Lululemon | Q3-24 Review & Call

Patience paid.

If you don’t know about Lululemon, you will find everything you need right here.

Overview.

In a few words, this quarter was pretty good.

EPS. $2.72 | $2.87 | +5.51% beat

Revenue. $2.36B | $2.4B | +1.57% beat

$409M of buyback.

Yup, as good as it looks.

Business.

This quarter wasn’t very surprising, bringing what I was expecting from it: a strong international market - growing 33% YoY, with continuous stability in the U.S., which means no growth for the second quarter in a row.

What’s even more interesting is to look at the comparable sales - YoY comparison of stores which have been opened during the last 12 months.

Half of the internationnal growth came from new stores, confirming strong demand, great planning & execution from the company. The more poened stores, the faster the company should grow - based on this sample.

And that is what they intend to do, starting with an expansion to Mexico with 15 new stores, which were not included in previous guidance, an more.

“Our plans for 2025 include opening in Italy as a new company-operated market, and in Denmark, Belgium, Turkey, and the Czech Republic under a franchise model.”

Newness.

This is their biggest problem in America: Clients come to spend but couldn’t find the perfect product for them. Newness had fallen to historical lows, and management has been working to change this, with a target goal to be back to normal levels by Q2-25.

“When looking at the composition of our assortments, we are on track with our efforts to increase the penetration of seasonal newness and expect to be in line with historical levels in quarter one 2025.”

The time target has shortened, which is already a great sign, and clients have already responded positively to the first steps taken by management, with growth in newness consumption during the quarter.

“we are very pleased and seeing a good guest response to the newness that we put in.”

Focus on America.

Briefly, as you know by now I am not really bullish in the medium term. Let’s start with the positive points, with a strong Black Friday - which was true globally, not only for Lululemon.

“In fact, on Black Friday, we had the most visits ever to our shop app and e-commerce site.”

But besides this one-time event, traffic remains correct, without strong growth, or nothing significant enough for management to be positive about it.

“And in terms of the U.S. specifically, e-com channel remains positive, and our stores were slightly lower than last year.”

There were a few more comments during the call where they expressed rapid concern about the “macro environment” without saying it was bad or degrading, but without sharing optimistic views either.

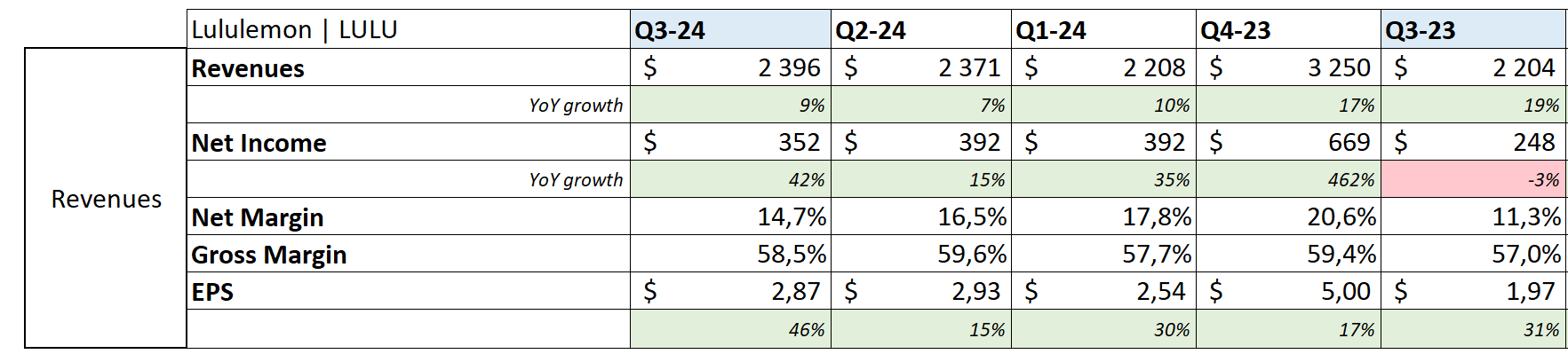

Revenues.

Numbers reflect the good quarter & the improvements.

The quaterly 9% YoY growth is followed by an 8.8% YoY growth for the nine months ending, which is pretty great considering the challenges faced, especially in America. The biggest opportunity remains in international markets and management is laser-focused on those as well, so everything points to even better days.

Execution is also very good with flat/slightly improving margins, helped on the net margins comparison by the impairments expenses in 2023, but still improving, even deducting it. This, combined with a great buyback strategy leads to growing EPS & happy shareholders. Balance sheet & FCF remain very healthy.

Guidance.

I’ll start with management’s words, which reflect my own perception of the actual U.S. economy.

“But given fewer shopping days between Thanksgiving and Christmas and an uncertain macro environment, we continue to plan the business prudently.”

Nevertheless, management is guiding to between $10.45B & $10.48B, which represents 9% growth YoY with a strong impact from currency mix & the actual strength of the dollar - if it remains that way.

Q4-24 is guided between $3.475B & $3.51B, a low range YoY growth of 8%.

My Take & valuation.

Lululemon is bringing everything shareholders wanted - at least I. A constant & even acceleration in international growth with an aggressive policy of expansion. A stable U.S. market while rapid actions were taken to answer their newness issues, already showing results. Combined with positive guidance & strong words on the future of the brand & company.

“We remain committed to delivering on our Power of Three x2 revenue target of $12.5 billion in 2026, and we remain ahead of schedule.”

As a reminder, reaching this target requires around 9% CAGR by 2026, which would yield our 11% returns on investment if the stock trades at 5.5x sales by then - a correct but not a cheap, or around 30x earnings which again, isn’t cheap but isn’t excessive either - while my assumptions do not include buybacks.

I am not a buyer anymore at these prices as the margin of safety is reduced, but I am holding and feel very positive about the future, while keeping an eye on the U.S. economy, which remains correct for now. As long as it does, I am pretty bullish for Lululemon’s future.