Meta Q1-25 | Earning & Call

As strong as usual.

If you don’t know about Meta & why I personally consider it to be one of the best company on the market, you’ll have everything detailed here.

Overview.

As strong as usual.

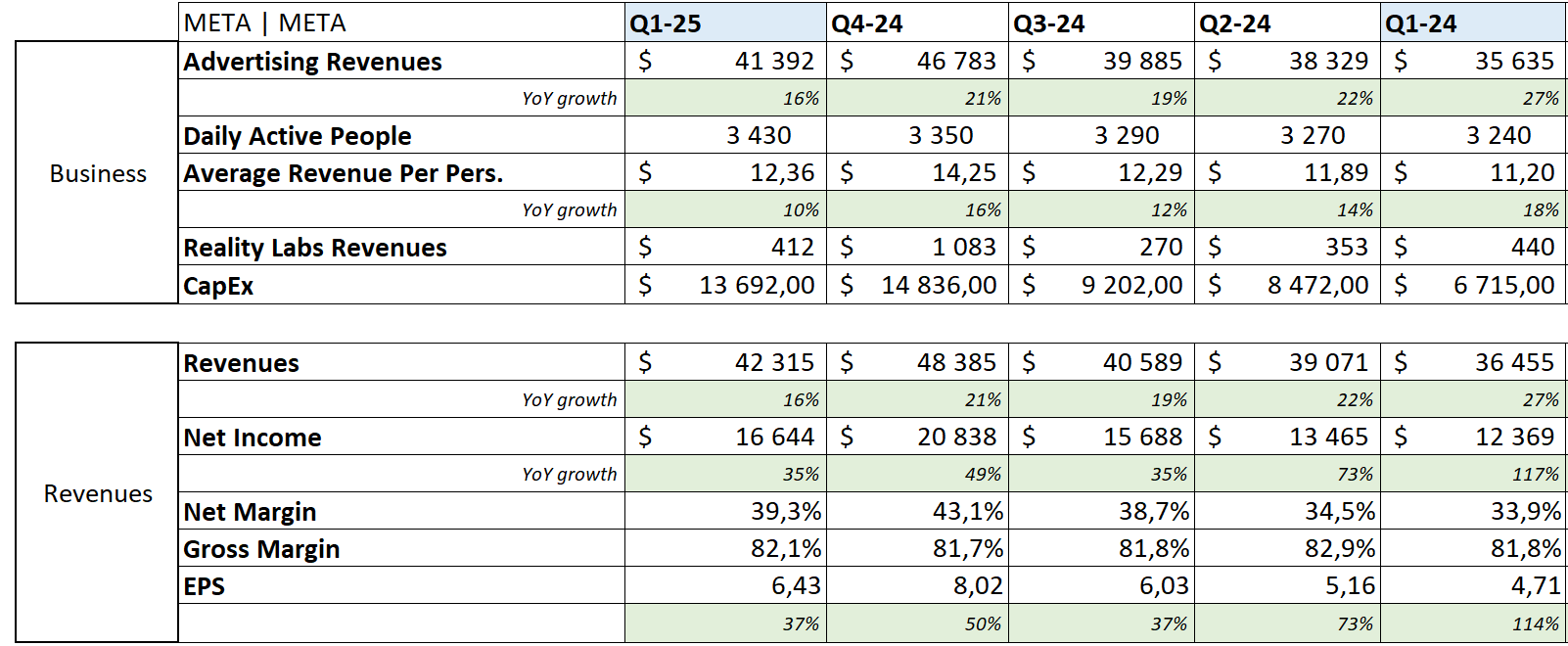

Revenue. $41.38B | $42.31B | +2.26% beat

EPS. $5.28 | $6.43 | +21.78% beat

$13.4B of buybacks & $1.3B of dividends

Business.

Meta continues to find new users & please them with 3.43B daily active users & a constantly growing time spent on their apps.

“In the last six months, improvements to our recommendation systems have led to a 7% increase in time spent on Facebook, a 6% increase on Instagram, and 35% on Threads. Threads now also has more than 350 million monthly actives [users].”

Growing user base & time spent also means more potential spots for advertisers. Also important to note that Threads isn’t optimized for monetization yet as management focuses on improving the platform. They also released their AI standalone app which is meant to become a personal agent, fed from their users’ interactions & interests on their other platforms.

“In addition to building Meta AI into our apps, we just released our first Meta AI standalone app. It is personalized, so you can talk to it about interests that you've shown while browsing reels or different content across our apps“

Your virtual best friend who knows everything about you.

Monetization continues to improve with a growing average revenue per user.

More users. Better monetization… I could end this report here as the most important is said. Yet, there still are more positives.

In how they advertise first. The company’s system became so good at creating & targeting customers that they almost don’t need input from advertisers anymore.

“Our goal is to make it so that any business can basically tell us what objective they're trying to achieve like selling something or getting a new customer and how much they're willing to pay for each result, and then we just do the rest. Businesses used to have to generate their own ad creative and define what audiences they wanted to reach, but AI has already made us better at targeting and finding the audiences that will be interested in their products than many businesses are themselves, and that keeps improving. And now, AI is generating better creative options for many businesses as well.”

