% YoY boosted by the datacenter branch which is responsible for 88% of tthem. Gross margins are globally growing from 72% to 75% YoY although they fell QoQ as Blackwell is ramping & the company is focusing on delivering the product more than cost optimisation.

“At this point, we are focusing on expediting our manufacturing, expediting our manufacturing to make sure that we can provide to customers as soon as possible […] When fully ramped, we have many opportunities to improve the cost, and gross margin will improve and return to the mid-70s, late this fiscal year.”

A short-term bump to focus on growth.

The company closed the year with $34.6B of net debt and $60.7B of FCF while share count is flatish YoY.

Guidance.

The company only guides one quarter at a time but numbers remain strong.

We are talking about a 74% YoY growth & a 9.3% QoQ growth, obviously slowing down as comps get harder but still highlighting a strong & growing demand.

My Take & Valuation.

It is still impossible for me to not be bullish on Nvidia fundamentally and the stock remains on my top 5 companies to own based on fundamentals. They provide something no one else does & everyone needs.

And the need for it won’t slow down as it gets better & cheaper; on the contrary, like the demand for cars didn’t slow down while they got accessible to the mass. Everyone will eventually use, work on or consume AI products or services & every company will need to work with it in the future if they want to remain competitive or even relevant, software & hardware wise.

We also have use cases that we cannot foresee today, some of them with generated content & their usage for pre-training or many other physical applications which aren’t yet on anyone’s roadmap.

Bottom line: the business is fire & will continue to be.

The second question is about valuation though, as a fire business doesn’t mean a fired-up stock & the market actually didn’t react to the double beat & strong guidance - stock is flat pre-market. It’s hard to know why but valuation sure is a reason & concerns about continuation is another one.

I played some simulations & assumed an 8% QoQ growth during the next year which is pretty strong & probably above what will happen but I tampered it going into FY26 with a 2% sequential growth, which would bring us to a 2Y CAGR of 35%, so above my bull case while not being overly bullish, far from it.

Nvidia’s 5Y average P/S sits at x25 & its 5Y CAGR growth was at 35%. I wouldn’t base myself on this target to buy the stock as sure, CAGR is supposed to be equivalent but future growth will probably slow from there as comps get harder & demand will eventually stabilize - at one point.

It’s very hard to know what ratios the market is going to give Nvidia when it happens & I am on the team “sell-off” which is why I treat with caution on this name & focus on its implications, with my position on Nebius more than Nvidia itself because we’ve been running & expectations are now very different.

I’d love to own it for the long term, but my last purchase was only for a swing & I have strong convictions that we will be able to buy Nvidia cheap in the next years; that is when I will build my long-term position. For now, swing & observe is enough.

On another subject, this report shows that demand for compute won’t slow so soon & confirms my wish to own & grow Nebius, which reacted better than Nvidia as the stock is up 5% pre-market.

I am so very bullish fundamentally on Nvidia. But I am not so very bullish for its stock short to medium term. Market expectations & fundamentals are two very different things & today’s reaction shows that great isn’t enough. This is dangerous territory as risks become higher than potential rewards here.

Still holding my shares but I will take profits at the top of the range if we get there - I believe we will when the market finds its last bucket of optimism & pushes higher. Keeping in mind that cyclical stocks ALWAYS look cheap at the top.