Lululemon | Q1-24 Earning & Call

If you don’t know about Lululemon, here’s what you need.

Overview. We finally had the results of the first quarter and they are pretty good. Much better than what the street expected which confirmed my view that the beating was unjustified. Growth is still slowing as the company is becoming bigger and bigger, but it doesn’t justify the low multiples the stock traded at the last weeks.

EPS. $2.39 | $2.54 | +6.28% beat

Revenue. $2.20B | $2.21B | +0.41% beat

$297M buybacks | $1B new buyback program.

"In the first quarter, we saw strong momentum in our international markets, demonstrating how our brand continues to resonate around the world. Looking ahead, we continue to have a significant runway for growth and are confident in our team’s ability to powerfully deliver for our guests in 2024 and beyond."

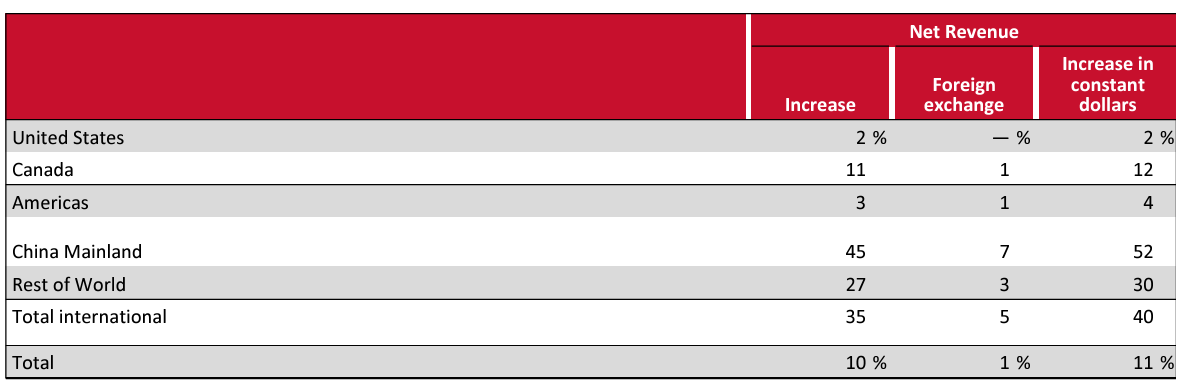

Business. We already talked about the company’s expansion and how they were aggressively opening shops overseas, mainly in Asia. Those places are where their next growth spike would come from and where competition is less present. Vuori, for example, is being sold through Chinese e-commerce apps (notably Alibaba’s Tmall), but they do not have many shops opened there - the first one was opened this year compared to more than 120 for Lululemon.

Brands are a big deal in China as they reflect status and Chinese love to show theirs, so any premium brand has a very big market to address there and that is what Lululemon has been focused on. A bet which is paying off as growth in those regions is really, really strong with China’s mainland revenue growing +52% and RoW growing +30% on a dollar basis.

This is where growth comes from now. Lululemon’s management saw the opportunity and is making it work, big time, as international now represents 26% of the company’s revenues compared to 21% in FY-23. And the management won’t stop there.

“I see the potential for it to grow to 50% as we continue to expand our presence outside of North America.”

Besides geography, growth has been good for every product Lululemon is selling as women’s increased 10% YoY, men’s products increased 15% YoY and accessories increased 2% - while comparing to very, very strong results last year. Yet, management speaks of what could have been better, especially in the women’s market.

“we've seen a slower start to the year due to several internal factors including missed opportunity in women's and bags, which we are actively addressing, and some ongoing choppiness in the consumer environment.”

While the men’s market still holds a strong potential.

“Our market share gains were strong in men's in Quarter 1, and with unaided brand awareness of less than 20% in the U.S., our opportunity to continue to grow this business remains significant.”

“we had some missed opportunity really, in our color palette, in particular in some of key categories such as our legging business, where we didn't have enough color, newness […] we [also] came into the year with some missed opportunity across our size profile, particularly our smaller sizes.”

I like it when a management is able to identify and publicly talk about what didn’t go well. It shows that they are entirely aware of it and understood their mistakes - and won’t do them again.

“All of this is within our control [...] and we expect much of that to be addressed in the second half of this year”

In terms of stores, not much changed as the company ended up its quarter with 711 stores, like in Q4-23 as they opened 5 new ones and closed 5 old ones, but the growth trend should continue during the next quarter.

“We continue to expect to open 35 to 40 net new company-operated stores in 2024 and complete approximately 40 colocated optimizations.”

More than 70% of those new stores are set to open outside of North America, another proof of the international focus.

Revenues. Everything is going well financially for the company, as strong as usual with double digit growth YoY & strong profitability

Growth margins increased 20 points YoY thanks to a combination of good factors but operating margin decreased 50 points and net income growth YoY is positively impacted by the bills held by the company. Higher interest rates and a bigger cash pocket result in more income.

The company ended its quarter with a strong balance sheet and a net debt of $750M and decreased its inventory by -15% YoY.

Guidance. The FY-24 EPS were risen to $14.27 to $14.47 or a net income of $1.8B - hence a net margin of 16.8% FY-24 in the lower case. Those would be strong numbers YoY and allow the company to return lots of value to shareholders with a proper growth.

The guidance for Q2-24 shows the same tendency, with a minimum of 9% growth YoY to $2.400B - $2.420B and EPS at $2.92 to $2.97, assuming a net margin above 15%, decreasing/flatish YoY due to lower gross margins.

“The decrease will be driven predominantly by deleverage on fixed costs and our ongoing investment in our multiyear distribution center project.”

Call. Some more information coming from the earning call.

Consumers & Competition. Rapid word about the consumers which apparently keep spending.

“I sort of mentioned that obviously we're monitoring the environment, and it remains dynamic. But we do know that the guest is being more selective but will spend where they choose.”

The question is always asked about competition, and the answer is always the same: It always existed, and Lululemon always performed. Answers during this call were the same. What matters is the brand and its quality and that’s where focus is.

Membership. The company started a membership program in the U.S giving access to different perks like the early access to new products for example.

“We are just beginning to leverage the power of our membership program, which now has approximately 20 million members in North America.”

This could become a good leverage to growth over the next years as those programs give opportunities for brands to engage with and fidelise clients.

Advertising. There are new plans to grow awareness around Lululemon’s brand over the next quarters, especially with the Summer Sweat Games in China during Q2 and new TV campaigns during Q3.

This is important for the company as even management recognizes that their brand awareness is pretty low - maybe a bigger logo would work even better in China.

Conclusion. Lululemon is delivering, as usual. To be entirely honest, there is nothing excellent in this quarter and the stock’s reaction is entirely due to its current (under)valuation. The market thought the brand was slowing down and that their products were less demanded.

The report showed continued growth, demand for their products, a working expansion, stable margins, and guidance that confirms those tendencies. Investors now realize that the company deserved proper multiples.

And it showed with a strong pump after-hours. Let’s see how the stock behaves over the next few weeks. I’m sitting on my hands as I accumulated aggresively laterly and keeping this stock as my bigger position for now.

Thank you for reading it all! If you like it, please consider subscribing to receive it all directly in your inbox and not miss a thing!

Everything I share here is free but if you found the content valuable enough, you can always leave a tip!