Lululemon | Q2-24 Earning & Call

Weak but encouraging.

If you do not know much about Lululemon, everything you need is here.

Overview.

A pretty correct quarter altogether considering actual valuation, with lots of encouraging data & insights.

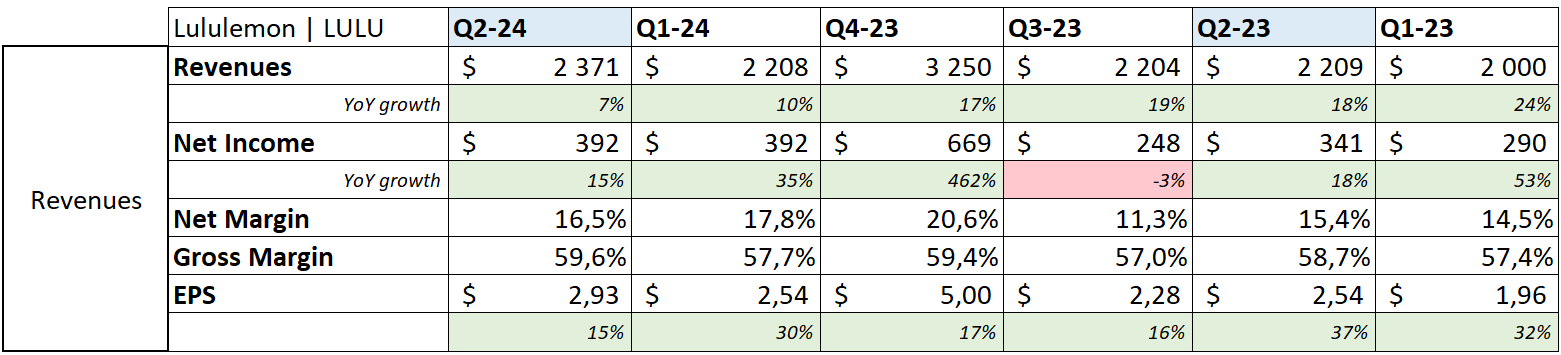

EPS. $2.93 | $3.15 | +7.51%

Revenue. $2.41B | $2.37B | -1.62% miss

$583.7M of buybacks.

"Looking ahead, we feel confident in the long runway in front of us as we execute on our Power of Three ×2 growth plan."

The rapid overview is more than correct despite a tough environment & consumers.

Business.

A lot of things to say about the business this quarter as management gave lots of valuable information.

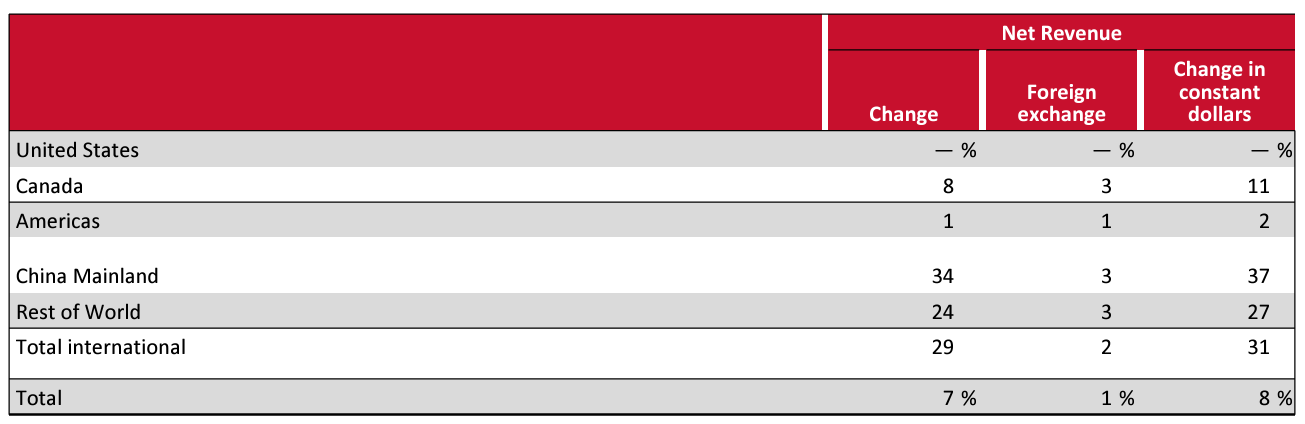

Geography.

Let’s start with the positive notes, the strong growth coming from the international branch of Lululemon, with weakness only coming from the U.S., the bigger part of the company’s revenues.

The infographic says it all, we’re talking about +34%, +24%, & +8% revenue growth in the different regions while the U.S. is flat YoY. There also is a big difference in revenues & comparable sales as the last data is down -3% in the U.S. while up +21% & +17% in China & RoW respectively, which shows strength in the stores opened in the last 12 months as those aren’t included in this data, most of them being opened in China & RoW.

The strategy of international growth is working, working well, and management is very confident in it.

“we remain on track to quadruple international revenue from 2021 levels by the end of 2026.“

We’ll talk about this more a bit further.

