Meta | Q2-24 Earning & Call

The market is schizophrenic.

If you were to say the exact same thing at three-month intervals to a person, you’d expect them to react the same way, right - assuming nothing changed in between? Well, not if you tell it to the market, as this quarter seems to be a copy of the last, but the market now sees things differently - for the better.

Overview. Nothing changes for Meta; the company keeps on with its perfect business & execution.

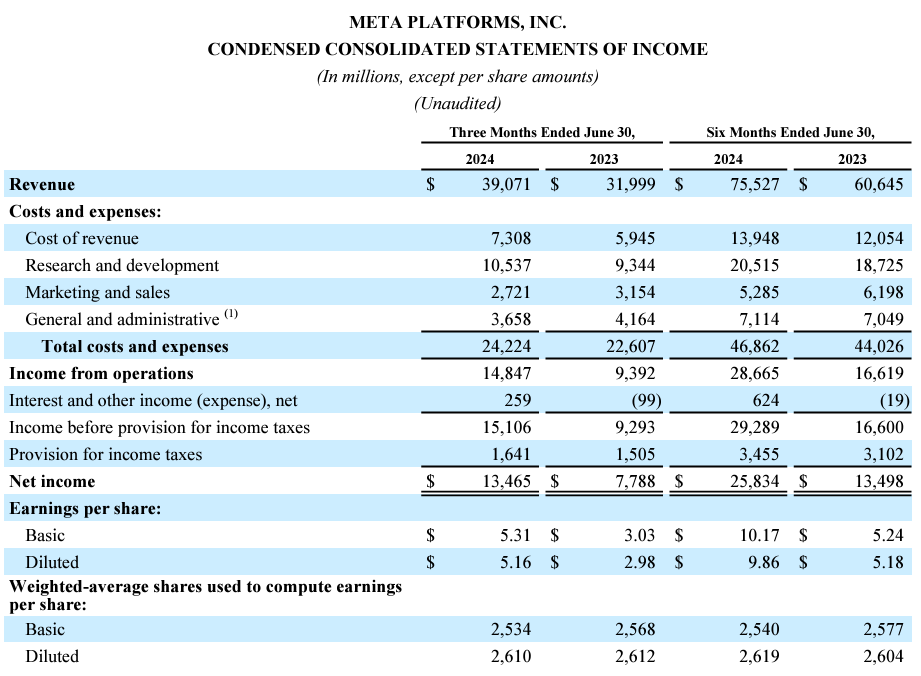

EPS. $4.71 | $5.16 | +9.55% beat

Revenue. $38.31B | $39.07B | +1.98% beat

$6.3B of cashback & $1.26B of dividends.

The overview shows how good a business Meta is.

Business.

Revenues continue to flow in as the company keeps its status as one of the best platforms to advertise on, strong with its social media with billions of daily users - 3.2B exactly this quarter. We’re talking about Instagram & Facebook as the most important ones but it’s worth mentioning that Threads reached 200M monthly users.

A pretty wide audience, which the company knows how to monetize, as the ARPP shows, constantly growing YoY to reach $11.89 this quarter, its highest ARPP ever - excluding the Christmas quarter.

The user base is growing, monetization is getting better, and their entire business is more & more efficient quarter after quarter, with ad impressions & prices per ad growing constantly.

“we got to the point where our ads system could better predict who would be interested than the advertisers could themselves.”

The first one’s growth is slowing as the company deployed its new AI tools some time ago and the initial growth spurt is behind but as advertisers realize the power of these tools, more & more are using them, growing the average price per ad faster than ever.

Business is booming thanks to major investments made months ago.

I’ll add a personal touch here as I’ve been noticing many more ads lately on Instagram, to the point where it kind of bothered me but then I thought, “What’s the alternative?” Most (if not all) of their user base will accept more ads as they can’t find what they find on Instagram anywhere else. Although this should also change as Meta gets better & better at targeting - because what matters is engagement, not only impressions.

“This is enabling us to drive revenue growth and conversions without increasing the number of ads or in some cases even reducing ad load.”