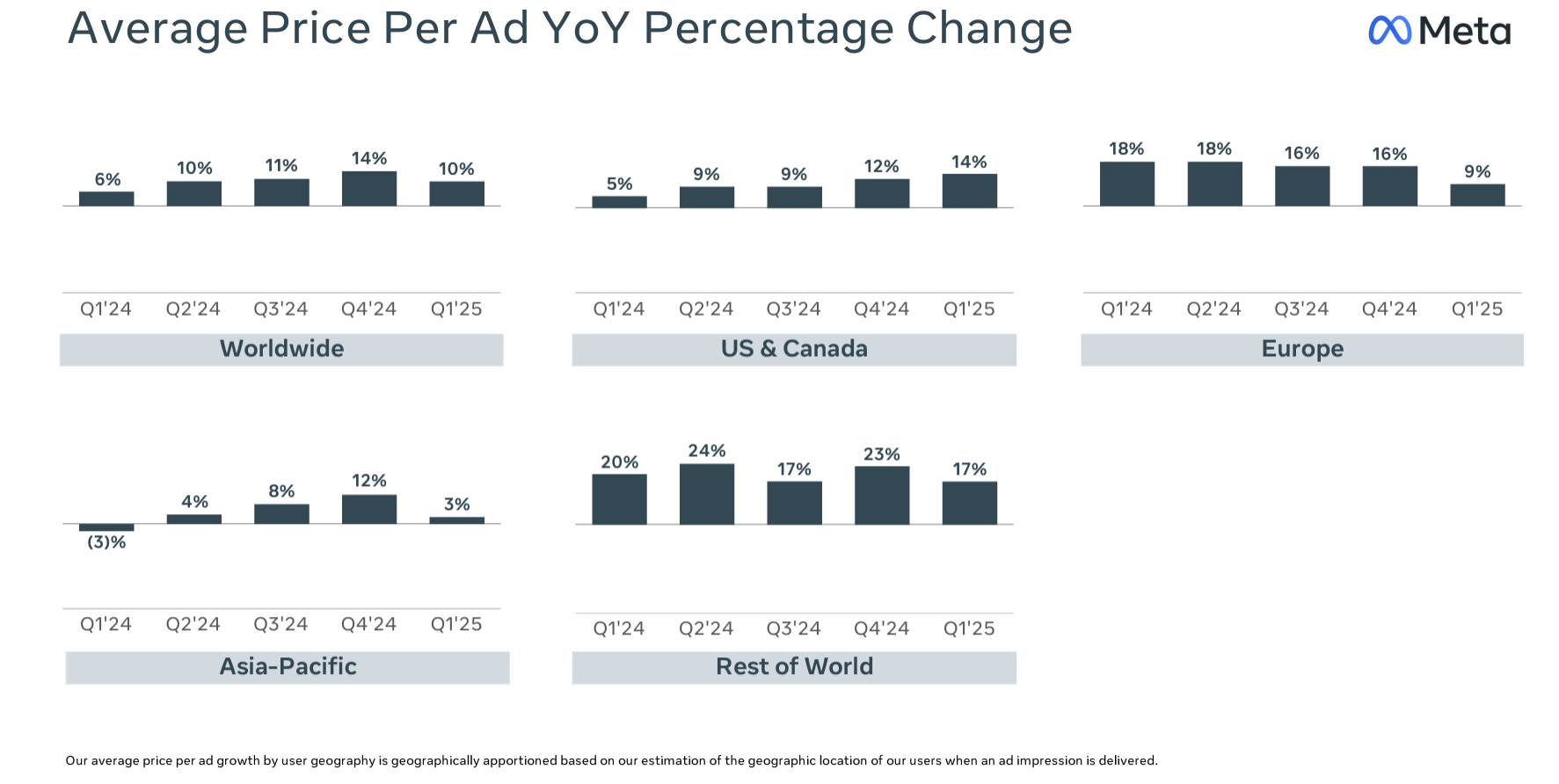

This is why Meta remains one of the biggest advertising platforms: their user pool but also their high-end advertising technology, which ends up being more expensive as the company delivers better results.

This constant quarterly double-digit growth in price per ad is due to the quality & results of the service but also of the volume as more advertisers use Meta’s tools.

“In just the last quarter, we are testing a new ads recommendation model for reels, which has already increased conversion rates by 5%, and we're seeing 30% more advertisers are using AI creative tools in the last quarter as well.”

&

“Pricing growth benefited from increased advertiser demand, in part driven by improved ad performance.”

Improvements continue to roll in & more advertisers demand to be part of it.

On verticals & geographies, e-com remained a very big portion of their revenues & growth came mostly from rest of the world, with a 14% & 12% growth from Europe & Asia. I would remain cautious on the next quarter with tariffs clearly slowing down consumption hence advertising.