Strategies, Problematics & Resolutions.

Branding Strategies.

Things are going well internationally thanks to lots of initiatives taken those last quarters to grow brand awareness in those regions, notably in China through the company’s involvement in the “Healthy China 2030 initiative” or the “Summer Sweat Games” which attracted more than 10,000 participants.

These events’ success is incentivising the company to export them and hold similar ones this fall in South Korea, Germany, the U.K., and the U.S., hopefully bringing the same positive results.

Newness. The biggest issue this quarter is about growth in the U.S. Data is pretty good when it comes to frequentation with a strong brand awareness & retention.

The problem comes with conversion in women, with lots of them leaving the stores & websites without purchases. An issue management identified & labeled newness.

“By newness, I'm referring to the seasonal updates we bring into the assortment, typically expressed as color, print, patterns, and silhouettes. I'm not referring to our pipeline of innovation, which remains full, and the details of which I will share with you shortly.”

This is about growing consumption, proposing the same products with different colors & shapes, not new products. Lots of women already own Lululeon’s products and are looking for equivalents one with different colors or motifs, and that is what lacked this entire semester in America.

“The newness we had sold very well. Guest was coming in, traffic was positive across all channels, and the opportunity was in conversion. So, I see that as an opportunity that they were there with intent to spend, and there was a noticeable reduction in those historical levels of newness.”

The takeaway is that many consumers didn’t find what they wanted, which is a problem as it can drive customers to competition - namely Alo. Management reacted to remediate the situation and expects to have enough newness ready for the second half of next year, hence a probable similar impact on Lululemon U.S. for the few next quarters.

Innovations. Besides newness, innovation is going well with lots of products in the pipeline and very strong demand for them.

“we saw strength across the assortment, including Zeroed In, which was launched this past spring and has quickly become a guest favorite and a top three performance franchise.”

Management also talked a lot about a new fabric they used for hot weather sport practice called “Breeze Through” which didn’t work at all, but again, shows the strong focus the company is putting on Asia, the principal target for this kind of product, used in hot & humid atmospheres. It also shows a wish to innovate & propose new things, even if it doesn’t always work.

“We're really excited about the guest response, not just in North America but actually internationally, in particular, in our APAC market, where this fabric was really designed, as I shared, for hot yoga. But we see it as versatility in high humid environments for a variety of activities.”

The teams are still working with it and will come back in the next years with a new product, hopefully more adapted to demand.

Membership Program. We talked about this a few times already, a pretty important part for any brand as it gives consumers a feeling of belonging through exclusive events, for more than 20M members now.

“In early June, we hosted a members-only weekend at Peloton Studios New York. This exclusive sold-out event featured live classes, a 5K run, sessions with our Peloton ambassadors, and a wrap-up party. We also launched partner perks for members. And the early feedback from guests has been very positive.”

Personal Take. I’ll share a rapid opinion on those different subjects because they all show how reactive and smart management is. They work to collect valuable data, try to target the problem, launch initiatives very rapidly, reiterate when it doesn’t work and aren’t scared to try things.

“In terms of the action plan that we put in place and the teams have been working on that, as I alluded to, I think coming out of Q1, we saw some opportunity. The learning in Q2 was the missed opportunity in silhouettes, which was new news for us, as we continue to analyze the business. And the teams have, through that action plan of chase, have been pulling forward and going into deeper on inventory that had been purchased, that we're seeing the guests respond well to as well as fast-tracking some designs. The chasing into will sequentially get stronger, and we will see that improve through Q3 into Q4.”

Collect data. Identify an issue. Propose a solution. Repeat.

This is a very hard & long process when you’re talking about retail sportswear, but Lululemon is doing it pretty well, and this is surely what helped them hold proper quarters in the last year.

Power of Three x2.

Let’s talk about the long-term vision of management & their different plans which are:

1. Double their revenues to $12.5B by 2026, launched in 2021.

2. Quadrupling revenues of the international branch from 2021 to 2026.

Management confirmed that they’re still on track to achieve both on time, and when listening to calls & guidance, they could even go even further if the economy stays strong.

If we were to extrapolate a bit, the FY-24 guidance is around $10.37B. With the company’s goal to reach $12.5B by 2026, it needs to grow 9% per year, while YoY growth FY-24 should only be at 7.8% with actual guidance, a bit under expectations mostly due to a temporary weakness in the company’s bigger market: America.

This will require pretty strong international growth, and that is where Lululemon’s potential is, as quadrupling international revenues from 2021 to 2026 would mean reaching $4B by then, while the company ended FY-23 with $1.99B. A need for a 26% CAGR during the next three years, lower than actual growth.

It would mean a revenue of $8.5B in north America by 2026 or a 3.7% YoY growth from 2023 to 2026.

This is where the actual weakness is, and the stronger growth in China & RoW doesn’t compensate yet. But as management said, this international growth should continue and remain strong while measures are taken in America, with a potential return of growth H2-25.

Those targets are far from unreachable be it with a return of growth in the U.S. next year or by a bigger than expected growth from the international section - which is the case at the moment.

