Meta | Q4-24 Review & Call

Excellent, once again.

If you don't know enough about Meta or want to reassure yourself on how great the company is, everything you need is here.

Overview.

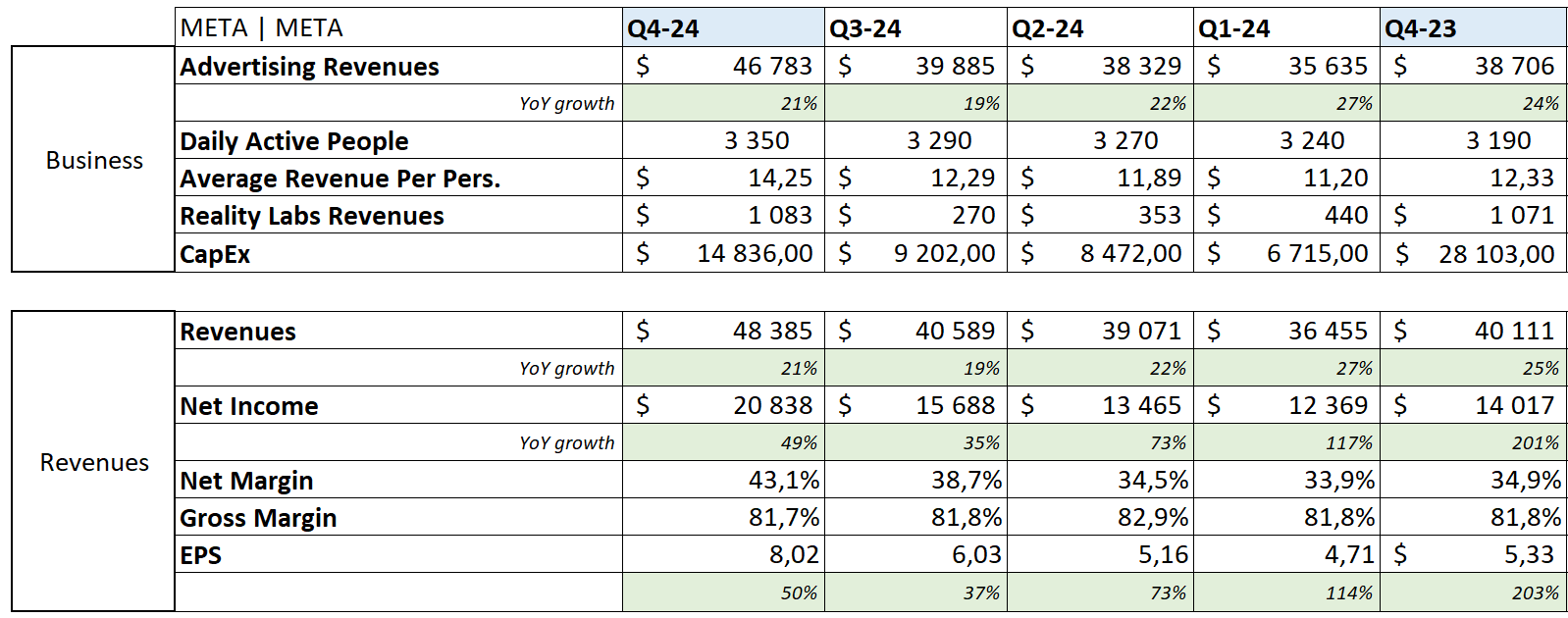

Revenue. $46.99B | $48.39B | +2.97% beat

EPS. $6.76 | $8.02 | +18.64% beat

$5.9B of buyback.

What more can we ask for?

Business.

As a reminder, Meta’s revenues come from advertising on their platforms, leveraging their users. Growth comes from three verticals: User growth, Engagement growth & Advertising pricing which grows with conversion rate.

Things unfold as usual in terms of users as the company is closing the year with more than 3,300,000,000 daily active users through all their platforms and sets one of its 25 targets to be that its AI assistant reaches 1,000,000,000 daily users. User growth is almost a given for Meta…

In terms of engagement & pricing, things are also pretty positive with a constant trend.