Meta should benefit from a rotation of advertisers - like Google, as new verticals will take the spots left by others - potentially e-coms. Hard to know to what extent and if total volume decrease pricing also will. We’re in for some volatility and troubles began at the start of Q2, hence aren’t seen yet. It doesn’t seem to be what management saw until today though.

“But our Q2 outlook reflects the trends we're seeing so far in April, which have generally been healthy.”

Despite this personal assumption, there are some troubles with European regulations which should force Meta to change their subscription plans & their advertising models in the region.

“Based on feedback from the European Commission in connection with the DMA, we expect we will need to make some modifications to our model, which could result in a materially worse user experience for European users and a significant impact to our European business and revenue as early as the third quarter of 2025.”

Everybody loses but politicians are happy. This could impact Meta’s revenues in the year to come as Europe represents 16% of their FY24 total revenues. Appealing the decision will take time and won’t guarantee anything - it is hard to win against bureaucratic institutions.

Meta is already working on AI’s next step which can be resumed by AI Agents, with their new standalone AI app. Management’s vision is pretty straightforward.

“So in the next few years, I expect that, just like every business today has an email address, social media account and website, they'll also have an AI business agent that can do customer support and sales, and they should be able to set that up very easily given all the context that they've already put into our business platforms.”

My bull case remains the same: Meta has 3B+ users & every company in the west has an account on their platform. Why wouldn’t they use their AI agents?

About their hardware products, I also am very bullish on the AI smart glasses & their future version & agree once more with Mark that glasses are the perfect accessory to integrate AI on seamlessly.

“They enable you to let an AI see what you see, hear what you hear, and talk to you throughout the day, and they let you blend the physical and digital worlds together with holograms. More than a billion people worldwide wear glasses today. And it seems highly likely that these will become AI glasses over the next five to 10-years.”

The Ray-Ban Meta AI glasses have apparently tripled in sales YoY - starting from a very low point though, with great satisfaction.

“Moving to Reality Labs, we're seeing very strong traction with RayBan Meta AI glasses with over 4 times as many monthly actives as a year ago, and the number of people using voice commands is growing even faster as people use it to answer questions and control their glasses.“

It still remains a very small portion of their revenues but the potential is here.

For once, the market didn’t react harshly to the Capital Expenditure forecast, which was raised from between $60B & $65B to $64B & $72B, a 8.8% increase.

“This updated outlook reflects additional data center investments to support our AI efforts as well as an increase in the expected cost of infrastructure hardware.“

We knew that Meta intended to continue to invest but confirmations are important, especially as they meet other hyperscalers in the narrative that they do not have enough capacities today, which means the trend won’t slow down.

“So even with the capacity that we're bringing online in 2025, we are having a hard time meeting the demand that teams have for compute resources across the company. So we are going to continually invest meaningfully here across our infrastructure footprint, but we are also really looking to build this capacity in a way that gives us the maximum flexibility in how and when we deploy it over the coming years.”

We had lots of other confirmations through the call but I won’t copy them all. Meta is committed & believes it is critical to have their own infrastructure, which means they will continue to invest.

This is pretty good for Nvidia, Arista Networks & co which I talk about regularly as my go-to stocks for AI infrastructure. We also have to consider AMD on which Meta relies on & intends to rely more to run its inference at low latency - critical for AI chatbots.

I’ll keep an eye on all those names for you.

Financials.

Nothing but perfection.

Strong & constant revenue growth - up 16% YoY, but most importantly, an excellent & optimized expense management as total costs only grew 9.3% despite strong R&D growth - balanced by G&A decline due to lower legal costs, which results in higher margins globally, higher EPS combined with the company’s massive buybacks & more cash generation - $10.33B of FCF, hence an insane balance sheet of $70.23B cash & $42B of net debt.

Guidance.

Management gave itself lots of room for the next quarter with a very large guidance, ranging from 9% to 16% YoY growth.

“We expect second quarter 2025 total revenue to be in the range of $42.5-45.5 billion. Our guidance assumes foreign currency is an approximately 1% tailwind to year-over-year total revenue growth, based on current exchange rates.”

Many companies are completely lost in the actual political landscape so we can’t blame them but will need to wait & see.

My Take & Valuation.

Meta remains strong, no doubts here. Business is booming & certainly won’t stop as even the worst recession won’t impact its network effect, nor the time spent on their apps, nor their advertising systems to improve... It sure can reduce total advertising spending but in time, nothing will really change. Except that they will be better at everything they do when it comes back.

This is why Meta is one of my top 5 favorite stocks & a blue chip I only accumulate as long as the price is below what I believe to be an optimum buying price for a long-term position.

This model assumes a 10% & 12% CAGR growth until FY26 & FY29 respectively, 42% of net margins, 2% of returns to shareholders & multiples equal to Meta’s 5Y average at x25 earnings & x7 sales.

I remain overly bullish for Meta’s next decade and really want to be part of it. The next year could be a bit challenging due to the reasons shared above but I will not mind accumulating this name & accept a paper loss, until the economy & politics turn around, as I am pretty convinced Meta will be stronger by then.