Revenues.

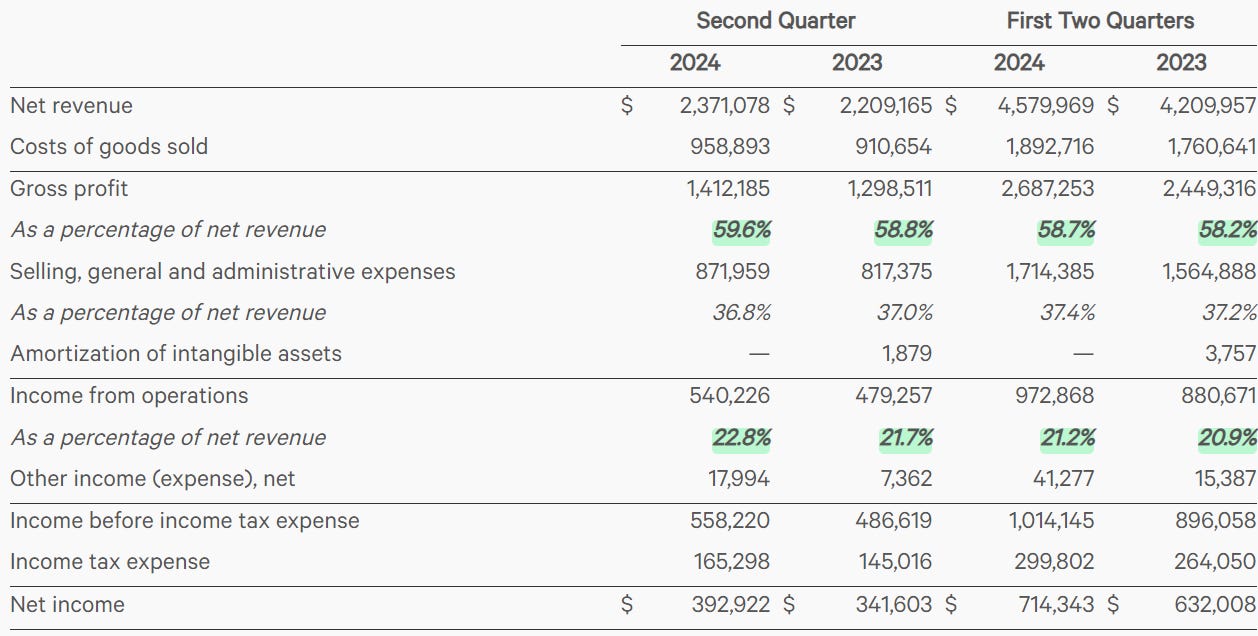

As said, the actual environment is pretty tough and this 7% revenue growth is correct in my opinion, with a pretty strong 18% YoY increase in EPS, much stronger than many expected thanks to better margins & buybacks.

Margins should be a big talk during this quarter as both gross & net margins grew YoY in a much more difficult macro environment. This shows strong management decisions and very, very good execution and this is, in my opinion, the most important data of this quarter, a proof of the company’s quality.

In terms of balance sheet & cash flow, the company ended the quarter with $1.6B in cash for no debt & $1.46B in lease expenses while the business generated $570M in cash & $425M in FCF, a pretty strong position.

$583.7M was spent on buybacks with an average at $310, a very fair price in my opinion, an efficient use of cash. The company has $1B left on its current buyback plan and I was kinda surprised not to have a new plan announced, although they still have enough firepower left for now, enough to buy back 3% of the company at current valuation.

Guidance.

The quarter was pretty weak in terms of revenues & growth without any doubts; also, business news is very positive, but this weakness should persist a bit longer and that is what is shown with this guidance.

The company reduced FY-24 revenues between $10.37B & $10.47B, or a growth of 8% YoY, which is still correct and within expectations, especially in a complex macro environment. Same for EPS expectation reduced between $13.95 & $14.15 compared to expectations between $14.27 & $14.47 last quarter.

The Q3-24 guidance is also weakish with revenues between $2.34B & $2.36B or a 6% YoY growth with EPS between $2.68 & $2.73.

My Take.

This quarter is showing some good & some weakness but I really want to talk again about the quality of the company’s management as this is the most important take away from this quarter. It still isn’t a good quarter, far from it, but it is in line with what most were expected.

In terms of valuation, I’ll change a bit my way of doing and only base my assumptions on two case: realizing the long-term Power of Three plan x2 & not reaching it, which are in my opinion pretty conservative expectations as RoW & China growth is stronger than needed to reach it, and growth in America should restart next year, probably ending up reaching expectations by 2026.

Yet, even then, I reach this kind of result, without taking any shares buyback into account.

At today’s price, we’d reach our 11% return with a 5% margin of safety with “only” x23 of PER and a very correct P/S, if the company were to succeed in its long-term play while keeping its actual net margins. Even if we were to fall a bit behind the plan, we wouldn’t need astronomic ratios to have our returns.

This is what I call an undervalued company and a pretty good price to buy if my assumptions turn out right by 2026, and this quarter seemed to point towards it.