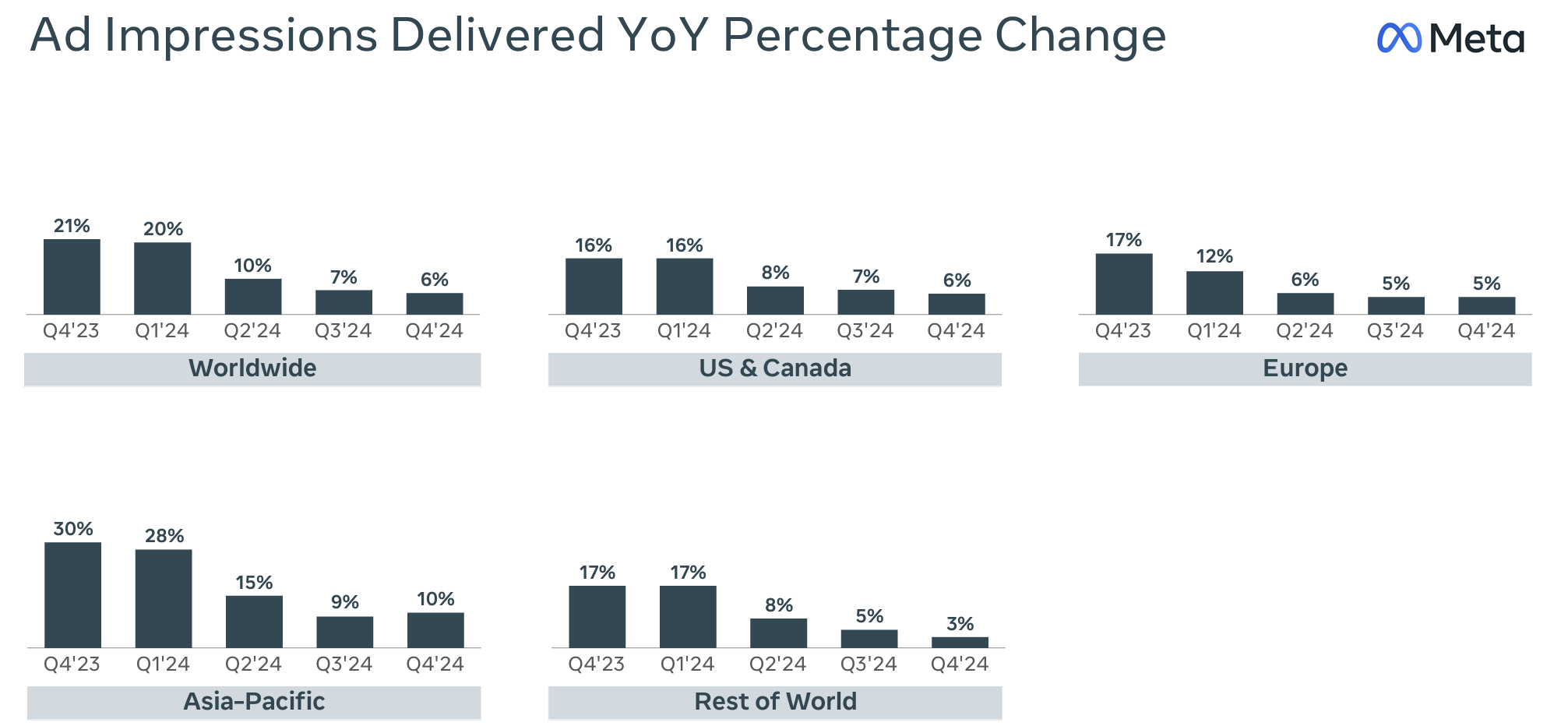

Impressions continue to grow regularly since Meta started its AI optimizations more than a year ago now. Growth is either stable or accelerating depending on the geographies.

Those three verticals are the focus of the company short term with different projects meant to optimize engagement & targeting with initiatives which have already “driven an 8% increase in the quality of ads that people see on objectives we've tested.”

Those kinds of improvements in user targeting & ads generation tools are demanded by advertisers as shown by the take rate growth from advanced packages.

“Adoption of Advantage Plus shopping campaigns continues to scale, with revenue surpassing a $20,000,000,000 annual run rate and growing 70% year over year in Q4.”

&

“More than 4,000,000 advertisers are now using at least one of our generative AI ad creative tools, up from 1,000,000 6 months ago.”

Constant improvement on that will continue to impact growth while Meta also has other strong verticals with Threads, Meta AI, Llama, WhatsApp & video content which either aren’t or are only starting to be monetized - plus its hardware R&D.

Those new verticals still need CapEx & talent to develop, the two priorities & biggest expenses source going into 2025. CapEx is probably the most important conversation, for Meta & for the broader market.

Meta confirmed its goal of investing between $60B & $65B through the year, mostly in data centers & high-tech profiles' compensations.

And this should continues as “These are all big investments, especially the 100 of 1,000,000,000 of dollars that we will invest in AI infrastructure over the long term.”

The DeepSeek story didn’t shake the team’s confidence in their need to spend nor in their methods. Open source remains their priority with reason as when it comes to LLMs, what matters is to have users, not technology. And Meta has more of them than anyone else.