And as for Google, we had confirmations that Meta’s new AI tools are much, much better at targeting and driving bigger conversions when they are coupled with each other.

“We’re seeing those tools continue to unlock performance gains with a study conducted this year demonstrating 22% higher return on ad spend for US advertisers after they adopted Advantage+ Shopping campaings […] we began rolling out full iage generation capabilities into Advantage+ creative, and we’re already seeing improved performance from advertisers using the tool.”

There would be much more to say and to quote, but the summary is pretty easy: Meta’s user base is growing and its new advertising tools bring more impressions, better targeting & conversion on its applications’ users and therefore generate more demand from advertisers and more revenues with better margins for Meta.

What’s not to like?

AI. Much has been said about AI once more as Llama has finally been released, and Mark talked about the future.

“In the coming years, AI will be able to generate creative for advertisers as well […] Over the long term, advertisers will basically just be able to tell us a business objective and a budget, and we’re going to go do the rest for them.”

This is about the advertiser part, but Meta’s AI tools aren’t just about advertising anymore and will, in time, allow brands and influencers to use Llama to create personalized agents capable of answering any questions - the best selling & assistance tool ever.

“we’re not just creating a single AI, but enabling lots of people to create their own AIs […] every business is also going to have an AI agent that their customers can interact with.”

Capex. Whatever investors were scared about last quarter in terms of capex & expenses, this quarter made it worse. Mark and Susan didn’t go lightly and clearly stated that investments will be bigger and that returns on those will take time.

“The amount of compute needed to train Llama 4 ill likely be almost 10x more than what we used to train Llama 3.”

And about the returns.

“While we expect to come in over a longer period of time, we are mapping these investments gainst the significant monetization opportunities that we expect to be across customized ad creative, business messaging, a leading AI assistant, and organic content generation.”

And we’ve heard the exact same comment from Sundar during Google’s call.

“I’d rather risk building capacity before its needed, rather than too late, given the long lead times for spinning up ne infra projects.”

I said this many times already, but I’ll say it again: This is very, very bullish for computing power, hardware & IT cybersecurity companies - Hello Nvidia, Arista Network, Palo Alto & Co.

Any opportunity on those stocks will be bought on my end.

Reality Labs. No surprise that this portion of the company keeps losing money, but there is some good news on two fronts. Firstly, stronger demand than expected for the Ray-Ban glasses - they’re also pretty cool.

“Ray-Ban Meta glasses continue to be a bigger hit sooner than we expected. Demand is still outpacing our ability to build them.”

This won’t bring billions of revenues tomorrow, but it shows that there is a demand for this kind of product. A good sign for future ones. The Quest headset is following the same trajectory.

“”Quest 3 sales are also outpacing our expectations – and I think that’s because it’s not jut the best MR headset for the price, but it’s the best headset on the market, period.”

Take that Apple.

Revenues.

The company continues its perfect execution with revenues growing 22% for a billion-dollar capitalization company while costs only grow 7% YoY.

The progression is impressive, no need to make a drawing of why margins are growing that rapidely with such numbers… The company generated $10.8B of FCF and ended up the quarter with $40B of net debt.

A very strong position.

Guidance.

Nothing short of expectations, as we are talking about revenues between $38.5B & $41B, a slower growth but a significant one still, with Capex continuing to grow for the two next quarter to reach at least $37B at the end of the year.

My Take.

Exactly like last quarter, there is nothing bad here and everything just makes me wanna buy more - urges which I try to refrain.

Meta is run by smart people who think long term and everything they do isn’t for the next quarter but for the next decade. They have proven repeatedly their capability to do well and to adapt if needed - changing focus from the metaverse to AI very rapidly and not missing the train for example, while others did (I won’t name Apple here, that would be mean).

Investing as much as they did in their own infrastructure is going to bring returns; it will just take time, but they are aware of the importance of being able to adapt and said repeatedly that they will be able to use this hardware for other means if necessary.

They know what they’re doing, they know their business, they have the strongest position in the entire social media sector and as of today, cannot be challenged.