Meta’s engneers will gladly look at what was done in the middle kingdome & adapt it to their models.

“And there are a number of things that they have advances that we will hope to implement in our systems. And that's part of the nature of how this works, whether it's a Chinese competitor or not.“

This shows once more how good this management is in my opinion. No ideology here, just opportunism.

To go further for the broader market, especially Nvidia, Meta confirms that this “break through” in training won’t change nor reduce the computing power needed in the future.

“That was already something that I think a lot of the other labs and ourselves were starting to think more about and already seemed pretty likely even before this, that like of all the compute that we're using that, you know, the largest pieces aren't necessarily going to go towards pre training. But that doesn't mean that you need less compute, because one of the new properties that's emerged is the ability to apply more compute at inference time in order to generate a higher level of intelligence and a higher quality of service, which means that as a company that has a strong business model to support this, I think that's generally an advantage that we're now going to be able to provide a higher quality of service than others who don't necessarily have the business model to support it on a sustainable basis.”

Only negative point is that where confidence was strong, there now is a bit of doubt in a few sentences Mark shared.

“And I continue to think that investing very heavily in CapEx and infra is going to be a strategic advantage over time. It's possible that we'll learn otherwise at some point, but I just think it's way too early to call that.”

But he remains bullish medium term.

I have to talk about Reality Labs as well, growing only 1% YoY while losses increased up to $5B this quarter. This includes developments with headsets, AI glasses & Orion which should yield returns in the future.

As usual from me, my take is that innovation requires investment. Not an issue.

On the Meta glasses, I’ve been a bit disappointed to be honest as growth is very slow while Mark talked in many interviews this year about a growing demand & how happy they were with the results.

Seems weaker than expected but those kind of things take time & the team remains very bullish on those going further - and I can personally understand the bull case of having intelligent glasses on your nose, seeing & hearing what you can see & hear.

We can talk a bit about politics as well as Mark highlighted the need to redefine their relations with government, as things sure change between Trump & Biden.

“Administration that is proud of our leading companies, prioritizes American technology winning and that will defend our values and interests abroad. And I am optimistic about the progress and innovation that this can unlock.“

Again, personal opinions shouldn’t matter when talking about investments & I’d just like to say that when you are the CEO of one of the companies with the biggest reach on any population, it’s important to have good relationships with governments, whomever is at its head.

Politics are important in its position, and it’s in shareholders' interest that the company adapts depending on who leads the country.

Financials.

No surprises here.

Meta closes the year with $164.5B of revenue & a 21.9% YoY growth and $62.36B of net income, a 59.5% YoY increase while net margins passed from 28% to 38%… Impressive, especially as there is no cheating here, everything comes from business optimization.

Some interesting points to note though. The R&D expenses growth come, as said above, from higher compensations to attract talent for their AI & hardware R&D. The tendency will continue through 2025 as tech talents become the priority for the company. The quarter also had much less G&A expenses due to legal fees cut.

meta closes the year with $77.8B of cash for $29B of debt & $43B of FCF & returned $35.2B to shareholders through the year.

Impressive.

Guidance.

No FY guidance but Q1-25 guidance is between $39.5B & $41.8B of revenues or between 8% & 15% YoY growth including currency mix.

Valuation.

Growth might slow down a little bit going forward as suggested by the guidance & I’d rather stay conservative as the next two years’ growth should “only” be driven by the company’s core business & its capacity to convert advertisers to better tools. Other monetization sources & hardware should kick in later on.

Assuming the company can keep its Q1-25 growth guidance through the next two years seems conservative, not overly optimistic. Holding the margins seems a given as revenue growth comes with higher take rate of higher margin products.

As with other Mag7, it’s very hard to call Meta expensive at today’s pre-market price. We’d need the stock to trade around $600 for a F.P/S on its 10Y average of x9.6 & at $680 for its F.P/E of x29, assuming a 2% share outstanding yearly reduction & not including dividends, which could lower slightly its fair price.

Anything above my growth targets would of course mean that Meta’s actual fair price is higher, so it’s up to each of us to use the assumptions we want.

In terms of price action, this brings my fair price perfectly on the ATH retest, broken after this earning release.

My Take.

There isn’t much more to say, everything is perfect & is even more impressive when you realize the potential leverage Meta still has for its future growth, with lots of verticals they can work on between their core advertising business & R&D…

Buying when the street was crying over CapEx turned out to bring really great returns - and to print the perfect bottom, as we’re now up more than 62% in less than a year on the position…

Fundamentals are rock solid, financials are rock solid, management is rock solid, valuation is pretty correct.

Lovely.